PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850236

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850236

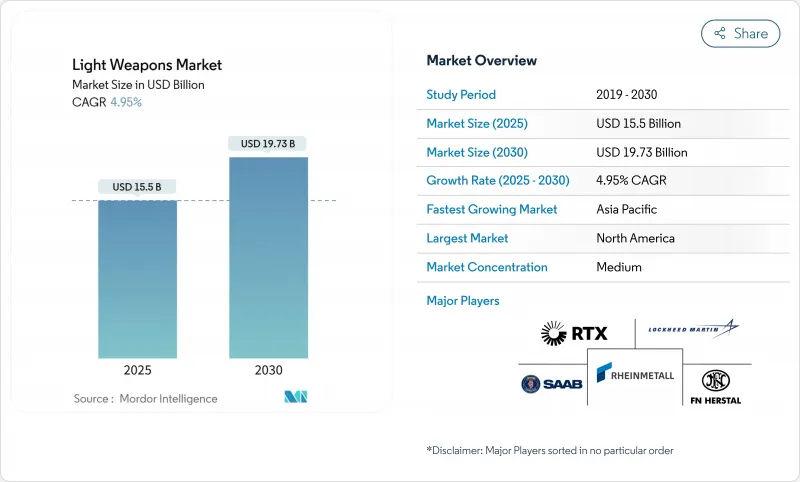

Light Weapons - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The light weapons market size was valued at USD 15.50 billion in 2025 and is forecasted to reach USD 19.73 billion by 2030, translating into a 4.95% CAGR.

This steady advance stems from defense-budget expansion in response to heightened geopolitical risk, with global military expenditure rising 9.4% to USD 2.718 trillion in 2024. Procurement priorities concentrate on man-portable precision systems, while naval close-in programs and polymer-composite ammunition illustrate parallel modernization currents. Technology convergence-especially AI-enabled fire-control modules-allows armed forces to upgrade legacy inventories at a lower cost than wholesale fleet replacement. Vendor competition remains moderate: established contractors guard incumbency through scale and compliance expertise, yet niche innovators exploit software-centric differentiation. Raw-material price volatility and tightening arms-export rules temper growth but outweigh the demand pull created by escalating regional flashpoints.

Global Light Weapons Market Trends and Insights

Escalating Defense Budgets Amid Geopolitical Tensions

European military outlays climbed 17% to USD 693 billion in 2024 as NATO states reacted to Russia's invasion of Ukraine. Poland will raise defense spending to 4.7% of GDP by 2025, while Germany's EUR 100 billion (USD 109 billion) special fund underlines long-term commitment. The European Union's ReArm Europe proposal aims to mobilize EUR 800 billion (USD 870 billion), which includes EUR 150 billion (USD 163 billion) in joint-procurement loans. This initiative has led to significant infantry weapon orders, such as Germany's EUR 8.5 billion (USD 9.2 billion) ammunition contract with Rheinmetall, strengthening the demand in the light weapons market.

Proliferation of Asymmetric Warfare Driving Demand for Man-Portable Systems

Ukraine's battlefield experience shows how man-portable missiles blunt heavier forces, prompting regional actors to stockpile similar assets; European arms imports doubled in 2019-2023 versus 2014-2018. Taiwan's purchase of Switchblade 300 loitering munitions worth USD 360.2 million highlights Asia-Pacific uptake. Smart-rifle scopes such as the SMASH 2000L, fielded under a USD 13 million US Army program, illustrate counter-drone. Asymmetric doctrine thus sustains multi-role, low-footprint products within the light weapons market.

Stringent International Arms-Transfer Regulations

The US Commerce Department imposed tighter firearms-export rules in May 2024, presuming denial for many commercial deals. Washington's revised Conventional Arms Transfer policy blocks shipments likely to enable rights abuses. The Arms Trade Treaty, now at 113 parties, mandates prior risk assessments.The UK's 2024 Export Control amendment added emerging-tech coverage. Compliance overhead and license uncertainty curb smaller exporters' access to the light weapons market.

Other drivers and restraints analyzed in the detailed report include:

- Modernization of Infantry Units with Lightweight Modular Weaponry

- Rising Counter-Terror Operations and Urban Warfare Requirements

- Volatile Raw-Material Prices for Specialty Alloys and Electronics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

MANPADS generated 33.35% of 2024 revenue, the highest individual slice of the light weapons market size, reflecting broad procurement of Stinger-class missiles by Taiwan and Eastern European allies. Although loitering drones threaten substitution, established logistics chains and immediate availability keep demand resilient. Heavy machine guns and mortars retain niche relevance through service-life extension contracts, while counter-drone rifles form a fledgling but important category.

Grenades and grenade launchers delivered the fastest 8.91% CAGR outlook. Programmable air-burst rounds and precision launchers, such as the Mk 47 acquired by Colt CZ, illustrate value migration toward guided sub-munitions. Urban warfare doctrines and policing requirements underpin dual-use sales. Together, these trends ensure product-mix diversification inside the light weapons market.

Guided munitions commanded 55.51% revenue in 2024 and will outpace other technologies at 7.40% CAGR, underlining their mass in the light weapons market share hierarchy. Beam-riding laser models and IR fire-and-forget missiles reduce operator exposure and meet collateral-damage thresholds, as evidenced by Thales' Lightweight Multi-role Missile trials.

Unguided systems persist due to their price advantage and resilience against jamming. Budget-constrained forces stockpile inexpensive rounds to ensure supply sufficiency. As electronic warfare (EW) threats expand, dual inventories-smart and dumb-provide hedge flexibility, securing a stable niche for unguided products within the light weapons industry.

The Light Weapons Market Report is Segmented by Type (Heavy Machine Guns (HMGs), Grenades and Grenade Launchers, Mortars, and More), Technology (Guided and Unguided), Platform (Land-Based, Airborne, and Naval), End-User (Army, Special Forces, and More), Material (Steel and Specialty Alloys, Polymer Composites, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the market with 38.70% revenue in 2024, anchored by the United States' USD 997 billion defense budget. Robust domestic orders underpin economies of scale, while Foreign Military Sales extend reach into allied fleets. Lockheed Martin's Missiles and Fire Control sales climbed 13% to USD 3.37 billion in Q1 2025 as backlog visibility improved.

Asia-Pacific's light weapons market size is projected to grow at a 7.65% CAGR through 2030, the fastest regional rate. India's 20% compound defense-capital growth through FY24-FY29 sustains local sourcing mandates covering 65% of contracts. The Philippines earmarked USD 35 billion under Re-Horizon 3, while Japan's 21% budget hike marks the largest since 1952. Rising China-related security anxiety fuels multi-country rearmament, giving suppliers an expansive pipeline.

Europe's surge in military spending-up 17% year-on-year to USD 693 billion-creates the most immediate procurement spike. Germany's EUR 100 billion (USD 109 billion) fund, Poland's 4.7% of GDP target, and the EU's ReArm proposal underpin a broad, multi-year refresh of infantry weapons. Joint programs such as the UK-Germany deep-strike missile demonstrate intra-European industrial cohesion, boosting the regional light weapons market.

- FN Herstal, S.A. (FN Browning Group)

- Saab AB

- RTX Corporation

- MBDA

- Thales Group

- BAE Systems plc

- Rheinmetall AG

- Rostec

- Lockheed Martin Corporation

- Rafael Advanced Defense Systems Ltd.

- Denel SOC Ltd.

- Heckler & Koch GmbH

- Israel Aerospace Industries Ltd.

- LIG Nex1 Co. Ltd.

- SIG Sauer Inc.

- Fabbrica d'Armi Pietro Beretta SpA

- Northrop Grumman Corporation

- Colt's Manufacturing Company LLC

- China North Industries Group Corporation Limited (NORINCO)

- Barrett Firearms Manufacturing Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating defense budgets amid geopolitical tensions

- 4.2.2 Proliferation of asymmetric warfare driving demand for man-portable systems

- 4.2.3 Modernization of infantry units with lightweight modular weaponry

- 4.2.4 Rising counter-terror operations and urban warfare requirements

- 4.2.5 Integration of AI-enabled fire-control modules into legacy light weapons

- 4.2.6 Emergence of polymer-cased ammunition reducing soldier load

- 4.3 Market Restraints

- 4.3.1 Stringent international arms-transfer regulations

- 4.3.2 Volatile raw-material prices for specialty alloys and electronics

- 4.3.3 Battlefield shift toward loitering munitions curbing MANPATS demand

- 4.3.4 Environmental/health concerns over legacy propellants

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Heavy Machine Guns (HMGs)

- 5.1.2 Grenades and Grenade Launchers

- 5.1.3 Mortars

- 5.1.4 Man-portable Anti-tank Systems (MANPATS)

- 5.1.5 Man-portable Air-Defense Systems (MANPADS)

- 5.1.6 Other Types

- 5.2 By Technology

- 5.2.1 Guided

- 5.2.1.1 Laser Guided

- 5.2.1.2 Infra-red Guided

- 5.2.1.3 Satellite Guided

- 5.2.1.4 Semi-automatic Command to Line of Sight

- 5.2.2 Unguided

- 5.2.1 Guided

- 5.3 By Platform

- 5.3.1 Land-based

- 5.3.2 Airborne

- 5.3.3 Naval

- 5.4 By End-user

- 5.4.1 Army

- 5.4.2 Special Forces

- 5.4.3 Law Enforcement Agencies

- 5.4.4 Homeland Security/Paramilitary

- 5.4.5 Others

- 5.5 By Material

- 5.5.1 Steel and Specialty Alloys

- 5.5.2 Aluminum and Light-Metal Alloys

- 5.5.3 Polymer Composites

- 5.5.4 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 Israel

- 5.6.5.1.3 UAE

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 FN Herstal, S.A. (FN Browning Group)

- 6.4.2 Saab AB

- 6.4.3 RTX Corporation

- 6.4.4 MBDA

- 6.4.5 Thales Group

- 6.4.6 BAE Systems plc

- 6.4.7 Rheinmetall AG

- 6.4.8 Rostec

- 6.4.9 Lockheed Martin Corporation

- 6.4.10 Rafael Advanced Defense Systems Ltd.

- 6.4.11 Denel SOC Ltd.

- 6.4.12 Heckler & Koch GmbH

- 6.4.13 Israel Aerospace Industries Ltd.

- 6.4.14 LIG Nex1 Co. Ltd.

- 6.4.15 SIG Sauer Inc.

- 6.4.16 Fabbrica d'Armi Pietro Beretta SpA

- 6.4.17 Northrop Grumman Corporation

- 6.4.18 Colt's Manufacturing Company LLC

- 6.4.19 China North Industries Group Corporation Limited (NORINCO)

- 6.4.20 Barrett Firearms Manufacturing Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment