PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850322

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850322

Password Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

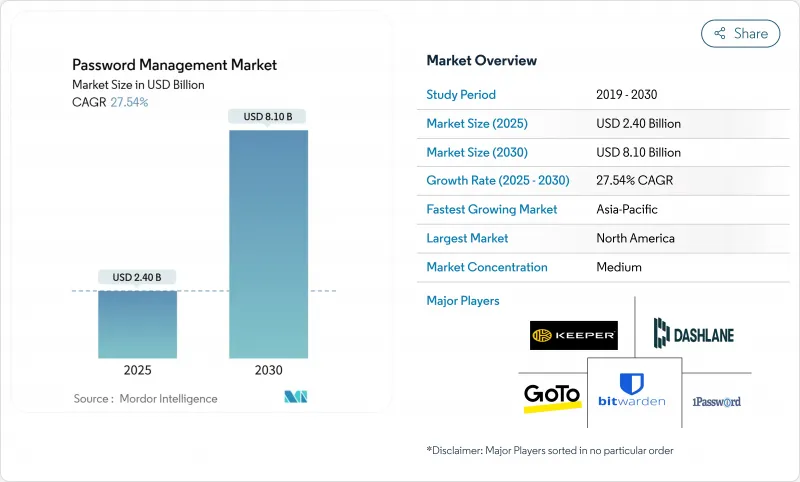

The password manager market size sits at USD 2.40 billion in 2025 and is forecast to climb to USD 8.10 billion by 2030, reflecting a powerful 27.54% CAGR that underscores how credential protection has become a frontline cyber-risk priority.

Growth is underpinned by the pivot from single-purpose vaults to platforms that orchestrate privileged access, automate audit evidence, and enable passwordless journeys through FIDO2 and passkeys. Enterprises are tightening identity controls in response to insurer mandates, zero-trust reference architectures, and a relentless rise in SaaS adoption. Competitive intensity is escalating as open-source offerings win mindshare on transparency, while incumbent vendors race to bundle privilege management, secrets automation, and SaaS discovery into one experience. The resulting innovation cycle is expanding the addressable opportunity in the business segment even as consumer demand moderates.

Global Password Management Market Trends and Insights

Zero-trust programs driving privileged vault rollouts

Financial institutions in North America are refactoring security baselines around "never trust, always verify." In 2024, 90% of organizations reported at least one identity breach, with 31% tied to weak oversight of privileged credentials. Regulators and boards now treat privileged access management as foundational, pushing banks to modernize static vaults with real-time rotation, just-in-time elevation and high-assurance secrets delivery. SSH's partnership with CYE illustrates the shift: vendors bundle risk quantification with passwordless channels to satisfy operational resilience rules. The immediate result is a budget reallocation from network tools to identity security platforms, positioning the password manager market for outsized growth in the privileged tier.

EU GDPR & NIS-2 mandated password audits

The NIS-2 directive obliges critical-sector entities to enforce MFA, unify credential policies and demonstrate continuous compliance. A European Cyber Security Organisation survey confirms that inconsistent national rules create execution pain points. Enterprises therefore deploy centrally managed vaults that collect evidence for auditors, reconcile legacy standards and cut remediation cycles. Hypervault highlights how automated rotation paired with granular reports lowers breach risk and audit costs hypervault.com. Heightened scrutiny compresses the procurement timeline, boosting near-term revenue visibility for vendors serving Europe-based headquarters and global subsidiaries alike.

High-profile breaches eroding trust

The 2022 breach at LastPass and fresh compromises at PowerSchool and TalkTalk in January 2025 reignited skepticism toward centralized vaults. Privacy-sensitive DACH buyers display heightened due diligence, amplifying churn risk. Open-source vendors address the concern by publishing cryptographic audits, yet buyers still weigh regulatory penalties against operational gains. Market growth slows temporarily as committees reassess vendor selection, driving an emphasis on zero-knowledge architectures and independent certifications.

Other drivers and restraints analyzed in the detailed report include:

- SaaS identity sprawl accelerating cross-platform vault demand

- Cyber-insurance underwriting demanding automated credential hygiene

- Rapid passkey/FIDO2 adoption shrinking consumer TAM

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Self-Service products retaining a 65% grip on the password manager market. Privileged User Password Management, however, is expanding at a 28% CAGR, pushed by zero-trust directives and auditor scrutiny over administrator rights. The differential implies that password manager market size allocations will skew toward privilege controls, even as self-service features remain table stakes.

Enterprises view privileged identity as the new blast radius. One Identity surfaced Cloud PAM Essentials in 2024, bundling discovery, session isolation and compliance analytics. Administration teams elevate vaults into incident-response platforms, correlating access events with SIEM telemetry. As risk officers quantify breach costs, budgets flow into privilege-centric offerings that can wrap high-value secrets with adaptive authentication and immutable audit trails.

Desktop clients still generated half of 2024 revenue, yet mobile subscriptions are on a 29.8% CAGR, confirming the smartphone's rise as a secure authenticator. Enhanced biometrics and hardware enclaves deepen assurance, while cross-device sync counters user friction. A notable 73% BYOD penetration in Nordic and North American companies. accelerates uptake. Vendors elevate mobile as the passkey companion, embedding WebAuthn APIs and push-to-approve workflows.

Industry response to the AutoSpill flaw spurred rapid patch cycles and injected password manager industry confidence by demonstrating transparent coordination among vendors. As users couple vaults with native biometrics, the handset transforms into the launchpad for next-generation multi-factor flows, widening the mobile revenue corridor.

The Password Management Market is Segmented by Solution Type (Self-Service Password Management, and More), Technology Type (Desktop, and More), Deployment Mode (Cloud-Hosted, and More), Enterprise Size (Large Enterprises, and More), End-User Vertical (BFSI, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America wields the largest regional footprint at 38% of 2024 revenue, buoyed by early zero-trust adoption, stringent breach disclosure laws and insurance oversight. Cyber-insurers tie policy eligibility to demonstrable vault usage, converting risk managers into de facto sales champions. Nevertheless, headline breaches temporarily check enterprise enthusiasm, reinforcing the need for transparent cryptographic design and third-party attestations.

Asia Pacific delivers the sharpest trajectory with a 28.1% CAGR. Rapid SaaS onboarding multiplies credential stores, turning password hygiene into a foundational pillar of digital-economy policy. Government frameworks in Australia and Japan explicitly list vaulting in critical infrastructure baselines, and enterprises leverage locally hosted clusters to satisfy data-residency clauses. Startup ecosystems in India and Singapore embed vault SDKs directly into fintech stacks, expanding the password manager market addressable base.

Europe's profile is regulatory-driven. GDPR and NIS-2 transform vault procurement from discretionary to mandatory in critical sectors. Fragmented national interpretations complicate rollout, but pan-European platforms capture scale advantage by offering policy templates aligned to each supervisory authority. The DACH region, while cautious, rewards vendors that expose source code or commission independent audits, a stance that plays to open-source strengths.

Middle East and Africa register double-digit expansion as digital-nation initiatives progress. Sovereignty demands push the hybrid narrative: UAE pilots demonstrate that localized SaaS nodes can coexist with global support networks. Saudi Arabia's Vision 2030 budgets elevate identity security line items, signaling longer-run upside for best-practice vaults.

- LastPass (GoTo)

- 1Password (AgileBits)

- Dashlane

- Keeper Security

- Bitwarden

- CyberArk Software

- Delinea (Centrify/Thycotic)

- Microsoft

- IBM

- Apple Inc.

- CA Technologies (Broadcom)

- Okta Inc.

- SailPoint Technologies

- Quest Software

- Hitachi ID Systems

- FastPassCorp A/S

- Avatier

- Trend Micro

- Ivanti

- Steganos GmbH

- AceBIT GmbH

- Siber Systems (RoboForm)

- EmpowerID

- Intuitive Security Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Zero-Trust Programs Accelerating Privileged Password Vault Deployments in North American BFSI

- 4.2.2 EU GDPR & NIS-2 Mandates Triggering Enterprise-wide Password Audits and Upgrades

- 4.2.3 Surge in SaaS Identity Sprawl Creating Demand for Cross-Platform Vaults in APAC Mid-market

- 4.2.4 Workforce Mobility & BYOD Driving Mobile-First Password Managers in Nordics

- 4.2.5 Cyber-Insurance Underwriting Requiring Automated Credential Hygiene Proof in U.S.

- 4.2.6 Open-Source Security Audits (e.g., Argon-2, PBKDF2) Elevating Trust in Community-Led Tools

- 4.3 Market Restraints

- 4.3.1 High-Profile Breaches (e.g., LastPass 2022) Undermining User Trust, Especially in DACH Region

- 4.3.2 Rising Adoption of Passkeys/FIDO2 Reducing Future TAM in Consumer Segment

- 4.3.3 Regulatory Data-Residency Rules Complicating Cloud Vault Roll-Outs in MENA

- 4.3.4 Persistent Shadow-IT Password Stores Inflating Migration Costs for Large Enterprises

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porters Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Industry Value-Chain Analysis

- 4.8 Impact of COVID-19 & Hybrid Work Patterns

5 MARKET SIZE & GROWTH FORECASTS (VALUE, USD)

- 5.1 By Solution Type

- 5.1.1 Self-Service Password Management

- 5.1.2 Privileged User Password Management

- 5.2 By Access/Technology Type

- 5.2.1 Desktop

- 5.2.2 Mobile Devices

- 5.2.3 Voice-Enabled Password Reset

- 5.2.4 Browser Extensions & Web Vaults

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Hosted

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small & Medium Enterprises (SMEs)

- 5.5 By End-user Vertical

- 5.5.1 Banking, Financial Services & Insurance (BFSI)

- 5.5.2 Healthcare & Life Sciences

- 5.5.3 IT & Telecommunications

- 5.5.4 Government & Public Sector

- 5.5.5 Retail & E-commerce

- 5.5.6 Manufacturing

- 5.5.7 Education

- 5.5.8 Other Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Nordics

- 5.6.3.5 Rest of Europe

- 5.6.4 Middle East

- 5.6.4.1 GCC

- 5.6.4.2 Turkey

- 5.6.4.3 Israel

- 5.6.4.4 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Nigeria

- 5.6.5.3 Rest of Africa

- 5.6.6 Asia

- 5.6.6.1 China

- 5.6.6.2 India

- 5.6.6.3 Japan

- 5.6.6.4 South Korea

- 5.6.6.5 Southeast Asia

- 5.6.7 Oceania

- 5.6.7.1 Australia

- 5.6.7.2 New Zealand

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 LastPass (GoTo)

- 6.4.2 1Password (AgileBits)

- 6.4.3 Dashlane

- 6.4.4 Keeper Security

- 6.4.5 Bitwarden

- 6.4.6 CyberArk Software

- 6.4.7 Delinea (Centrify/Thycotic)

- 6.4.8 Microsoft

- 6.4.9 IBM

- 6.4.10 Apple Inc.

- 6.4.11 CA Technologies (Broadcom)

- 6.4.12 Okta Inc.

- 6.4.13 SailPoint Technologies

- 6.4.14 Quest Software

- 6.4.15 Hitachi ID Systems

- 6.4.16 FastPassCorp A/S

- 6.4.17 Avatier

- 6.4.18 Trend Micro

- 6.4.19 Ivanti

- 6.4.20 Steganos GmbH

- 6.4.21 AceBIT GmbH

- 6.4.22 Siber Systems (RoboForm)

- 6.4.23 EmpowerID

- 6.4.24 Intuitive Security Systems

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-Space & Unmet-Need Assessment