PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850089

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850089

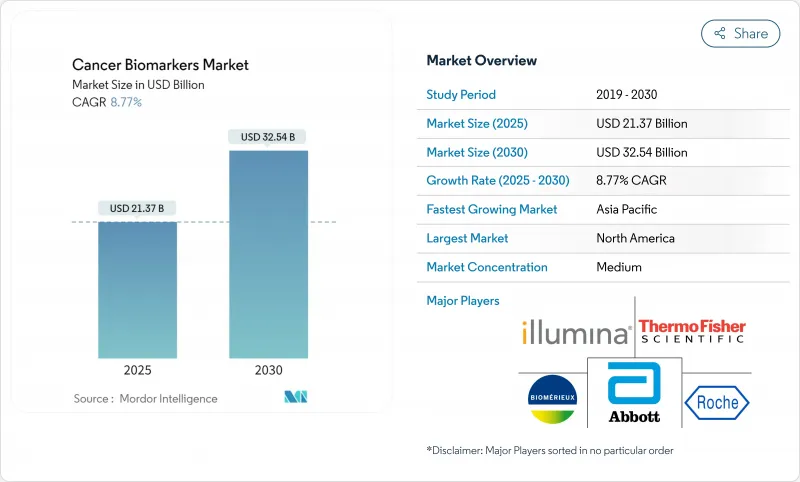

Cancer Biomarkers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The cancer biomarkers market reaches USD 21.37 billion in 2025 and is projected to climb to USD 32.54 billion by 2030, reflecting an 8.77% CAGR.

Strong growth stems from artificial-intelligence platforms that mine multi-omics datasets, enabling the identification of tumor signatures up to seven years before symptoms appear. Liquid-biopsy products now detect colorectal cancer with 83% sensitivity through blood-based methylation analysis, a milestone that the FDA underscored by clearing Guardant Health's Shield test in July 2024. Commercial focus is shifting from reactive diagnosis toward proactive risk assessment, supported by multi-cancer early-detection assays that deliver 98.6% specificity across several tumor types. Competitive intensity is rising as AI-native companies shorten discovery timelines by screening population-scale genomic databases, while established diagnostics firms race to integrate similar capabilities into their existing workflows.

Global Cancer Biomarkers Market Trends and Insights

Surge in Cancer Prevalence

Escalating cancer incidence sustains long-term demand for molecular screening in every major healthcare market. The United States alone recorded more than 1.8 million new cases in 2024, a burden prompting payers to favor tests that can flag tumors at asymptomatic stages. Health systems worldwide recognize that earlier detection through biomarkers lowers mortality and reduces treatment expenditures, strengthening the business case for broad test reimbursement.

Shift to Proactive Risk Assessment & Early Detection

Clinical strategies are pivoting from diagnosing established disease toward predicting individual risk. Oxford Population Health reported 371 plasma-protein signals that forecast multiple cancers up to seven years in advance, illustrating the feasibility of predictive molecular medicine. Large-scale blood-based screens now achieve 75% sensitivity with 98.6% specificity, providing multipurpose screening tools that improve patient compliance in settings where single-tumor tests are impractical.

High Cost of Biomarker-Based Diagnostics

Liquid biopsies average USD 2,800 versus USD 700 for tissue biopsies, limiting adoption in cost-sensitive systems. Medicare still requires extensive clinical-utility evidence before granting broad test coverage, delaying access and compressing vendor margins. While point-of-care devices can reduce procedural outlays, meaningful cost decline hinges on manufacturing scale and automation.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Multi-Omics & NGS Platforms

- AI-Enabled Biomarker Discovery Pipelines

- Uncertain & Region-Specific Reimbursement Pathways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Breast malignancies represented 34.28% of the cancer biomarkers market in 2024, anchored by mature HER2, ER, and PR testing protocols that now guide routine therapeutic decisions in both inpatient and outpatient settings. This leadership rests on decades of clinical evidence that underpins reimbursement and physician familiarity. Expanded use of circulating-tumor-DNA assays further entrenches breast cancer's market position by providing minimally invasive options for monitoring minimal residual disease.

Prostate cancer is the fastest-rising segment, advancing at a 9.35% CAGR to 2030 as non-invasive biomarker panels gain favor in Asia where cultural hesitancy toward traditional screening remains high. Epigenetic assays such as EpiSwitch deliver higher specificity than PSA alone and avoid uncomfortable procedures, a combination that propels uptake in regions where early-stage diagnosis has historically lagged. Together, these trends indicate that prostate cancer will significantly escalate its revenue share despite breast cancer's continuing dominance .

Protein analytes accounted for 52.31% of 2024 revenue thanks to the ubiquity of immunoassays and the extensive clinical evidence supporting protein-based diagnostics. Hospitals rely on ELISA and chemiluminescence platforms that deliver results within hours, reinforcing their preference for protein markers in acute decision-making.

Genetic indicators are anticipated to post a 9.78% CAGR through 2030 as whole-genome sequencing becomes mainstream. Plummeting sequencing costs and AI-driven variant-calling pipelines let clinicians interrogate hundreds of oncogenes simultaneously, propelling genetic tests into frontline care and enlarging the cancer biomarkers market size for precision-genomics offerings. Industry collaboration on multi-gene companion diagnostics further accelerates the revenue expansion of genetic assays.

The Cancer Biomarkers Market is Segmented by Disease (Breast Cancer, Lung Cancer, Prostate Cancer, and More), Biomolecule Type (Protein Biomarkers and More), Profiling Technology (Omics Technologies, Imaging Technologies, and More), End User (Hospitals & Clinics, and More) and Geography (North America, Europe, Asia-Pacific and More). The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 42.41% of 2024 revenue, bolstered by robust reimbursement, an established biobank network, and clear FDA pathways that facilitate rapid test approvals. Federal policy continues to support innovation, even as new rules for laboratory-developed tests impose USD 1.29 billion in compliance costs over four years. Capital commitments such as Roche's USD 50 billion US investment affirm confidence in the region's future growth trajectory.

Europe ranks second, supported by the European Health Data Space, which harmonizes genomic data sharing under GDPR safeguards. Germany's Health Data Use Act and European-wide liquid-biopsy standardization initiatives expand the utility of biomarkers in population screening. Still, stringent privacy obligations prolong data-exchange negotiations, occasionally delaying pan-European trials.

Asia-Pacific is set to record the swiftest 9.91% CAGR as governments allocate more than USD 138 billion to upgrade medical infrastructure by 2027. China's investment in sovereign AI systems and Japan's nationwide genome initiatives underpin local innovation pipelines. Non-invasive tests addressing prostate and gastric cancers are gaining acceptance, narrowing historical disparities in early detection. Diverse regulatory frameworks persist, yet regional harmonization efforts are underway, pointing to streamlined future approvals and an expanding cancer biomarkers market across emerging economies.

- Roche

- Abbott Laboratories

- Thermo Fisher Scientific

- QIAGEN

- Illumina

- Agilent Technologies

- Merck

- bioMerieux

- Quest Diagnostics

- Hologic

- Becton Dickinson & Co.

- Bio-Rad Laboratories

- PerkinElmer

- Myriad Genetics

- NeoGenomics Inc.

- Guardant Health

- Foundation Medicine Inc.

- Exact Sciences Corp.

- NanoString Technologies Inc.

- Bio-Techne

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in prevalence of cancer worldwide

- 4.2.2 Shift from diagnosis to proactive risk assessment & early detection

- 4.2.3 Rapid adoption of multi-omics & NGS platforms

- 4.2.4 AI-enabled biomarker discovery pipelines

- 4.2.5 Expansion of decentralized liquid-biopsy devices in emerging markets

- 4.2.6 Regulators fast-track approvals for companion diagnostics

- 4.3 Market Restraints

- 4.3.1 High cost of biomarker-based diagnostics

- 4.3.2 Uncertain & region-specific reimbursement pathways

- 4.3.3 Stringent data-privacy rules curbing genomic data sharing

- 4.3.4 Limited availability of longitudinal biobank samples

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Disease

- 5.1.1 Breast Cancer

- 5.1.2 Lung Cancer

- 5.1.3 Prostate Cancer

- 5.1.4 Colorectal Cancer

- 5.1.5 Cervical Cancer

- 5.1.6 Other Cancers

- 5.2 By Biomolecule Type

- 5.2.1 Protein Biomarkers

- 5.2.2 Genetic Biomarkers

- 5.2.3 Others

- 5.3 By Profiling Technology

- 5.3.1 Omics Technologies

- 5.3.2 Imaging Technologies

- 5.3.3 Immunoassays

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Clinical & Reference Laboratories

- 5.4.3 Pharma & Biotech Companies

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 F. Hoffmann-La Roche Ltd

- 6.3.2 Abbott Laboratories Inc.

- 6.3.3 Thermo Fisher Scientific

- 6.3.4 QIAGEN N.V.

- 6.3.5 Illumina Inc.

- 6.3.6 Agilent Technologies

- 6.3.7 Merck KGaA (Millipore Sigma)

- 6.3.8 bioMerieux SA

- 6.3.9 Quest Diagnostics

- 6.3.10 Hologic Inc.

- 6.3.11 Becton Dickinson & Co.

- 6.3.12 Bio-Rad Laboratories Inc.

- 6.3.13 PerkinElmer Inc.

- 6.3.14 Myriad Genetics Inc.

- 6.3.15 NeoGenomics Inc.

- 6.3.16 Guardant Health

- 6.3.17 Foundation Medicine Inc.

- 6.3.18 Exact Sciences Corp.

- 6.3.19 NanoString Technologies Inc.

- 6.3.20 Bio-Techne Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment