PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850213

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850213

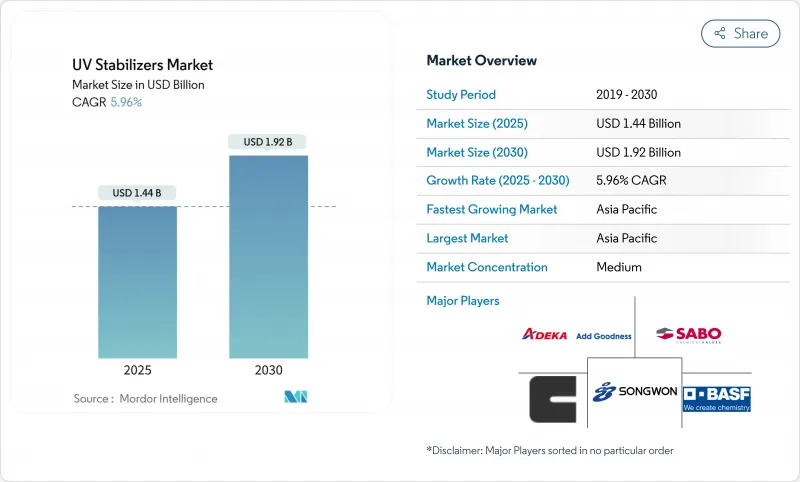

UV Stabilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The UV Stabilizers Market size is estimated at USD 1.44 billion in 2025, and is expected to reach USD 1.92 billion by 2030, at a CAGR of 5.96% during the forecast period (2025-2030).

The expansion reflects rising demand for plastics that retain appearance and mechanical integrity when exposed to sunlight in automotive, packaging, and construction settings. Growth is reinforced by stricter durability standards, rapid industrialization in Asia-Pacific, and mounting sustainability expectations that push producers toward bio-based or biomass-balanced additive lines. Regulatory momentum - including the 2024 listing of UV-328 under the Stockholm Convention - is accelerating reformulation, while recent US tariffs on specialty chemicals are prompting regional supply localization. Concurrently, fast-growing segments such as bead- or granule-form stabilizers and advanced HALS systems are improving processing safety, dispersion, and long-term performance.

Global UV Stabilizers Market Trends and Insights

Rapid Penetration of UV-Stable Polyolefin Films in Asia's Industrial Packaging

Industrial shippers in China and India are replacing conventional wraps with UV-protected polyolefin films that cut material use by up to 15% while extending shelf life. Advanced HALS packages integrated with antioxidants in single-pellet form ensure consistent performance during high-throughput extrusion, leading to broader adoption in electronics logistics.

Shift Toward Low-VOC, Water-Borne Wood Coatings in Europe

Stringent VOC rules are moving European producers toward waterborne systems that need stabilizers compatible with aqueous media. Encapsulated UV absorbers activate after film formation, preventing colour fade and lignin breakdown in outdoor structures, a technology highlighted in recent launches for exterior decking.

Volatility in Feedstock Prices

Geopolitical events and petrochemical realignments have lifted the cost of key diamines and hindered phenols used in HALS production. Manufacturers are pursuing backward integration and catalytic process efficiencies to stabilize costs and protect margins, with one leading Asian producer announcing new on-purpose precursor capacity to offset volatility.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Weather-Resistant 3D-Printed Plastics in North America

- Surge in UV-Stabilized Greenhouse Films Across the Middle East

- Supply-Chain Disruptions of HALS Intermediates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hindered amine light stabilizers account for 65% of 2024 revenue, reflecting their regenerative radical-scavenging mechanism that sustains polyolefin durability over extended outdoor service. Competitive focus has shifted to low-colour HALS grades that maintain clarity while meeting stringent food-contact norms, typified by SI Group's LOWILITE series.

The UV absorbers sub-segment is accelerating as triazine chemistries pair synergistically with HALS, particularly in polycarbonate and acrylic systems that demand optical clarity. Quenchers and antioxidants target narrower niches where thermal-light stability is required simultaneously, such as clear styrenics for lighting lenses.

Polyolefins secured 52% of revenue in 2024. Higher-efficiency HALS has reduced typical loading from 0.25% to 0.15% in blown film without compromising retention of elongation or gloss.

Polyurethanes post the highest CAGR at 6.44% on rising use in clear coats, sealants, and flexible foams exposed to sunlight. PVC, engineering plastics, and elastomers round out the demand profile, each requiring tailored multi-additive packages that address photo-oxidation alongside thermal or chemical stresses.

The UV Stabilizers Market Report Segments the Industry by Type (Hindered Amine Light Stabilizers (HALS), UV Absorbers, Quenchers, and More), End-User Industry (Packaging, Automotive, Agriculture, and More), Polymer Type (Polyolefins, PVC, Polyurethane, and More), Form (Liquid, Powder, and Bead/Granule), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific controlled 54% of 2024 revenue and is forecast for a 6.59% CAGR to 2030, propelled by accelerating automotive builds, infrastructure expansion, and photovoltaic roofing adoption. A collaboration between 3TREES and Solvay produced a TPO BIPV membrane demonstrating 25-year weathering, highlighting regional material innovation. Government incentives in China and India further underpin greenhouse film and industrial packaging volumes, while Japanese electronics majors specify next-generation stabilizers that balance durability with recycling compatibility.

North America ranks second, characterised by high-value applications in transportation, aerospace and additive manufacturing. Research at Purdue University produced a UV-protectant spray that forms a durable film on sensitive surfaces, illustrating academic-industry collaboration to extend service life for composite parts. The region also leads in electric-vehicle TPO fascia adoption.

Europe's stringent chemical and sustainability legislation steers demand toward low-VOC, recyclable formulations. The Cradle-ALP roadmap underscores additive circularity, pressuring formulators to deliver bio-based alternatives without sacrificing lifetime weatherability.

South America shows moderate expansion concentrated in Brazilian and Argentine greenhouse and irrigation products. In the Middle East and Africa, protected-agriculture film demand and big-ticket infrastructure projects fuel above-average growth; Saudi Arabia's large-scale greenhouse initiatives typify the opportunity for premium multi-season HALS packages.

- 3V Sigma S.p.A.

- ADEKA Corporation

- Altana AG

- BASF SE

- Chitec Technology Co., Ltd.

- Clariant

- Eastman Chemical Company

- Everlight Chemical Industrial Co.

- Evonik Industries AG

- Kaneka Corporation

- Lycus Ltd. LLC

- Mayzo Inc.

- Rianlon Corporation

- SABO S.p.A.

- SI Group Inc.

- Solvay

- Songwon

- SUQIAN UNITECH CORP..LTD

- Tianjin Baofeng Chemical Co., Ltd.

- Wanhua

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Penetration of UV-Stable Polyolefin Films in Asia's Industrial Packaging

- 4.2.2 Shift Toward Low-VOC, Water-Borne Wood Coatings in Europe

- 4.2.3 Growing Adoption of Weather-Resistant 3D-Printed Plastics in North America

- 4.2.4 Surge in UV-Stabilized Greenhouse Films Across the Middle East

- 4.2.5 OEM Mandates for Long-Life Exterior Automotive Plastics

- 4.3 Market Restraints

- 4.3.1 Volatility in Feedstock Prices

- 4.3.2 Supply-Chain Disruptions of HALS Intermediates

- 4.3.3 Adoption of High-Barrier Monolayer Films Reducing Need for Stabilizers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Hindered Amine Light Stabilizers (HALS)

- 5.1.2 UV Absorbers

- 5.1.3 Quenchers

- 5.1.4 Antioxidants

- 5.2 By End-Use Industry

- 5.2.1 Packaging

- 5.2.2 Automotive

- 5.2.3 Agriculture

- 5.2.4 Building and Construction

- 5.2.5 Adhesives and Sealants

- 5.2.6 Other End-user Industries (Electrical and Electronics, etc.)

- 5.3 By Polymer Type

- 5.3.1 Polyolefins (PE, PP)

- 5.3.2 PVC

- 5.3.3 Polyurethane

- 5.3.4 Engineering Plastics (PC, PA, PET)

- 5.3.5 Others (Styrenics and Rubber and Elastomers)

- 5.4 By Form

- 5.4.1 Liquid

- 5.4.2 Powder

- 5.4.3 Bead / Granule

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3V Sigma S.p.A.

- 6.4.2 ADEKA Corporation

- 6.4.3 Altana AG

- 6.4.4 BASF SE

- 6.4.5 Chitec Technology Co., Ltd.

- 6.4.6 Clariant

- 6.4.7 Eastman Chemical Company

- 6.4.8 Everlight Chemical Industrial Co.

- 6.4.9 Evonik Industries AG

- 6.4.10 Kaneka Corporation

- 6.4.11 Lycus Ltd. LLC

- 6.4.12 Mayzo Inc.

- 6.4.13 Rianlon Corporation

- 6.4.14 SABO S.p.A.

- 6.4.15 SI Group Inc.

- 6.4.16 Solvay

- 6.4.17 Songwon

- 6.4.18 SUQIAN UNITECH CORP..LTD

- 6.4.19 Tianjin Baofeng Chemical Co., Ltd.

- 6.4.20 Wanhua

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Nano-composites in UV Stabilizers