PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850232

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850232

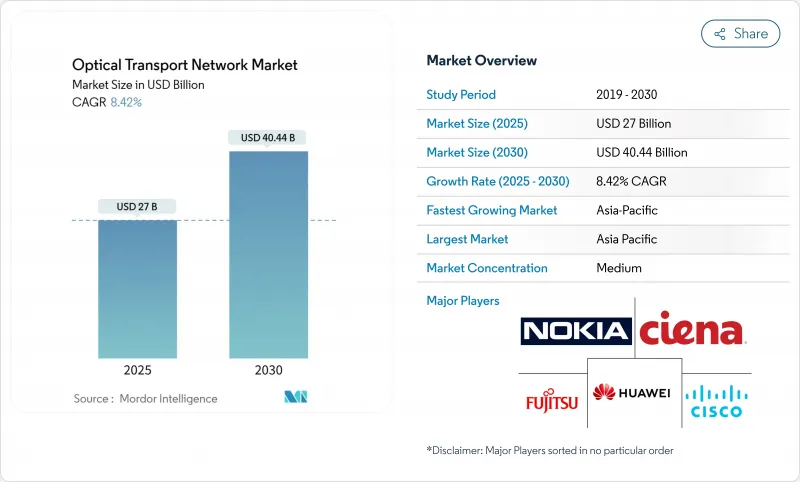

Optical Transport Network - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The optical transport network market is valued at USD 27 billion in 2025 and is on track to reach USD 40.44 billion by 2030, translating into an 8.42% CAGR.

Rising data-center-interconnect bandwidth, the commercialization of 400ZR/ZR+ coherent pluggables, and government-funded fiber rollouts are guiding this expansion. Hyperscalers alone expect to channel USD 215 billion into digital infrastructure in 2025, intensifying demand for high-capacity dense-wavelength-division multiplexing (DWDM) systems. Silicon photonics cost curves are falling after the shift to 6-inch indium-phosphide wafers, while open-line architectures are lowering capital outlays for carriers. Taken together, these forces position the optical transport network market as an essential backbone for artificial-intelligence clusters, cloud interconnects, and broadband inclusion.

Global Optical Transport Network Market Trends and Insights

Rapid 400 ZR/ZR+ Adoption for DCI

Commercial availability of standardized 400ZR and ZR+ pluggables now lets operators plug coherent optics directly into routers, eliminating standalone transponders and trimming equipment cost. Coherent's industrial-temperature 100G ZR QSFP28-DCO ships at only 5.5 W power draw, making coherent links viable in edge locations. Operators are logging 20-39% total-cost-of-ownership reductions from IP-optical convergence, and hyperscalers are already redesigning network fabrics to exploit these savings. Ciena's 1.6T Coherent-Lite and new 448 Gb/s PAM4 optics answer a sixfold rise in DCI throughput expected by 2030. Most short-term gains will materialize in North America and APAC, where hyperscaler campus clusters generate bursty, latency-sensitive traffic.

Hyperscaler AI-Cluster Traffic Boom

Bandwidth tied to machine-learning training clusters is scaling much faster than traditional workloads. Fiber-optical transceiver revenue for AI fabrics is forecast to compound at 30% through 2028, dwarfing the 9% pace for non-AI deployments. Lumen Technologies signed USD 8 billion in new fiber deals during 2024, including a large order with Microsoft that underlines the scale of AI-driven optical demand. Coherent's 300-port optical-circuit switch and Google's deployment of similar technology in TPUv4 pods illustrate the architectural shift toward wavelength-selective, reconfigurable fabrics. This driver supports medium-term growth, especially in North America and the European Union as their hyperscale campuses expand.

Capex Freeze at Tier-2 Telcos (2024-25)

Smaller operators curtailed spending sharply in 2024, with Nokia citing a 23% slide in optical-network revenue because European and Asian customers deferred upgrades. Ciena's optical revenue also fell to USD 2.64 billion, mirroring tight budgets and low average revenue per user in Europe. Ekinops disclosed a 41% decline in optical-transport sales, underscoring widespread caution. This restraint widens the gap between cash-rich hyperscalers advancing optical rollouts and traditional carriers postponing modernization.

Other drivers and restraints analyzed in the detailed report include:

- Government Fibre-Backhaul Stimulus (US BEAD, EU CEF-2)

- Silicon Photonics Price Inflection

- US-China Export Controls on Coherent DSPs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

DWDM retained a 62% share of the optical transport network market in 2024, confirming its status as the backbone for long-haul and metro connections. 800G-ready DWDM links are set to grow at 14.5% CAGR to 2030 as operators consolidate traffic from AI clusters and 5G backhaul into fewer wavelengths, boosting spectral efficiency.

Continuous DSP innovation anchors this shift. Ciena's WaveLogic 6 pushes 1.6 Tb per wavelength, and Nokia's PSE-6s raises reach at 800G speeds. These breakthroughs keep the optical transport network market moving toward flexible-grid operation, while Infinera's 83.6 Tbps field test shows the upper ceiling is still rising. Convergence of DWDM and packet-optical functions now guides procurement decisions in both carrier and cloud settings, embedding integrated platforms as default choices.

The next horizon is C + L band expansion and the inclusion of previously unused wavelength windows, as Japan's 402 Tbps field record revealed. China Broadnet's Huawei-based 400G OTN deployment underscores high-density switching trends, and C+L integration lifts per-rack capacity to 100 Tbit/s. These moves ensure the optical transport network market remains future-proof as data rates climb beyond 1 Tb per channel.

Components accounted for 54% of the optical transport network market size in 2024, led by coherent transceivers, ROADMs, and optical circuit switches. Sales of standardized pluggables are projected to double from USD 600 million in 2024, propelled by multi-vendor interoperability under the 400ZR specification.

Edge-ROADM units grow at a 13.2% CAGR because network disaggregation lets carriers and hyperscalers insert wavelength-selective switching directly at aggregation sites. At the same time, network-design and integration services are pivoting toward intent-based automation, helping customers translate application-level requirements into optical-path provisioning.

Managed network offerings are reviving under bandwidth-as-a-service models that bundle equipment and lifecycle management. Swift rollout of optical platform components, especially colorless-directionless-contentionless (CDC) architectures, is unlocking flexible spectrum allocation. Service providers thus shift operating models away from box-centric procurement to outcome-oriented contracts, realigning internal skill sets around software orchestration.

The Optical Transport Network Market Report is Segmented by Technology (WDM, DWDM, and More), Offering (Services and Components), End-User Vertical (IT and Telecom Operators, Cloud and Colocation Data Centers, Healthcare, and More), Application (Long-Haul DWDM, Metro Networks, and More), Data Rate / Wavelength (100-400 Gbit/S, 400-800 Gbit/S, and More), and Geography.

Geography Analysis

Asia-Pacific controlled 35% of 2024 revenue and is projected to expand at a 10.8% CAGR, the fastest across regions. Chinese authorities selected over 20 cities for 10 G broadband pilots; China Mobile alone serves 272 million broadband lines, with one-third on gigabit tiers. Japan partners NTT and Intel on government-funded optical semiconductors, while South Korea's K-Network 2030 allocates USD 481 million for 6 G research and low-orbit satellite links. The ALPHA subsea cable, with 18 Tbit/s per fiber pair, fortifies regional interconnectivity.

North America sits on mature infrastructure yet sees renewed momentum as the USD 42.45 billion BEAD program funnels capital into middle-mile construction. Lumen's USD 8 billion fiber contracts and Zayo's USD 4 billion long-haul expansion reveal how AI-driven edge compute is reconfiguring route demand. Workforce shortages remain acute: 205,000 additional technicians are needed, spurring training alliances among carriers, vendors, and the Fiber Broadband Association.

Europe balances ambitious digital-sovereignty goals with tight operator cash flow. The European Investment Bank's EUR 350 million loan to Deutsche Glasfaser targets rural gigabit coverage, while the CEF Digital scheme outlines EUR 200 billion requirements for very-high-capacity networks. Operator ARPU remains muted, so public co-funding remains critical. Orange Poland's build for 155,000 homes highlights reliance on blended finance. Planned 48-pair subsea links between the UK and mainland Europe will trim latency by up to 5.5 ms for certain routes.

- Nokia

- Ciena

- Cisco Systems

- Huawei

- Fujitsu

- ZTE

- Infinera

- Ericsson

- NEC

- Coriant (Infinera)

- ADVA Optical Networking

- Ribbon Communications

- Tejas Networks

- ECI Telecom (Ribbon)

- Juniper Networks

- Sterlite Technologies

- NativeWave

- Ciena-Photonera

- Padtec

- FiberHome

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid 400 ZR/ZR+ adoption for DCI

- 4.2.2 Hyperscaler AI-cluster traffic boom

- 4.2.3 Government fibre-backhaul stimulus (US BEAD, EU CEF-2)

- 4.2.4 Open-line systems lowering capex

- 4.2.5 Silicon photonics price inflection

- 4.2.6 Under-sea green-field cables (>20 Tb/s)

- 4.3 Market Restraints

- 4.3.1 Capex freeze at Tier-2 telcos (2024-25)

- 4.3.2 US-China export controls on coherent DSPs

- 4.3.3 Skilled-labour shortage for fibre installation

- 4.3.4 Supply-chain dependency on InP epitaxy

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 WDM

- 5.1.2 DWDM

- 5.1.3 O-band and Other Technologies

- 5.2 By Offering

- 5.2.1 Services

- 5.2.1.1 Network Maintenance and Support

- 5.2.1.2 Network Design and Integration

- 5.2.2 Components

- 5.2.2.1 Optical Transport Equipment

- 5.2.2.2 Optical Switch

- 5.2.2.3 Optical Platform/Edge ROADM

- 5.2.1 Services

- 5.3 By End-user Vertical

- 5.3.1 IT and Telecom Operators

- 5.3.2 Cloud and Colocation Data Centres

- 5.3.3 Government and Defence

- 5.3.4 Healthcare

- 5.3.5 Banking and Financial Services

- 5.3.6 Others (Utilities, Education)

- 5.4 By Application

- 5.4.1 Long-Haul DWDM

- 5.4.2 Data-Center-Interconnect (DCI)

- 5.4.3 Metro Networks

- 5.4.4 Enterprise Networks

- 5.5 By Data Rate / Wavelength

- 5.5.1 100-400 Gbit/s

- 5.5.2 400-800 Gbit/s

- 5.5.3 Beyond 800 Gbit/s

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 UK

- 5.6.2.3 France

- 5.6.2.4 Rest of Europe

- 5.6.3 Asia Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 ASEAN

- 5.6.3.6 Rest of Asia Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nokia

- 6.4.2 Ciena

- 6.4.3 Cisco Systems

- 6.4.4 Huawei

- 6.4.5 Fujitsu

- 6.4.6 ZTE

- 6.4.7 Infinera

- 6.4.8 Ericsson

- 6.4.9 NEC

- 6.4.10 Coriant (Infinera)

- 6.4.11 ADVA Optical Networking

- 6.4.12 Ribbon Communications

- 6.4.13 Tejas Networks

- 6.4.14 ECI Telecom (Ribbon)

- 6.4.15 Juniper Networks

- 6.4.16 Sterlite Technologies

- 6.4.17 NativeWave

- 6.4.18 Ciena-Photonera

- 6.4.19 Padtec

- 6.4.20 FiberHome

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment