PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850174

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850174

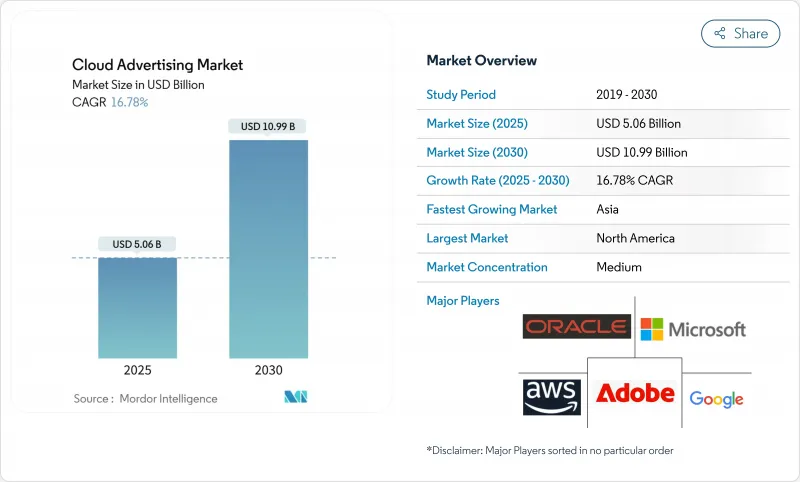

Cloud Advertising - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The cloud advertising market size is estimated at USD 5.06 billion in 2025 and is forecast to reach USD 10.99 billion by 2030, reflecting a 16.8% CAGR.

Demand accelerates as advertisers trade on-premises stacks for elastic, AI-enabled cloud services that deliver millisecond bidding, real-time analytics, and integrated privacy controls. Each new billion flowing into cloud workloads lifts spending on observability, encryption, and GPU-rich instances, making infrastructure a direct revenue lever. Workloads that manage identity graphs, creative generation, and campaign measurement increasingly run in sovereign or logically isolated regions, pushing hyperscalers to bundle clean-room templates and customer-managed keys into reserved-instance offers. Procurement cycles now involve marketing, legal, and IT in equal measure because campaign agility and regulatory alignment have converged into one negotiation.

Global Cloud Advertising Market Trends and Insights

Public-Cloud Retail-Media Acceleration

Retailers operating large e-commerce storefronts shifted ad-serving code to public clouds in 2024. One marketplace cut flash-campaign launch times by 43% after moving to serverless GPU pools and reported double-digit off-peak cost savings, freeing budget for immersive video formats. Hourly inventory-aware promotions have replaced weekly refresh cycles, demonstrating how cloud economics reshape merchandising strategy.

Privacy-Centric First-Party Data Clean Rooms

Europe's GDPR continues to steer architecture decisions. In spring 2025, a multinational broadcaster migrated audience-matching to an encrypted BigQuery clean room, enabling advertisers to measure lift without accessing raw tables . Agencies now request similar blueprints in new tenders, indicating that clean rooms are becoming a default requirement rather than a premium add-on.

Rising Cloud Egress Fees Elevating TCO

Advertisers discovered in 2024 that data-out charges can erode ROI when impression logs traverse multiple clouds. A European gaming publisher cut seven-figure costs by repatriating traffic to a colocation facility with private fiber, without latency penalties. Finance teams now treat network topology as a core budget variable.

Other drivers and restraints analyzed in the detailed report include:

- Programmatic Video Expansion in Asia

- Edge-AI Bidding Engines

- Regional Data-Sovereignty Mandates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid-cloud advertising market size is projected to grow at a 24% CAGR through 2030, underscoring brands' need for elastic compute without relinquishing sensitive identity graphs. A global airline ran edge Kubernetes clusters for passenger-list processing while bursting forecasting tasks to public zones, enabling GDPR-compliant retargeting and real-time yield management. Public-cloud advertising retained 64% cloud advertising market share in 2024 as a streaming service halved rendering costs by using reserved GPU blocks for AV1 encoding. Private-cloud deployments remain critical in finance and healthcare, with a European insurer cutting regulatory man-hours by 20% after migrating segmentation models to a private OpenShift cluster.

Cloud Advertising Market is Segmented by Deployment Type (Public Cloud Advertising, Private Cloud Advertising, Hybrid Cloud Advertising), Service Model (Software As A Service (SaaS) Advertising Platforms, Infrastructure As A Service (IaaS) for Ad Delivery, and More), End-User Industry (Retail and ECommerce, Media and Entertainment, and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 38% of 2024 revenue, supported by dense inter-cloud connectivity that keeps median bid-request round-trip below 120 ms. State-level privacy laws introduced in 2025 spurred demand for policy-as-code tooling, rewarding vendors that abstract compliance into declarative templates.

Asia-Pacific is expected to record the fastest regional growth at 20% CAGR from 2025-2030. Government incentives for data-center construction, renewable energy projects in Guangdong, and low-earth-orbit connectivity across remote Indonesian islands together extend mobile-ad reach to previously unreachable audiences.

Europe faces the strictest privacy regime. A pan-European grocery chain federated encrypted loyalty IDs through sovereign clouds in 2025, trading minor latency overhead for compliance certainty. Advertisers across the region increasingly accept such performance tradeoffs to mitigate regulatory risk.

Latin America's virtuous cycle of logistics investment and advertising revenue continues. A Brazilian fulfilment specialist extended same-day delivery to 55% of urban consumers, boosting click-through rates on sponsored listings and enabling ad revenue to outpace GMV growth.

Middle East and Africa benefit from new terrestrial fiber routes and sovereign-cloud builds. A Gulf airline's Arabic-language retargeting campaign launched from an Abu Dhabi stack in 2025 generated incremental bookings in markets that previously under-indexed on digital spend.

- Adobe Inc.

- Amazon Web Services Inc.

- Google LLC

- Microsoft Corporation

- Oracle Corporation

- IBM Corporation

- Salesforce Inc.

- Sprinklr Inc.

- SAP SE

- Meta Platforms Inc.

- Microsoft Advertising (Xandr)

- The Trade Desk Inc.

- InMobi Pte Ltd

- AppLovin Corporation

- PubMatic Inc.

- Criteo SA

- Magnite Inc.

- Zeta Global Holdings Corp.

- Yahoo Advertising

- Alibaba Cloud

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Public Cloud Adoption by Retail-Media Networks

- 4.2.2 Privacy-Centric First-Party Data Clean Rooms in Europe

- 4.2.3 Programmatic Video Boom Fueling Cloud DSP Demand in Asia

- 4.2.4 Edge-AI Bidding Engines Requiring GPU-Rich IaaS

- 4.2.5 Generative-AI Creative Suites Driving SaaS Uptake

- 4.2.6 SMB eCommerce Expansion in Latin America

- 4.3 Market Restraints

- 4.3.1 Rising Cloud Egress Fees Elevating TCO

- 4.3.2 Regional Data-Sovereignty Mandates

- 4.3.3 Ad-Fraud Detection Latency Concerns

- 4.3.4 Kubernetes / DevOps Talent Shortage

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Intensity of Competitive Rivalry

- 4.6.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Public Cloud Advertising

- 5.1.2 Private Cloud Advertising

- 5.1.3 Hybrid Cloud Advertising

- 5.2 By Service Model

- 5.2.1 Software as a Service (SaaS) Advertising Platforms

- 5.2.1.1 Demand-Side Platforms (DSP)

- 5.2.1.2 Supply-Side Platforms (SSP)

- 5.2.1.3 Ad Exchanges

- 5.2.2 Infrastructure as a Service (IaaS) for Ad Delivery

- 5.2.2.1 Compute-Optimized Instances

- 5.2.2.2 GPU-Accelerated Instances

- 5.2.2.3 Edge / Content Delivery Networks

- 5.2.3 Platform as a Service (PaaS) Marketing Middleware

- 5.2.3.1 Data Clean Rooms

- 5.2.3.2 API Management and Micro-services

- 5.2.3.3 AI / ML Model-Training Platforms

- 5.2.1 Software as a Service (SaaS) Advertising Platforms

- 5.3 By End-User Industry

- 5.3.1 Retail and eCommerce

- 5.3.2 Media and Entertainment

- 5.3.3 Information Technology and Telecom

- 5.3.4 Banking, Financial Services and Insurance (BFSI)

- 5.3.5 Government and Public Sector

- 5.3.6 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 South Korea

- 5.4.4.4 India

- 5.4.4.5 Australia

- 5.4.4.6 New Zealand

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 Adobe Inc.

- 6.3.2 Amazon Web Services Inc.

- 6.3.3 Google LLC

- 6.3.4 Microsoft Corporation

- 6.3.5 Oracle Corporation

- 6.3.6 IBM Corporation

- 6.3.7 Salesforce Inc.

- 6.3.8 Sprinklr Inc.

- 6.3.9 SAP SE

- 6.3.10 Meta Platforms Inc.

- 6.3.11 Microsoft Advertising (Xandr)

- 6.3.12 The Trade Desk Inc.

- 6.3.13 InMobi Pte Ltd

- 6.3.14 AppLovin Corporation

- 6.3.15 PubMatic Inc.

- 6.3.16 Criteo SA

- 6.3.17 Magnite Inc.

- 6.3.18 Zeta Global Holdings Corp.

- 6.3.19 Yahoo Advertising

- 6.3.20 Alibaba Cloud

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment