PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850219

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850219

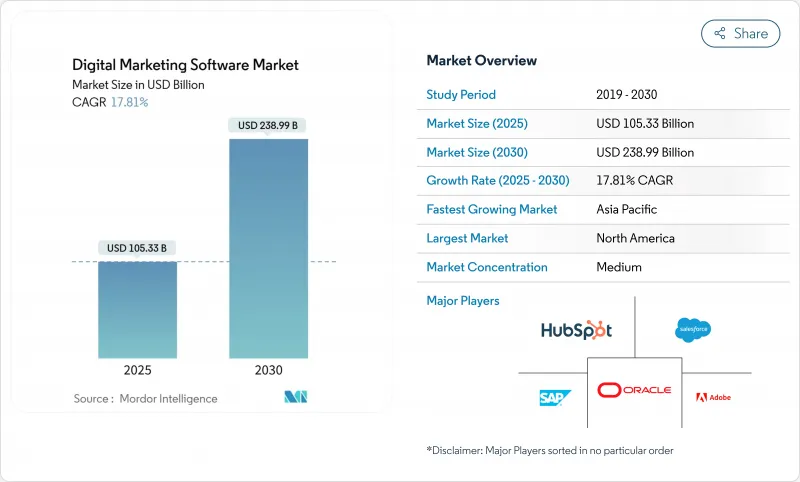

Digital Marketing Software Market - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The global digital marketing software market posted USD 105.33 billion revenue in 2025 and is forecast to touch USD 238.99 billion by 2030, advancing at a 17.81% CAGR over the period.

Rapid migration to cloud-native architectures, AI-driven automation, and cookieless personalization keeps spending on marketing technology at 25.4% of overall marketing budgets. Enterprises now favor integrated suites that unify data, content, and activation functions, replacing fragmented point solutions that raise integration costs. Subscription pricing tied to usage reduces up-front capital outlays, encouraging adoption among mid-market firms. Competitive intensity continues to rise as platform vendors embed generative AI copilots that shorten creative cycles and expand self-service analytics.

Global Digital Marketing Software Market Trends and Insights

Surge in Digital-First Customer Journeys

Seventy percent of B2B buyers now initiate research via search engines, forcing enterprises to re-engineer engagement models across content, data, and commerce. Manufacturing firms allocate 75% of marketing budgets to digital channels, up 10 percentage points versus past cycles. Healthcare providers use AI orchestration to deliver compliant, personalized journeys across web portals and patient apps. European organizations devote 22.9% of digital transformation budgets to marketing technology, recognizing customer experience as a primary competitive lever. The persistent shift toward digital-first engagement underpins sustained demand for unified platforms that manage acquisition, conversion, and retention.

AI-Powered Content and Campaign Optimization

Generative AI platforms such as Adobe GenStudio enable dynamic asset variation at scale, cutting production times by 50% while raising email conversion rates two-fold. HubSpot embedded more than 80 AI features in its Breeze AI release of September 2024, underscoring the race to automate campaign design. Asia-Pacific firms are accelerating investment, with 59% planning higher AI budgets in 2025. Enterprise deployments of autonomous agents, as seen in Salesforce Agentforce, prove marketing workflows can operate with minimal human intervention. AI capability is rapidly becoming a baseline requirement rather than a differentiator.

Integration Complexity with Legacy Martech Stacks

Enterprises average 130 applications in the stack, yet fewer than one-fifth are fully integrated, inflating operational costs and delaying ROI. CMOs cite disconnected data, poor governance, and limited implementation skills as top barriers. Moving to MACH (microservices, API-first, cloud-native, headless) architectures demands technical expertise that many mid-market firms lack, extending timelines and inflating total cost of ownership. European manufacturers illustrate the gap, with only two-thirds achieving digital maturity, compared with nearly four-fifths of US peers.

Other drivers and restraints analyzed in the detailed report include:

- Omnichannel Engagement Demand from B2C and B2B

- Gen-AI Copilots Slashing Creative Production Time

- Data-Privacy and Consent-Management Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud delivery controlled 65.5% of 2024 revenue, and its share of the digital marketing software market size is projected to expand at an 18.5% CAGR through 2030. The economics remain compelling: elastic infrastructure, continuous updates, and lower maintenance overheads drive total cost of ownership down while improving scalability. On-premise installations persist in regulated verticals where data residency and bespoke integration remain critical, but their share shrinks as cloud providers earn advanced security certifications.

Cost alignment with usage encourages mid-market entry, and AI functionality is often available first in cloud editions, reinforcing preference. Vendors offer hybrid models to ease transition, yet the momentum toward full SaaS deployment appears irreversible as enterprises prioritize speed and flexibility.

Software licenses represented 54.9% of 2024 revenue, yet services revenue is set to grow faster at 19.2% CAGR as firms seek expertise to unlock platform value. System integration, data hygiene, and change-management engagements dominate initial projects, while managed services sustain long-term optimization. The digital marketing software market size for service engagements is further buoyed by AI adoption, which requires model training, governance, and iterative performance tuning.

As stacks grow more complex, external partners fill capability gaps, particularly around multi-cloud and composable architectures. Vendors bundle advisory and managed-service offerings into subscription plans, generating sticky recurring revenue and deepening customer lock-in. Training academies and certification programs proliferate to upskill client teams and accelerate platform ROI.

Digital Marketing Software Market is Segmented by Deployment (Cloud and On-Premise), Component (Software and Services), End-User Enterprise Size (Large Enterprises and Small and Medium Enterprises (SMEs)), End-User Vertical (IT and Telecom, BFSI, Retail and E-Commerce, Manufacturing and More) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 41.9% revenue in 2024, driven by deep cloud penetration, a skilled workforce, and dense concentration of platform vendors such as Adobe, Salesforce, and HubSpot. Venture capital continues to favor AI-led martech startups, reinforcing the local innovation flywheel. Growth is steady but moderates as penetration approaches maturity and replacement cycles lengthen.

Asia-Pacific is projected to record a 20.6% CAGR to 2030, the fastest worldwide. Governments incentivize digital transformation, and enterprises are adopting localized AI models that respect linguistic and cultural nuances. Manufacturing and financial-services modernization programs accelerate platform uptake, and domestic vendors emerge to address regulatory specifics. The digital marketing software market size attributable to Asia-Pacific will therefore expand rapidly, even as competition intensifies.

Europe remains a solid but regulated adopter. While only 66% of EU manufacturers have achieved end-to-end digitalization, 56% of executives plan higher technology budgets in 2025. GDPR catalyzes demand for privacy-first platforms, yet also stretches implementation timelines and cost structures. Vendors with compliance-by-design architectures find receptive buyers, and expertise developed in Europe is increasingly exported as other jurisdictions replicate privacy statutes.

- Adobe Inc.

- Salesforce, Inc.

- Oracle Corp.

- SAP SE

- Microsoft Corp.

- HubSpot Inc.

- IBM Corp.

- Google LLC

- SAS Institute Inc.

- Teradata Corp.

- Criteo SA

- Infor Inc.

- Marketo Engage (Adobe)

- ActiveCampaign LLC

- Klaviyo Inc.

- Intuit Mailchimp

- Sendinblue (Brevo)

- Zoho Corporation

- Constant Contact

- Sitecore

- Acoustic L.P.

- Insider Inc.

- Sprinklr

- Braze Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in digital-first customer journeys

- 4.2.2 Cloud-native SaaS cost advantages

- 4.2.3 AI-powered content and campaign optimization

- 4.2.4 Omnichannel engagement demand from B2C and B2B

- 4.2.5 Zero-party data and cookieless personalization

- 4.2.6 Gen-AI copilots slashing creative production time

- 4.3 Market Restraints

- 4.3.1 Integration complexity with legacy martech stacks

- 4.3.2 Data-privacy and consent-management compliance costs

- 4.3.3 Rising unit prices for 1st-party data enrichment

- 4.3.4 CX talent shortage for AI-led campaign design

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By End-user Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Mid-sized Enterprises

- 5.4 By End-user Industry

- 5.4.1 IT and Telecom

- 5.4.2 Media and Entertainment

- 5.4.3 BFSI

- 5.4.4 Retail and E-commerce

- 5.4.5 Manufacturing

- 5.4.6 Healthcare and Life Sciences

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Spain

- 5.5.3.7 Switzerland

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Malaysia

- 5.5.4.6 Singapore

- 5.5.4.7 Vietnam

- 5.5.4.8 Indonesia

- 5.5.4.9 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 Nigeria

- 5.5.5.2.2 South Africa

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Adobe Inc.

- 6.4.2 Salesforce, Inc.

- 6.4.3 Oracle Corp.

- 6.4.4 SAP SE

- 6.4.5 Microsoft Corp.

- 6.4.6 HubSpot Inc.

- 6.4.7 IBM Corp.

- 6.4.8 Google LLC

- 6.4.9 SAS Institute Inc.

- 6.4.10 Teradata Corp.

- 6.4.11 Criteo SA

- 6.4.12 Infor Inc.

- 6.4.13 Marketo Engage (Adobe)

- 6.4.14 ActiveCampaign LLC

- 6.4.15 Klaviyo Inc.

- 6.4.16 Intuit Mailchimp

- 6.4.17 Sendinblue (Brevo)

- 6.4.18 Zoho Corporation

- 6.4.19 Constant Contact

- 6.4.20 Sitecore

- 6.4.21 Acoustic L.P.

- 6.4.22 Insider Inc.

- 6.4.23 Sprinklr

- 6.4.24 Braze Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment