PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066489

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066489

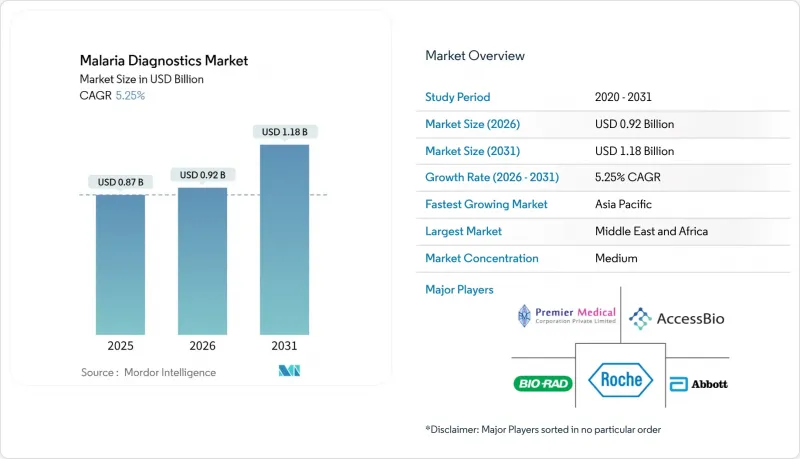

Malaria Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the malaria diagnostics market size is projected to expand from USD 0.87 billion in 2025 and USD 0.92 billion in 2026 to USD 1.18 billion by 2031, registering a CAGR of 5.25% between 2026 to 2031.

This report is Segmented by Technology (Microscopy, Rdts [HRP2-Based Pf-Only RDTs, and More], Molecular Diagnostics [qPCR / Conventional PCR, and More], Next-Gen Platforms), End-User (Hospitals, Clinics, Diagnostic Centres, Community Health Posts), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Malaria Diagnostics Market Trends and Insights

High Malaria Burden in Sub-Saharan Africa & Southeast Asia

Sub-Saharan Africa reported 265 million of the 282 million global malaria cases in 2024, anchoring 72% of worldwide diagnostic demand. India and Myanmar added a combined 2.3 million cases, but stronger laboratory infrastructure in these countries is accelerating molecular adoption. Persistent high case loads despite USD 3.1 billion in annual donor outlays highlight lingering diagnostic sensitivity gaps at low parasitaemia. Molecular platforms detecting as few as 10 parasites per microliter are therefore gaining traction. Vendors segment portfolios accordingly: high-sensitivity molecular systems are pushed into pre-elimination pockets, while cost-optimized RDTs saturate hyperendemic districts. Although molecular kits represented only 15% of unit volumes in 2025, they delivered 22% of revenue due to 8-12X higher average selling prices.

Large-Scale Donor & Government Funding for RDT Procurement

The Global Fund and the President's Malaria Initiative financed 72% of RDT purchases in sub-Saharan Africa during 2024. The current 2024-2026 allocation cycle earmarks USD 1.2 billion for diagnostics, 68% of which targets dual-target RDTs that detect both HRP2 and Pf-LDH antigens. PMI's 27-country footprint now directs incremental dollars toward community-level molecular testing in Zambia and Senegal. Proposed U.S. fiscal 2026 cuts could trim procurement volumes by 6 million tests, disproportionately affecting import-dependent nations. Vendors with WHO prequalification-Abbott, SD Biosensor, Access Bio-capture 78% of donor-funded tenders, reinforcing a two-tier market that limits scale for late entrants.

Patchy Healthcare Infrastructure in Remote Endemic Areas

A 2024 survey of 1,840 health posts across 12 African countries found 42% lacked reliable electricity and 67% had no refrigeration. Solar-powered molecular systems offer partial relief, yet their USD 4,500 price tags exceed annual diagnostic budgets in many rural districts. Seasonal road inaccessibility in Mozambique and Chad adds USD 0.40-0.80 per test in logistics costs. These constraints anchor demand for low-cost RDTs even where they underperform, sustaining an urban-rural technology divide that weighs on the overall growth trajectory of the malaria diagnostics market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Technological Shifts Toward Molecular Point-of-Care Platforms

- HRP2-Deletion Hot-Spots Accelerating Switch to Pf-LDH / Dual-Target RDTs

- Persistent False-Negative Risk at Low Parasitaemia

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rapid diagnostic tests captured 61.18% of the malaria diagnostics market size in 2025, maintaining leadership on unit volumes thanks to donor-funded purchases. However, molecular diagnostics are climbing at a 5.81% CAGR as LAMP and CRISPR formats reach field operability without refrigerated supply chains. Within the molecular cluster, LAMP systems already hold the dominant malaria diagnostics market share because of WHO prequalification and demonstrated 98.7% sensitivity at 10 parasites per microliter.

Hemozoin biosensors and AI-assisted digital microscopy occupy early-adoption niches, yet their growth outpaces the overall malaria diagnostics market. Field data from Uganda showed hemozoin magnetic sensors achieving 92% sensitivity, encouraging uptake in HRP2-deletion areas. Hybrid workflows that triage patients with RDTs before confirmatory molecular or AI-microscopy tests are scaling in district hospitals, compressing diagnostic turnaround times and limiting overtreatment costs.

Geography Analysis

Middle East and Africa anchored 81.15% of global revenue in 2025, propelled by 265 million cases and donor funding that pays for 72% of diagnostic purchases. Nigeria, the Democratic Republic of Congo, Uganda, and Mozambique together consume the largest share of RDT volumes. Pre-elimination countries such as Zambia and Senegal are adopting LAMP at scale-1,800 units were deployed across 420 facilities in 2025-signaling an incipient shift from microscopy to molecular confirmation. HRP2-deletion hotspots in Eritrea and Ethiopia have forced a rapid pivot to costlier dual-target RDTs, tightening margins for vendors lacking alternative antigen portfolios.

Asia-Pacific is the fastest-growing region at a 6.98% CAGR, buoyed by India's 1.9 million cases and a fiscal 2025-2026 commitment of INR 2.4 billion (USD 29 million) for diagnostics. China's post-elimination surveillance sustains a USD 12 million micro-market for imported case detection. Southeast Asian countries are pivoting to molecular active-case detection; a Cambodian trial showed LAMP detecting 3.2X more infections than RDT screening in low-transmission villages. South America remains a niche but strategic geography where Brazil and Peru deploy dual-target RDTs to counter HRP2 deletions exceeding 15% in the Amazon basin.

- Abbott Laboratories

- Access Bio

- Advy Chemical

- Atlas Medical

- bioMerieux

- Bio-Rad Laboratories

- Danaher Corp. (Beckman Coulter)

- Global Access Diagnostics

- Human Diagnostics

- Meridian Bioscience

- Premier Medical Corporation

- QIAGEN

- QuantuMDx

- QuidelOrtho (Ortho Clinical Diagnostics)

- Roche

- SD Biosensor Inc.

- Siemens Healthineers

- Sysmex Partec GmbH

- Thermo Fisher Scientific

- Zeesan Biotech

- Zephyr Biomedicals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High malaria burden in sub-Saharan Africa & SE-Asia

- 4.2.2 Large-scale donor & government funding for RDT procurement

- 4.2.3 Rapid technological shifts towards molecular PoC platforms

- 4.2.4 HRP2-deletion hot-spots accelerating switch to Pf-LDH / dual-target RDTs

- 4.2.5 AI-enabled portable digital microscopy reducing skills bottleneck

- 4.3 Market Restraints

- 4.3.1 Patchy healthcare infrastructure in remote endemic areas

- 4.3.2 Persistent false-negative risk at low parasitaemia

- 4.3.3 Covid-19-driven reallocation of RDT production capacity

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technology

- 5.1.1 Microscopy

- 5.1.2 Rapid Diagnostic Tests (RDTs)

- 5.1.2.1 HRP2-based Pf-only RDTs

- 5.1.2.2 Pf-LDH / Dual-Target RDTs

- 5.1.2.3 Multiplex Pan-Plasmodium RDTs

- 5.1.3 Molecular Diagnostics

- 5.1.3.1 qPCR / Conventional PCR

- 5.1.3.2 LAMP / Isothermal NAAT

- 5.1.3.3 CRISPR-based NAAT

- 5.1.4 Next-Gen Platforms

- 5.1.4.1 Hemozoin Biosensor Devices

- 5.1.4.2 Mobile Phone-Integrated Readers

- 5.2 By End-User

- 5.2.1 Hospitals

- 5.2.2 Clinics

- 5.2.3 Diagnostic Centres

- 5.2.4 Community Health Posts

- 5.2.5 Other End Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Access Bio Inc.

- 6.3.3 Advy Chemical

- 6.3.4 Atlas Medical

- 6.3.5 bioMerieux SA

- 6.3.6 Bio-Rad Laboratories

- 6.3.7 Danaher Corp. (Beckman Coulter)

- 6.3.8 Global Access Diagnostics

- 6.3.9 Human Diagnostics

- 6.3.10 Meridian Bioscience

- 6.3.11 Premier Medical Corporation

- 6.3.12 Qiagen N.V.

- 6.3.13 QuantuMDx

- 6.3.14 QuidelOrtho (Ortho Clinical Diagnostics)

- 6.3.15 Roche Diagnostics

- 6.3.16 SD Biosensor Inc.

- 6.3.17 Siemens Healthineers

- 6.3.18 Sysmex Partec GmbH

- 6.3.19 Thermo Fisher Scientific

- 6.3.20 Zeesan Biotech

- 6.3.21 Zephyr Biomedicals

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment