PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850151

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850151

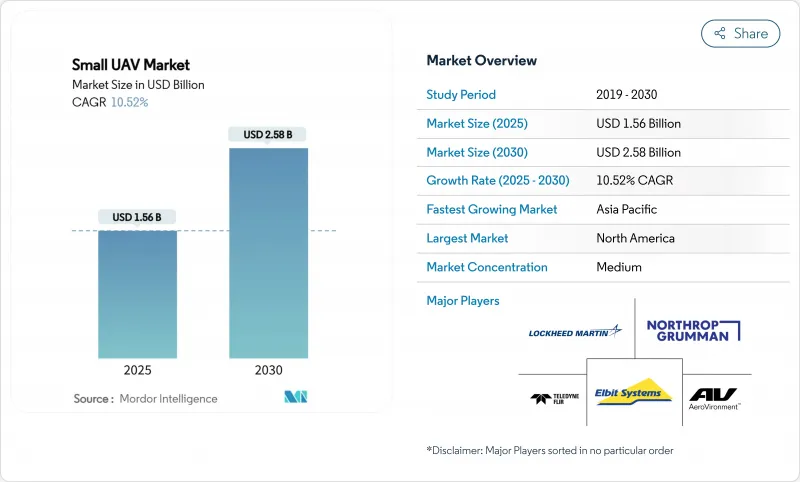

Small UAV - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The small UAV market size stood at USD 1.56 billion in 2025 and is forecasted to reach USD 2.58 billion by 2030, advancing at a 10.59% CAGR.

North American defense procurement programs and an executive order on domestic drone dominance drove early demand, while Asia-Pacific modernization plans continued to accelerate adoption. Swarm autonomy, hybrid airframe designs, and hydrogen fuel-cell propulsion created fresh avenues for differentiation, even as counter-UAS spending threatened to blunt tactical advantages. Semiconductors and lithium-ion cells remained supply-chain pinch points, pushing buyers to favor vendors with assured domestic sourcing. Competitors are therefore focused on vertical integration, software-first architectures, and export-compliant designs to secure a share in the small UAV market.

Global Small UAV Market Trends and Insights

Demand for Real-Time ISR in Contested Environments

Persistent surveillance proved indispensable for commanders operating without full air superiority. Small UAVs flew below radar coverage and streamed video directly to tactical tablets, as seen in the US Army Short Range Reconnaissance effort that invested USD 500 million in compact systems. Ukrainian forces validated quantity-over-quality tactics by launching millions of drones for field awareness. German-supplied HF-1 strike UAVs then added AI terrain-mapping to evade GNSS jamming, extending ISR value inside GPS-denied corridors. Together, these lessons lifted procurement urgency and underpinned a sizable portion of the small UAV market.

Force-Multiplier Value vs Crewed Aircraft

One F-35 costs roughly USD 80 million, whereas a mixed swarm of small UAVs delivers comparable reconnaissance coverage at a fraction of that budget, enabling commanders to hold more targets at risk. Australian trials showed AI algorithms dispatching multiple drones for simultaneous engagements, trimming pilot workload, and shrinking operational footprints. Lockheed Martin then demonstrated an F-35 controlling autonomous wingmen, proving the concept's viability and nudging air arms worldwide to reallocate funds toward the small UAV market.

Cyber/EW Vulnerability and Counter-UAS Proliferation

Raytheon, a business unit of RTX Corporation, earned a USD 196 million order for Coyote interceptors, while Anduril booked USD 250 million for Roadrunner/Pulsar, underscoring a defensive arms race that could erode offensive drone advantages. Qatar's USD 1 billion FS-LIDS purchase illustrated how even smaller militaries can field layered defenses capable of neutralizing unencrypted radio links. Elbit Systems delivered C-UAS kits to NATO states, reaffirming that survivability upgrades would shape platform roadmaps and temper the near-term growth of the small UAV market.

Other drivers and restraints analyzed in the detailed report include:

- DoD-Funded Soldier-Borne and Squad-Level Drone Programs

- AI-Enabled Autonomous Swarming Capability

- Short Endurance and Limited Lethal Payload

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fixed-wing systems led the small UAV market with 55.45% share in 2024, thanks to aerodynamic efficiency that extended ranges needed for ISR patrols. Operators valued their stealthier acoustic signatures and simpler maintenance cycles compared with rotary platforms. Hybrid airframes nevertheless logged a 13.60% CAGR as programs such as the Army's Future Tactical Unmanned Aircraft System demanded vertical launch paired with long-range cruise capabilities. In parallel, the small UAV market size for hybrid variants benefited from shrinking servo weights and more compact flight computers.

Rotary-wing UAVs retained niches in dense urban canyons where maneuverability trumped stamina. AI flight controllers let hybrid vehicles auto-shift between hover and glide, improving coverage rates without adding piloting workload. Vendors such as AeroVironment fielded JUMP 20-X prototypes that embodied this cross-domain agility, winning trials where runways were unavailable. These characteristics prompted procurement planners to diversify fleets, ensuring that hybrids captured incremental budget share across the small UAV market.

Mini UAVs weighing 2 to 20 kg represented 59.17% of the small UAV market share in 2024, aligning with squad portability and enough battery mass for EO/IR payloads. Adoption stayed high because infantry formations required no launch rails or recovery nets. Yet Nano/Micro craft under 2 kg registered a 12.47% CAGR as videogame-style controllers and sub-250 g sensors unlocked new reconnaissance roles. The small UAV market size for these featherweight units grew further once the Neros Archer FPV drone achieved Blue UAS certification, signaling regulatory acceptance for frontline use. Small (20 to 150 kg) vehicles retained utility where lift and fuel capacity trumped stealth, but doctrinal shifts toward distributed lethality kept incremental orders modest. Marine Corps and Army experiments confirmed that even disposable foam-bodied quadcopters produced meaningful battlefield awareness at minimal cost. Accordingly, procurement charters increasingly specified mixed complements that let platoon leaders choose between endurance, payload, and throw-and-go convenience, strengthening the small UAV market.

The Small UAV Market Report is Segmented by Wing Type (Fixed Wing, Rotary Wing, and Hybrid), Size Class (Nano/Micro, Mini, and Small), Application (Electronic Warfare, Logistics and Resupply, and More), Propulsion Type (Internal Combustion Engine, Batteries, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 48.90% revenue in 2024, benefiting from multi-year contracts such as AeroVironment's USD 990 million award and policy measures that mandated domestic sourcing. Blue UAS accreditation incentivized U.S. suppliers to internalize printed-circuit, battery, and optical supply chains, limiting exposure to foreign sanctions. Canada and Mexico adopted similar vetting regimes, sustaining cross-border demand inside the small UAV market.

Asia-Pacific delivered the steepest 11.95% CAGR through 2030 as China, Australia, India, and Japan raced to offset regional flashpoints. Beijing's mothership concept and Tokyo's potential tie-ins with Eurodrone moved procurement from isolated programs to integrated force structures, raising total market value. Canberra's investment in AI-controlled ghost-bat style swarms signalled a doctrinal pivot that other Pacific allies replicated, compounding opportunity for the small UAV market. Supply-chain clustering around Malaysian battery plants and Taiwanese microcontrollers, however, introduced geopolitical risk premiums.

Europe's ReArm Europe fund of EUR 800 billion( USD 937.11 billion) and a EUR 150 billion (USD 175.71 billion) EU loan scheme underwrote local production and eased reliance on external vendors. The Eurodrone program, German consideration of UK-led GCAP membership, and NATO counter-UAS procurements diversified spend across ISR and strike variants, reinforcing continental resilience. Middle East orders, exemplified by Qatar's USD 3 billion agreement, added incremental volumes that offset slower adoption in Africa, ensuring broad geographic balance for the small UAV market.

- AeroVironment, Inc.

- Teledyne Technologies Incorporated

- Elbit Systems Ltd.

- BAYKAR MAKINA SANAYI VE TICARET A.S.

- Northrop Grumman Corporation

- Lockheed Martin Corporation

- Textron Inc.

- Parrot Drones SAS

- Skydio, Inc.

- Anduril Industries, Inc.

- EDGE Group PJSC

- Israel Aerospace Industries Ltd.

- Leonardo S.p.A

- QinetiQ Group

- ideaForge Technology Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for real-time ISR in contested environments

- 4.2.2 Force-multiplier value vs crewed aircraft

- 4.2.3 DoD-funded soldier-borne and squad-level drone programs

- 4.2.4 AI-enabled autonomous swarming capability

- 4.2.5 DARPA projects for GPS-denied navigation

- 4.2.6 Rapid fielding of expendable loitering munitions

- 4.3 Market Restraints

- 4.3.1 Cyber/EW vulnerability and counter-UAS proliferation

- 4.3.2 Short endurance and limited lethal payload

- 4.3.3 Export-control (ITAR/MTCR) hurdles

- 4.3.4 Semiconductor and Li-ion cell supply-chain risk

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Wing Type

- 5.1.1 Fixed Wing

- 5.1.2 Rotary Wing

- 5.1.3 Hybrid

- 5.2 By Size Class

- 5.2.1 Nano/Micro (Less than 2 kg)

- 5.2.2 Mini (2-20 kg)

- 5.2.3 Small (20-150 kg)

- 5.3 By Application

- 5.3.1 Intelligence, Surveillance, and Reconnaissance (ISR)

- 5.3.2 Combat - Loitering Munition

- 5.3.3 Logistics and Resupply

- 5.3.4 Electronic Warfare (EW)

- 5.3.5 Training and Simulation

- 5.4 By Propulsion Type

- 5.4.1 Internal Combustion Engine

- 5.4.2 Batteries

- 5.4.3 Fuel Cells

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Israel

- 5.5.5.1.4 Turkey

- 5.5.5.1.5 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AeroVironment, Inc.

- 6.4.2 Teledyne Technologies Incorporated

- 6.4.3 Elbit Systems Ltd.

- 6.4.4 BAYKAR MAKINA SANAYI VE TICARET A.S.

- 6.4.5 Northrop Grumman Corporation

- 6.4.6 Lockheed Martin Corporation

- 6.4.7 Textron Inc.

- 6.4.8 Parrot Drones SAS

- 6.4.9 Skydio, Inc.

- 6.4.10 Anduril Industries, Inc.

- 6.4.11 EDGE Group PJSC

- 6.4.12 Israel Aerospace Industries Ltd.

- 6.4.13 Leonardo S.p.A

- 6.4.14 QinetiQ Group

- 6.4.15 ideaForge Technology Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment