PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850156

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850156

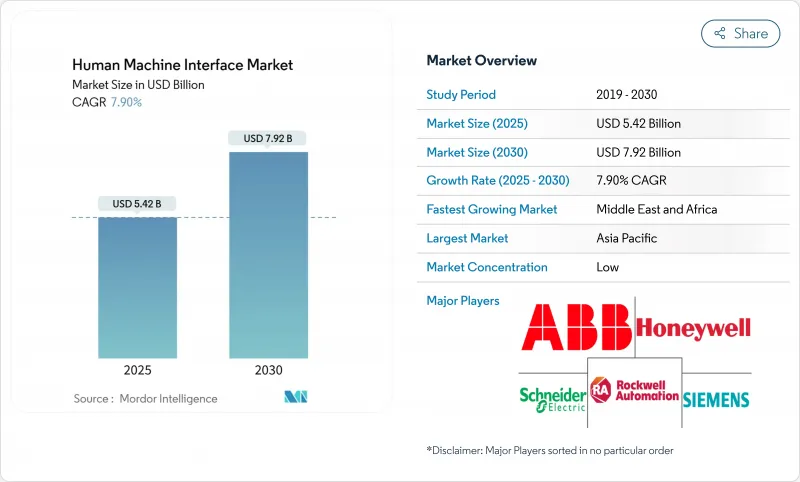

Human Machine Interface - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The HMI market size is estimated at USD 5.42 billion in 2025 and is forecast to reach USD 7.92 billion by 2030, reflecting a 7.9% CAGR.

Strong factory digitalization programs, expanding OT-IT integration, and the shift toward human-centric Industry 5.0 production models are the core demand catalysts. Investments in edge-connected panels, immersive visualization, and secure-by-design architectures continue to rise as manufacturers prioritize real-time insight, lower downtime, and workforce productivity. Hardware retains a clear lead thanks to purpose-built industrial PCs and panels, yet software-defined HMIs and low-code configuration tools are accelerating adoption among smaller plants. Regionally, the HMI market benefits most from large-scale automation in Asia-Pacific and rapid modernization programs in the Middle East & Africa, while North America and Europe focus on cybersecurity compliance and advanced analytics integration.

Global Human Machine Interface Market Trends and Insights

Accelerated Industry 4.0 adoption

Industry 4.0 programs transform HMIs from passive displays into data-driven command hubs that aggregate sensor, MES, and ERP feeds into context-aware dashboards. In many plants, operators now use HMIs to orchestrate co-bots, coordinate batch changes, and launch predictive maintenance workflows. A 2025 MDPI study highlights Industry 5.0's emphasis on collaborative robots, noting that intuitive HMIs are essential for seamless human-machine teamwork. Siemens reported its Senseye platform prevented costly downtime at a dairy facility through AI-enabled anomaly alerts, demonstrating tangible ROI for connected HMIs.

Convergence of OT-IT cybersecurity requirements

Remote connectivity and enterprise cloud links expose legacy panels to modern attack surfaces, prompting a move toward Zero Trust Architecture. The European Union's NIS2 directive compels critical-infrastructure operators to adopt strict authentication and role-based controls on every HMI node. Telefonica Tech underscores that multi-factor authentication and continuous verification are quickly becoming baseline interface functions. Vendors now embed secure boot, signed firmware, and encrypted protocols to satisfy these mandates.

Persistent legacy PLC installed base

Older controllers lack modern protocols, creating integration hurdles. Plants hesitate to rip and replace mature assets, instead layering protocol gateways that add cost and complexity. Food Engineering notes version-control headaches when proprietary buses clash with modern OPC UA or MQTT frameworks.

Other drivers and restraints analyzed in the detailed report include:

- Edge-AI enabling predictive UX

- Low-code/no-code HMI configuration tools

- Energy-efficient industrial displays

- 5G-enabled ultra-low-latency remote HMI

- Supply-chain volatility for specialty semiconductors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware generated 57% of the HMI market in 2024 as rugged panels, industrial PCs, and edge gateways remain mission critical. Texas Instruments confirms a pivot toward embedded AI to balance deterministic control with predictive analytics. The services segment, advancing at 11.4% CAGR, reflects mounting demand for integration, cybersecurity hardening, and continuous training. Control Global observes suppliers shifting from one-off projects to lifecycle partnerships with subscription models for interface optimization.

Hardware evolution now favours modular boards, and high brightness displays certified for Class I, Division 2 zones. Vendors integrate hot-swap SSD bays and field-upgradeable CPUs to extend lifespan. Meanwhile, managed services teams conduct remote UX audits, patch critical vulnerabilities, and retrain operators to exploit new features, a dynamic expected to lift service revenues to nearly one third of overall HMI market size by 2030.

Touchscreens retained 71% of the HMI market in 2024 because glove-friendly capacitive layers and chemically strengthened glass satisfy harsh-plant demands. Multi-touch gestures shorten navigation time and cut error rates, especially in batch changeovers. Yet AR/VR interfaces are scaling fastest at 18.7% CAGR, reshaping operator interaction paradigms. An MDPI study on XR-based robot programming reported faster commissioning and lower downtime than traditional pendant methods.

AR-equipped headsets provide spatial overlays, letting technicians visualize hidden piping, torque targets, or live analytics. Automotive OEMs run immersive design reviews that replace clay modelling and shorten concept loops. This cross-pollination of gaming engines and industrial data paves the way for spatial computing control rooms, potentially capturing an expanded share of HMI market size through 2030.

Human Machine Interface Market is Segmented by Offering (Hardware, Software and More), Interface Technology (Touchscreen, Push-Button / Keypad and More), Configuration (Embedded HMI, Stand-Alone HMI and More), End-User Industry (Automotive, Food & Beverage and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the HMI market with 38% share in 2024. Chinese installations surpassed 18.25 million units, generating revenue of CNY 9.28 billion (USD 1.39 billion) amid a climb in smart-factory rollouts. Japan and South Korea continue to commercialize next-gen OLED panels, while India's production-linked incentives propel automation uptake in pharmaceuticals and consumer durables. Regional suppliers such as Delta Electronics are scaling local manufacturing, widening access to cost-competitive panels.

The Middle East and Africa registers the highest growth at 9.8% CAGR. Vision 2030 initiatives in Saudi Arabia and the UAE's Operation 300bn plan are investing in digital plants for petrochemicals, logistics, and renewables. The Future Manufacturing Africa Conference spotlights AI-driven quality control and workforce upskilling for automation, signalling sustained large-project pipelines.

North America benefits from reshoring incentives and an established industrial-software ecosystem. Platforms like Ignition by Inductive Automation employ unlimited licensing to cut total cost of ownership for multi-site rollouts. Cybersecurity regulations such as CISA guidelines fuel adoption of secure-boot HMIs, further solidifying market demand across defence and critical-infrastructure verticals.

Europe maintains a sizeable slice of the HMI market on the back of regulatory rigor and sustainability leadership. Compliance with NIS2 and eco-design mandates drives preference for energy-efficient, IEC 62443-certified panels. Siemens' USD 2 billion European investment into digital-center expansions underscores the continent's determination to lead in human-centric, low-carbon industry.

- ABB Ltd

- Honeywell International Inc.

- Rockwell Automation, Inc.

- Mitsubishi Electric Corporation

- Schneider Electric SE

- Emerson Electric Co.

- GE Vernova (Industrial Automation)

- Texas Instruments Inc.

- Yokogawa Electric Corporation

- Siemens AG

- Robert Bosch GmbH

- Eaton Corporation plc

- Advantech Co., Ltd.

- Delta Electronics, Inc.

- Beijer Electronics Group

- Omron Corporation

- Parker Hannifin Corporation

- Phoenix Contact GmbH

- Red Lion Controls (Spectris)

- Moxa Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Industry 4.0 adoption

- 4.2.2 Convergence of OT-IT cybersecurity requirements

- 4.2.3 Edge-AI enabling predictive UX

- 4.2.4 Expansion of low-code/no-code HMI configuration tools

- 4.2.5 Energy-efficiency mandates for industrial displays

- 4.2.6 5G-enabled ultra-low-latency remote HMI

- 4.3 Market Restraints

- 4.3.1 Persistent legacy PLC installed base

- 4.3.2 Supply-chain volatility for specialty semiconductors

- 4.3.3 Fragmented UX standards across regions

- 4.3.4 Escalating OT-focused ransomware costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.1.1 HMI Panels

- 5.1.1.2 Industrial PCs

- 5.1.2 Software

- 5.1.2.1 Configuration / Programming

- 5.1.3 Services

- 5.1.1 Hardware

- 5.2 By Interface Technology

- 5.2.1 Touchscreen

- 5.2.2 Push-button / Keypad

- 5.2.3 Gesture-based

- 5.2.4 Voice-controlled

- 5.2.5 AR / VR-assisted

- 5.3 By End-User Industry

- 5.3.1 Automotive

- 5.3.2 Food and Beverage

- 5.3.3 Packaging

- 5.3.4 Pharmaceutical

- 5.3.5 Oil and Gas

- 5.3.6 Metal and Mining

- 5.3.7 Energy and Utilities

- 5.3.8 Aerospace and Defense

- 5.3.9 Semiconductors and Electronics

- 5.3.10 Other End Users

- 5.4 By Configuration

- 5.4.1 Embedded HMI

- 5.4.2 Stand-alone HMI

- 5.4.3 Distributed / Remote HMI

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Russia

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Turkey

- 5.5.4.4 South Africa

- 5.5.4.5 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Honeywell International Inc.

- 6.4.3 Rockwell Automation, Inc.

- 6.4.4 Mitsubishi Electric Corporation

- 6.4.5 Schneider Electric SE

- 6.4.6 Emerson Electric Co.

- 6.4.7 GE Vernova (Industrial Automation)

- 6.4.8 Texas Instruments Inc.

- 6.4.9 Yokogawa Electric Corporation

- 6.4.10 Siemens AG

- 6.4.11 Robert Bosch GmbH

- 6.4.12 Eaton Corporation plc

- 6.4.13 Advantech Co., Ltd.

- 6.4.14 Delta Electronics, Inc.

- 6.4.15 Beijer Electronics Group

- 6.4.16 Omron Corporation

- 6.4.17 Parker Hannifin Corporation

- 6.4.18 Phoenix Contact GmbH

- 6.4.19 Red Lion Controls (Spectris)

- 6.4.20 Moxa Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment