PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850306

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850306

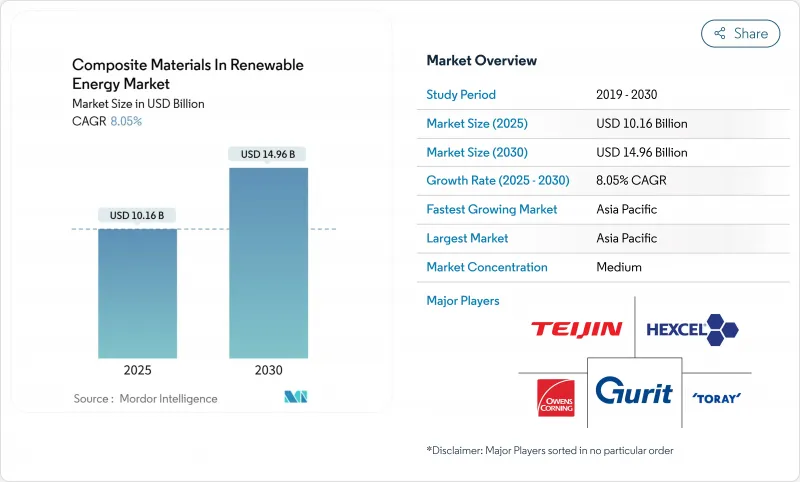

Composite Materials In Renewable Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The composite materials in the renewable energy market were valued at USD 10.16 billion in 2025 and are forecast to expand at an 8.05% CAGR, reaching USD 14.96 billion by 2030.

Rapid capacity additions in wind, solar, and hydrogen projects demand lighter, stronger structures that extend component lifetimes and shrink carbon footprints. Government clean-energy mandates, breakthroughs in recyclable thermoplastic platforms, and the need for lightweight materials that endure harsh offshore and desert climates combine to accelerate procurement cycles. Automated fibre placement, 3D printing, and other Industry 4.0 processes are compressing production timelines while trimming manufacturing scrap. At the same time, vertically integrated suppliers are consolidating fibre spinning, resin synthesis, and part fabrication to secure critical inputs amid supply-chain tension. These intersecting forces position the composite materials in the renewable energy market for a decade of steady, innovation-driven growth.

Global Composite Materials In Renewable Energy Market Trends and Insights

Reduced Weight Versus Metallic Structures

Composite substitution cuts structural mass in offshore wind, hydrogen tanks, and tidal devices, boosting payload efficiency and easing transport logistics. Weight savings of 13.76% on tidal blades have lifted power output by 46.1% versus steel alternatives. In aerospace, the development of liner-less Type V carbon-composite tanks supports the transition to liquid-hydrogen propulsion, indirectly increasing demand for renewable-grade fibres. Mitsubishi Chemical's C/SiC ceramic matrix composite endures 1,500 °C, opening paths for heliostat receivers and fusion-reactor hardware. These advances underline why the composite materials in the renewable energy market continue to displace aluminum and steel in high-temperature, corrosive environments.

Growing Demand for Longer Wind-Turbine Blades

Siemens Energy's 21 MW prototype with a 276 m rotor diameter illustrates how blade lengths nearing 150 m require carbon-fibre spar caps for stiffness-to-weight targets unattainable with glass fibre alone. Segmented blade architectures, enabled by high-toughness epoxy joints, ease transport while maintaining aeroelastic integrity. The ZEBRA consortium completed the world's largest fully recyclable thermoplastic blade using Arkema's Elium resin, signalling industrial readiness for closed-loop platforms. Hybrid lay-ups that mix natural and synthetic fibres improve impact resistance and lower embodied carbon, aligning with EU offshore wind targets of 150 GW by 2050 that could double global carbon-fibre demand.

High Research and Development and Tooling CAPEX

Automated fibre-placement lines cost USD 5-10 million each, while molds for >100 m blades exceed USD 2 million per set, tying up capital for years before payback. Certification programs often run 5-7 years, stretching working-capital needs for mid-tier innovators. Hexcel's USD 300 million bond issue in 2025 exemplifies the financial firepower required to retain process-technology leadership. Thermoplastic adoption compounds costs, since ovens, presses, and welding equipment differ from thermoset lines, creating parallel asset footprints that hamper small manufacturers' competitiveness.

Other drivers and restraints analyzed in the detailed report include:

- Government Inclination Towards Adoption of Renewable Energy

- Commercialization of Thermoplastic Recyclable Blade Platforms

- Recycling & Landfill-Ban Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The segment generated the largest revenue contribution in 2024, when GFRP held 55.25% of composite materials in the renewable energy market share. Carbon fibre's 8.62% CAGR reflects rotor diameters that eclipse 120 m, where stiffness and fatigue performance justify its 5-10X cost premium. SGL Carbon's supply agreements for 80 m-plus blades illustrate vertical moves into energy from aerospace. Fibre-hybrid lay-ups blending basalt and natural fibre reduce embodied carbon yet maintain required modulus, expanding options for mid-range turbine classes. Bio-based lignin fibre research in Germany offers a future cost-reduction lever, although commercial volumes remain limited. Recycled carbon fibre is steadily integrating into secondary structures as mechanical recycling preserves 60-70% original tensile strength, further diversifying feedstocks and tempering raw material price swings.

Epoxy maintained a 45.86% revenue share in 2024 thanks to mature supply chains and high fatigue resistance. Yet bio-resins and recycled resins are expanding at an 8.04% CAGR as OEMs race to satisfy circular-economy mandates. Dow and Vestas have qualified polyurethane spar-cap chemistries that enable rapid pultrusion while elevating interlaminar toughness. Sicomin's SGi 128 bio-epoxy gel coat demonstrates fire-safe solutions with 35% renewable content. Thermoplastic matrices such as Elium offer the added benefit of repairability and melt recycling, pivoting the composite materials in the renewable energy market toward closed-loop economics.

The Composite Materials in Renewable Energy Market Report Segments the Industry by Fibre Type (Glass-Fibre-Reinforced Plastics (GFRP), and More), Resin Matrix (Epoxy, Polyester, and More), Manufacturing Process (Vacuum Infusion, Prepreg/Autoclave, and More), Application (Wind Power, Solar Power, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 44.68% of the composite materials in the renewable energy market size in 2024 and is on track for an 8.12% CAGR through 2030. China anchors the region with end-to-end supply chains, yet its 2024 recycling standards raise compliance costs that favor integrated local champions. India's USD 2.4 billion Hydrogen Mission and defense-sector carbon-fibre push reinforce domestic production incentives. Japan's perovskite roadmap aims for 38.3 GW by 2040 via flexible composite substrates, a pivot that may recalibrate global solar module architectures. South Korea leverages shipbuilding know-how to enter offshore wind composites, while Australia tests floating solar on inland reservoirs, showcasing regional diversity in end-use cases.

North America benefits from USD 369 billion of Inflation Reduction Act funding, with domestic-content bonuses catalyzing plant expansion in Texas, New York, and Ontario. GE Vernova's USD 600 million manufacturing buildout exemplifies reshoring moves that cut trans-Pacific logistics risk. Canada's aerospace-composite cluster supports the transfer of out-of-autoclave methods to tidal-turbine shells, while Mexico's cost-competitive labor pool draws pultruders for solar-rack exports. The region's challenge is scaling fibre production to prevent over-dependence on imports, a gap several joint ventures aim to close by 2027.

Europe wields regulatory clout, steering global norms on recyclability and embodied carbon. The ZEBRA project's thermoplastic blade success positions the continent as a technology frontrunner. Germany's lignin-fibre pilot lines symbolize R&D leadership, whereas France leverages aerospace heritage to refine high-modulus prepregs. The UK National Composites Centre's SusWIND program validates multiple recycling routes, giving OEMs design flexibility. Offshore wind buildout in the North Sea and Baltic drives sustained fibre demand, though high energy costs compel automation to defend margins.

- Changzhou Tiansheng New Materials Co. Ltd

- EPSILON Composite SAS

- EURO-COMPOSITES

- Evonik Industries AG

- Exel Composites

- GE Vernova

- Gurit Services AG

- Jiangsu Hengshen Co.,Ltd

- Hexcel Corporation

- HS HYOSUNG ADVANCED MATERIALS

- LM WIND POWER

- Mitsubishi Chemical Group Corporation

- Norco Composites & GRP

- Owens Corning

- Plastic Reinforcement Fabrics Ltd

- SGL Carbon

- Siemens Gamesa Renewable Energy, S.A.U

- Solvay

- TEIJIN LIMITED

- TORAY INDUSTRIES, INC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Reduced weight versus metallic structures

- 4.2.2 Growing demand for longer wind-turbine blades

- 4.2.3 Government inclination towards the adoption of renwable energy

- 4.2.4 Commercialisation of thermoplastic recyclable blade platforms

- 4.2.5 Rising adoption of 3-D printed composite parts in floating solar & tidal devices

- 4.3 Market Restraints

- 4.3.1 High research and development and tooling CAPEX

- 4.3.2 Recycling & landfill-ban compliance costs

- 4.3.3 Concerns regarding the durability and fire resistance of some composite materials

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Fibre Type

- 5.1.1 Glass-Fibre-Reinforced Plastics (GFRP)

- 5.1.2 Carbon-Fibre-Reinforced Plastics (CFRP)

- 5.1.3 Fibre-Reinforced Polymers (FRP)

- 5.1.4 Other Fibre Types (Hybrid and Other Fibres, etc.)

- 5.2 By Resin Matrix

- 5.2.1 Epoxy

- 5.2.2 Polyester

- 5.2.3 Polyurethane

- 5.2.4 Thermoplastic

- 5.2.5 Bio-resins and Recycled Resins

- 5.3 By Manufacturing Process

- 5.3.1 Vacuum Infusion

- 5.3.2 Prepreg/Autoclave

- 5.3.3 Pultrusion

- 5.3.4 Automated Fibre Placement / 3-D Printing

- 5.3.5 Compression Moulding (SMC, BMC)

- 5.4 By Application

- 5.4.1 Wind Power

- 5.4.2 Solar Power

- 5.4.3 Hydroelectricity

- 5.4.4 Other Applications (Green-Hydrogen & Energy-Storage Vessels)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Changzhou Tiansheng New Materials Co. Ltd

- 6.4.2 EPSILON Composite SAS

- 6.4.3 EURO-COMPOSITES

- 6.4.4 Evonik Industries AG

- 6.4.5 Exel Composites

- 6.4.6 GE Vernova

- 6.4.7 Gurit Services AG

- 6.4.8 Jiangsu Hengshen Co.,Ltd

- 6.4.9 Hexcel Corporation

- 6.4.10 HS HYOSUNG ADVANCED MATERIALS

- 6.4.11 LM WIND POWER

- 6.4.12 Mitsubishi Chemical Group Corporation

- 6.4.13 Norco Composites & GRP

- 6.4.14 Owens Corning

- 6.4.15 Plastic Reinforcement Fabrics Ltd

- 6.4.16 SGL Carbon

- 6.4.17 Siemens Gamesa Renewable Energy, S.A.U

- 6.4.18 Solvay

- 6.4.19 TEIJIN LIMITED

- 6.4.20 TORAY INDUSTRIES, INC.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment