PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850326

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850326

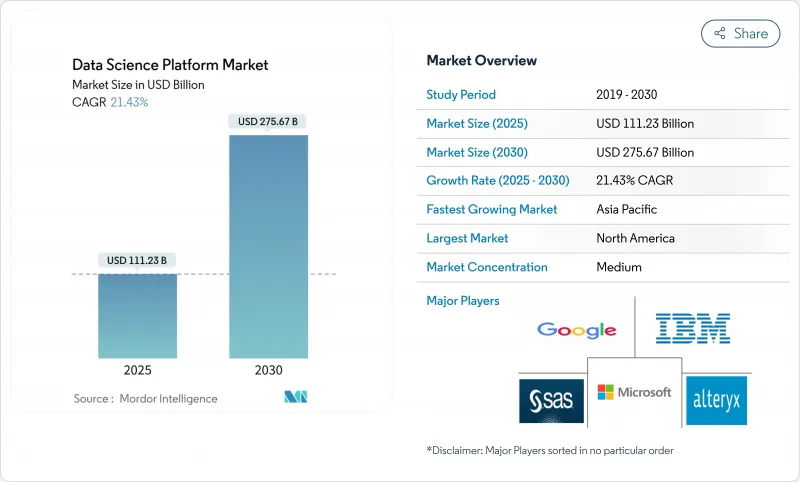

Data Science Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The data science platform market size is valued at USD 111.23 billion in 2025 and is forecast to climb to USD 275.67 billion in 2030, advancing at a 21.43% CAGR.

Demand escalates as enterprises consolidate machine-learning operations, data engineering, and business-intelligence workflows on a single stack that satisfies tighter governance rules under the EU AI Act and similar frameworks. Momentum also stems from growing edge-to-cloud fabrics that accommodate unstructured IoT and video streams, the need for scalable feature stores, and cloud providers' rollout of high-density GPU instances. North American leadership remains anchored in mature cloud infrastructure, while Asia-Pacific's accelerating investment in generative AI and data-center capacity underpins its status as the fastest-growing region. Competitive intensity is rising as hyperscalers embed native AI tooling and specialist vendors differentiate through open-format data sharing, hybrid deployment, and domain-specific accelerators.

Global Data Science Platform Market Trends and Insights

Proliferation of Open-Source ML Frameworks Catalyzing Platform Convergence

TensorFlow and PyTorch have evolved into full-stack ecosystems that cut model-prototyping time and simplify distributed training, encouraging enterprises to shift from bespoke stacks to vendor-managed platforms that remain framework agnostic. The resulting convergence allows mid-market firms to plug into unified environments without heavy engineering overhead, accelerating time-to-value. Patent families addressing AI/ML infrastructure climbed 45% year-over-year, signaling continued innovation that platform providers harness to avoid vendor lock-in and bolster governance.

Stricter Model-Governance Regulations Triggering Managed-Platform Uptake

The EU AI Act, effective August 2024, imposes risk-management and audit-trail duties that favor turnkey platforms offering built-in compliance dashboards, automated documentation, and continuous monitoring. Extraterritorial reach compels non-EU firms to adopt similar capabilities to serve European customers, while penalties up to 7% of global turnover sharpen the cost of non-compliance. Government initiatives such as France's EUR 30 billion (USD 33 billion) AI fund strengthen demand for compliant infrastructure.

Data-Residency Barriers Hampering Multi-Region Roll-outs in EU Public Sector

GDPR and sovereignty rules force public entities to confine processing within national borders, complicating multinational deployments. The EU trails the US by USD 1.36 trillion in ICT investment, and 43% of cross-border SMEs struggle with location mandates that narrow vendor options to providers offering in-region hosting.

Other drivers and restraints analyzed in the detailed report include:

- Edge-to-Cloud Data-Fabric Adoption Enabling Hybrid Platforms in Manufacturing

- Explosion of Unstructured IoT and Video Data Requiring Scalable Feature Stores

- Shortage of MLOps Engineers Undermining Complex Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platforms contributed 72% of the data science platform market in 2024, reflecting enterprise appetite for integrated toolchains that cover ingestion to model monitoring. Yet services are expanding at a 24.3% CAGR as firms purchase advisory, customization, and managed capabilities to operationalize complex workloads. Vendor revenue models increasingly blend licenses with professional engagements to curb customer churn and assure compliance readiness.

Service momentum traces back to the MLOps skills gap: enterprises lacking deployment expertise outsource design, automation, and monitoring. As a result, the services slice of the data science platform market size is projected to widen steadily through 2030, reinforcing the ecosystem's shift from pure software sales to outcome-based partnerships.

Cloud deployments accounted for 78% of the data science platform market share in 2024, underpinned by the need for elastic GPU clusters and AI-optimized storage. Providers report that half of incremental infrastructure revenue since 2023 stems directly from generative AI workloads.

With a 21.9% CAGR ahead, cloud remains the primary engine of the data science platform market. On-premise and hybrid implementations persist in heavily regulated verticals, but even those users increasingly offload dev-test stages to the cloud while keeping production pipelines within sovereign zones. Edge nodes now form an adjunct layer, enabling latency-critical inference yet remaining orchestrated from centralized consoles.

Data Science Platform Market is Segmented by Offering (Platform, Services), Deployment (On-Premise, Cloud), Enterprise Size (Small and Medium Enterprises, Large Enterprises), End-User Industry (IT and Telecom, BFSI, Retail and E-Commerce, Manufacturing, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains 40% of the data science platform market share in 2024, bolstered by USD 68.4 billion in Q1 2025 cloud-service revenue from the top three hyperscalers. Venture funding, patent leadership, and a dense partner ecosystem nurture advanced deployments, though rising infrastructure costs push providers to bankroll record capital budgets exceeding USD 100 billion for additional capacity.

Asia-Pacific is the fastest expanding arena, growing at 25.7% CAGR on the back of China's generative-AI outlays and India's doubling data-center footprint. Regional data-center power surpassed 12 GW operational, providing the backbone for sustained expansion. Government programs such as Australia's Digital Economy Strategy and China's Three-Year Data Factor Action Plan create policy pull that underwrites platform adoption.

Europe sits at a regulatory crossroads: the EU AI Act fuels platform demand, yet a USD 1.36 trillion ICT investment gap plus sovereignty imperatives compel providers to build local hosting and encryption. Fragmented markets raise costs, but initiatives such as Germany's Industry 4.0 and France's AI stimulus (EUR 30 billion / USD 33 billion) incentivize compliant, sovereign-cloud solutions. Global sovereign-cloud spending is forecast to cross USD 250 billion by 2027.

- IBM Corporation

- Google LLC (Alphabet Inc.)

- Microsoft Corporation

- Alteryx Inc.

- SAS Institute Inc.

- Databricks Inc.

- Snowflake Inc.

- Amazon Web Services Inc.

- The MathWorks Inc.

- RapidMiner Inc.

- DataRobot Inc.

- H2O.ai

- TIBCO Software Inc.

- KNIME GmbH

- Domino Data Lab Inc.

- Oracle Corporation

- SAP SE

- Cloudera Inc.

- Qlik Tech International

- Altair Engineering Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Open-Source ML Frameworks Catalyzing Platform Convergence

- 4.2.2 Stricter Model-Governance Regulations (EU AI Act et al.) Triggering Managed-Platform Uptake

- 4.2.3 Edge-to-Cloud Data-Fabric Adoption Enabling Hybrid DS Platforms in Manufacturing)

- 4.2.4 Explosion of Unstructured IoT and Video Data Requiring Scalable Feature Stores Drives the Market

- 4.3 Market Restraints

- 4.3.1 Data-Residency Barriers Hampering Multi-Region Roll-outs in Public Sector EU

- 4.3.2 Shortage of ML-Ops Engineers Undermining Complex Deployments

- 4.3.3 Escalating Cloud Bills Creating Budget Pushback for Real-Time Training Workloads

- 4.3.4 Legacy Data Silos in Energy and Utilities Delaying Platform ROI

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of Macro Economic Trends on the Market

- 4.8 Key Use Cases

- 4.9 Ecosystem Analysis

- 4.10 Pricing and Pricing Models

- 4.11 Key Capabilities of Data Science Platforms (AI/ML, Analytics, Visualization, Exploration, Modelling)

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Offering

- 5.1.1 Platform

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Retail and E-commerce

- 5.4.4 Manufacturing

- 5.4.5 Energy and Utilities

- 5.4.6 Healthcare and Life Sciences

- 5.4.7 Government and Defense

- 5.4.8 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC

- 5.5.5.1.1.1 United Arab Emirates

- 5.5.5.1.1.2 Saudi Arabia

- 5.5.5.1.1.3 Qatar

- 5.5.5.1.1.4 Rest of GCC

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Vendor Ranking by Region

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Google LLC (Alphabet Inc.)

- 6.4.3 Microsoft Corporation

- 6.4.4 Alteryx Inc.

- 6.4.5 SAS Institute Inc.

- 6.4.6 Databricks Inc.

- 6.4.7 Snowflake Inc.

- 6.4.8 Amazon Web Services Inc.

- 6.4.9 The MathWorks Inc.

- 6.4.10 RapidMiner Inc.

- 6.4.11 DataRobot Inc.

- 6.4.12 H2O.ai

- 6.4.13 TIBCO Software Inc.

- 6.4.14 KNIME GmbH

- 6.4.15 Domino Data Lab Inc.

- 6.4.16 Oracle Corporation

- 6.4.17 SAP SE

- 6.4.18 Cloudera Inc.

- 6.4.19 Qlik Tech International

- 6.4.20 Altair Engineering Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment