PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850254

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850254

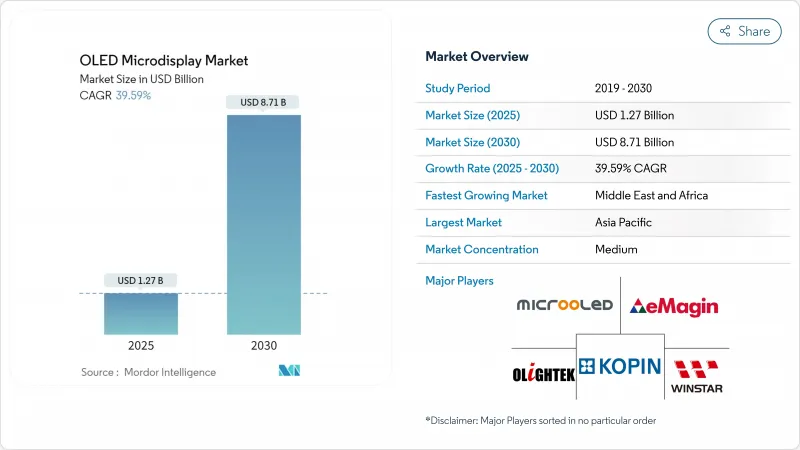

OLED Microdisplay - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The oled microdisplay market is valued at USD 1.27 billion in 2025 and is forecast to reach USD 8.71 billion by 2030, advancing at a 39.59% CAGR.

Robust demand for compact, high-resolution near-eye panels in augmented and virtual reality headsets, military helmet systems and premium automotive head-up displays is accelerating volume growth. Direct patterning and tandem-stack architectures are lifting brightness ceilings toward 60,000 nits while cutting power draw, strengthening the technology's position against emerging MicroLED. Parallel capacity expansions at Chinese OLED-on-Silicon foundries are lowering unit costs and shortening lead times, which encourages broader consumer-electronics adoption. Strategic acquisitions-most notably Samsung Display's 2024 purchase of eMagin-are pushing advanced process know-how into high-volume manufacturing lines, widening the performance gap with late-entry competitors

Global OLED Microdisplay Market Trends and Insights

Expansion of OLED-on-Silicon Capacity by Chinese Foundries

Production ramp-ups at BOE, SeeYA and IRay Group are injecting high-volume, high-yield supply into the oled microdisplay market. Foundries are pairing pixel-dense front-planes with newly built silicon backplane lines to raise throughput and tighten process control. IRay's dedicated backplane investment illustrates a vertical-integration push that reduces outsourcing steps, enhancing cost competitiveness.These moves reposition Asia Pacific from a regional to a global supply anchor, challenging Japanese and Korean incumbents on both scale and technology leadership. Wider capacity also stabilizes pricing, encouraging consumer device OEMs to commit to long-term oled microdisplay market orders.

Accelerated Adoption in Military Helmet-Mounted Displays

North American defense programs are rapidly shifting from AMLCD to OLED microdisplays for pilot, ground-troop and night-vision optics. Kopin's USD 7.5 million award in April 2025 underscores rising demand for ruggedized near-eye modules with superior contrast, zero-motion blur and reduced weight.Validation within the F-35 platform demonstrates mission-critical reliability, prompting other programs to specify similar display architectures. Diversification into weapon sights and command-control eyewear spreads procurement risk, making military demand a stable cornerstone of the oled microdisplay market.

Moisture-Ingress Encapsulation Challenges for OLEDoS

The persistent challenge of moisture ingress represents a significant technical barrier to widespread OLED microdisplay adoption, particularly in harsh operating environments like automotive and military applications. Unlike conventional displays, the ultra-compact form factor of microdisplays leaves minimal space for traditional encapsulation methods, creating a fundamental engineering challenge that impacts both manufacturing yield and long-term reliability. Recent innovations from Korean universities have introduced multi-functional encapsulation for fiber-based wearable OLEDs, potentially offering pathways to more robust solutions. The technical complexity of this challenge is compounded by the need for encapsulation solutions that maintain optical clarity while providing hermetic sealing-a balance that becomes increasingly difficult as pixel densities exceed 3,000 ppi. This constraint particularly impacts applications where extended operational lifetimes are expected, such as automotive displays with 10+ year service requirements, creating a competitive opportunity for companies that can develop proprietary encapsulation technologies.

Other drivers and restraints analyzed in the detailed report include:

- Automotive OEM Integration of AR Head-Up Displays

- Surge in High-End Mirrorless Camera EVFs

- Sub-1,000 cd/m2 Brightness Ceiling versus MicroLED

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The oled microdisplay market size for Near-to-Eye devices stood at USD 0.81 billion in 2025, equal to 64% of total revenue. Sustained shipments to mixed-reality headsets, training goggles and smart helmets anchor demand. Ecosystem investment from platform owners supports annual resolution and brightness upgrades, which in turn lift average selling prices and gross margins.

Electronic Viewfinders contributed a smaller base in 2025, yet their 41.2% CAGR prospect through 2030 signals ample headroom. Professional mirrorless bodies from Sony, Nikon and Canon are standardizing OLED EVFs to deliver lag-free framing and HDR previews. As camera makers streamline model cycles, panel volumes could double within three years, establishing EVFs as a strategic hedge within the oled microdisplay market.

The HD 720p tier held 36% of oled microdisplay market share in 2024, balancing acceptable clarity with tight power budgets for mainstream AR viewers. Growth momentum, however, lies in the Above-FHD tier where pixel densities exceed 3,000 ppi. Early 2025 samples from Samsung Display achieve 5,000 ppi and 20,000 nits peak luminance, positioning these panels for enterprise VR and military recon goggles.

A 42.3% CAGR forecast to 2030 for Above-FHD shipments will absorb much of the incremental oled microdisplay market size expansion. Higher bandwidth interfaces and low-latency drivers accompany these panels, creating ancillary silicon demand that benefits integrated suppliers.

The OLED Microdisplay Market Report is Segmented by Type (Near-To-Eye, Projections, and More), Resolution (SVGA and Below (<=800 X 600), XGA (1, 024 X 768), and More), Technology (RGB OLED-On-Silicon, and More), Panel Size (Diagonal) ( Less Than 0. 5 Inch, 0. 5-1. 0 Inch, and More), End-User Industry (Automotive, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific commanded 57% of global revenue in 2024, reflecting the region's dense network of backplane fabs, emitter suppliers and consumer-device assemblers. Ongoing capacity expansions by Samsung Display and leading Chinese foundries ensure supply continuity, while cross-border joint ventures smooth technology transfer. Government incentives in South Korea and China further lower production costs, sustaining regional leadership.

North America anchors high-specification demand, especially for defense and enterprise-XR deployments that demand ruggedized, high-brightness modules. Venture-capital funding in Silicon Valley and Boston fuels start-ups developing optics and driver ICs, which in turn elevates local sourcing of prototype displays. Defense procurement, led by programs such as the F-35 helmet upgrade, adds a stable layer to North American oled microdisplay market purchases.

Europe focuses on automotive rollouts and high-margin medical visualization. German and French tier-one suppliers work with panel makers to co-design low-latency interfaces for automotive head-up implementations. The Middle East & Africa region, although starting from a small base, is pacing at a 42% CAGR due to defense-modernization budgets and luxury-vehicle imports that include advanced AR-HUDs. South America remains largely consumer-oriented, with gradual opportunities arising from local camera production and burgeoning gaming communities.

- Sony Semiconductor Solutions Corp.

- Seiko Epson Corporation

- Kopin Corporation

- eMagin Corporation

- Yunnan Olightek Opto-Electronic Technology

- Microoled SA

- WiseChip Semiconductor Inc.

- Fraunhofer FEP

- Sunlike Display Technology

- BOE Technology Group Co., Ltd.

- Raysolve Technology

- SeeYA Technology

- AUO Corporation

- Dresden Microdisplay GmbH

- Jasper Display Corp.

- Himax Technologies, Inc.

- United Microdisplay Partners

- HC SemiTek Corporation

- Plessey Semiconductors

- OLiGHTEK Optoelectronics Kunming Co.

- Truly Semiconductors Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of OLED-on-Silicon (OLEDoS) capacity by Chinese Foundries

- 4.2.2 Accelerated Adoption of MicroOLED in Military Helmet-Mounted Displays across North America

- 4.2.3 Automotive OEM Integration of AR Head-Up Displays Using MicroOLED Panels in Europe

- 4.2.4 Surge in High-End Mirrorless Camera EVFs in Japan and South Korea

- 4.2.5 Growing VC Funding for AR/VR Start-ups Focused on OLED Microdisplays in the United States and Israel

- 4.2.6 Cost-Performance Advantage over MicroLED in <0.7-inch, >3,000 ppi Range

- 4.3 Market Restraints

- 4.3.1 Moisture-Ingress Encapsulation Challenges for OLEDoS

- 4.3.2 Sub-1,000 cd/m2 Brightness Ceiling versus MicroLED

- 4.3.3 Supply-Chain Concentration in Japan-China Creating Geopolitical Risk

- 4.3.4 Rapid Product Obsolescence Increasing OEM Inventory Risk

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Type

- 5.1.1 Near-to-Eye (NTE)

- 5.1.2 Projection

- 5.1.3 Electronic Viewfinder (EVF)

- 5.2 By Resolution

- 5.2.1 SVGA and Below (<=800 X 600)

- 5.2.2 XGA (1,024 X 768)

- 5.2.3 HD (720p)

- 5.2.4 Full HD (1080p)

- 5.2.5 Above FHD (2K-4K-Plus)

- 5.3 By Technology

- 5.3.1 RGB OLED-on-Silicon

- 5.3.2 White OLED + Color Filter

- 5.3.3 AMOLED on Glass

- 5.3.4 Top-Emitting OLED

- 5.4 By Panel Size (Diagonal)

- 5.4.1 <0.5 inch

- 5.4.2 0.5-1.0 inch

- 5.4.3 >1.0 inch

- 5.5 By End-User Industry

- 5.5.1 Consumer Electronics

- 5.5.1.1 AR/VR Headsets

- 5.5.1.2 Digital Cameras and Camcorders

- 5.5.1.3 Smart Wearables

- 5.5.2 Automotive

- 5.5.2.1 AR Head-Up Displays

- 5.5.2.2 Side-Mirror Replacement Displays

- 5.5.3 Healthcare

- 5.5.3.1 Surgical and Diagnostic Wearables

- 5.5.3.2 Medical Imaging Devices

- 5.5.4 Industrial and Enterprise

- 5.5.4.1 Smart Glasses

- 5.5.4.2 Machine Vision Systems

- 5.5.5 Aerospace and Defense

- 5.5.5.1 Helmet-Mounted Displays

- 5.5.5.2 Weapon and Thermal Sights

- 5.5.6 Law Enforcement and Security

- 5.5.6.1 Night-Vision Goggles

- 5.5.6.2 Body-Worn Cameras

- 5.5.7 Others (Research and Education)

- 5.5.1 Consumer Electronics

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 South Korea

- 5.6.3.4 India

- 5.6.3.5 South East Asia

- 5.6.3.6 Australia

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Sony Semiconductor Solutions Corp.

- 6.4.2 Seiko Epson Corporation

- 6.4.3 Kopin Corporation

- 6.4.4 eMagin Corporation

- 6.4.5 Yunnan Olightek Opto-Electronic Technology

- 6.4.6 Microoled SA

- 6.4.7 WiseChip Semiconductor Inc.

- 6.4.8 Fraunhofer FEP

- 6.4.9 Sunlike Display Technology

- 6.4.10 BOE Technology Group Co., Ltd.

- 6.4.11 Raysolve Technology

- 6.4.12 SeeYA Technology

- 6.4.13 AUO Corporation

- 6.4.14 Dresden Microdisplay GmbH

- 6.4.15 Jasper Display Corp.

- 6.4.16 Himax Technologies, Inc.

- 6.4.17 United Microdisplay Partners

- 6.4.18 HC SemiTek Corporation

- 6.4.19 Plessey Semiconductors

- 6.4.20 OLiGHTEK Optoelectronics Kunming Co.

- 6.4.21 Truly Semiconductors Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment