PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850339

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850339

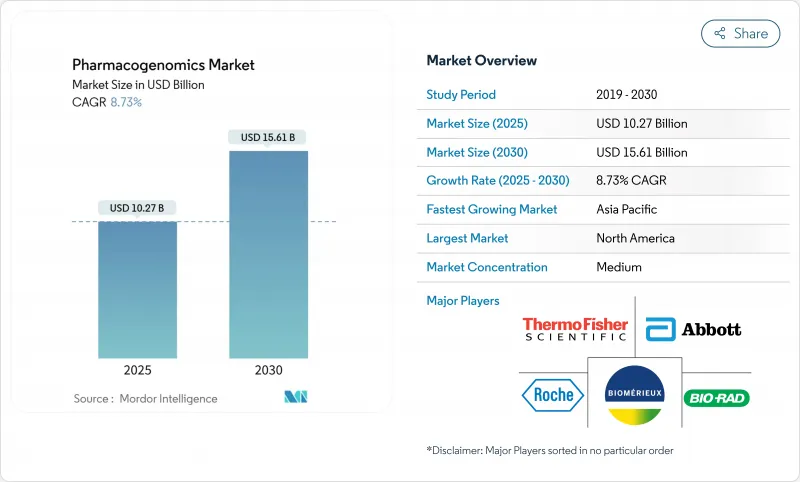

Pharmacogenomics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Pharmacogenomics Market size is estimated at USD 10.27 billion in 2025, and is expected to reach USD 15.61 billion by 2030, at a CAGR of 8.73% during the forecast period (2025-2030).

Clinical adoption is expanding as health systems weave pre-emptive genetic testing into routine workflows, trimming trial-and-error prescribing and lowering adverse reactions. Medicare's 2024 Local Coverage Determinations and the FDA's companion-diagnostic guidance have created clearer reimbursement and regulatory pathways, encouraging laboratories to scale capacity. Demand accelerates in pain management, where CYP2D6 testing supports opioid stewardship and posts the fastest segment CAGR of 13.75%. Asia-Pacific shows double-digit growth as China and India embed pharmacogenomic programs in national health strategies. Meanwhile, AI-driven software platforms shorten interpretation time and increasingly steer buying decisions for hospitals.

Global Pharmacogenomics Market Trends and Insights

Rising Demand for Personalized Medicine

Health systems now view genetic testing as core infrastructure because outcome data show 42% fewer prescribing adjustments and higher adherence when pre-emptive panels are used. The PREPARE multisite study reported a 33% drop in drug-related adverse events under pharmacogenomic guidance. Veterans Affairs has rolled out a nationwide program to align drug choice with veterans' genotypes, moving away from one-size-fits-all prescribing. These benefits underpin steady pharmacogenomics market growth even in budget-constrained systems. Data-rich implementation models also help payers quantify long-term savings, strengthening coverage proposals.

Advancements in Genetic Sequencing Technologies

Illumina's NovaSeq X has lowered per-sample costs while boosting throughput, making comprehensive panels affordable for community hospitals. Oxford Nanopore and PacBio long-read platforms now resolve CYP2D6 structural variants missed by earlier methods. A University of Illinois nanopore system compresses sequencing time from 2 weeks to 1 hour, cutting costs by 90% and enabling near-patient testing. Third-generation tools capture complex haplotypes in under-represented populations, closing equity gaps and expanding the addressable pharmacogenomics market. Faster, cheaper sequencing also frees budgets for informatics and counseling services.

High Costs Associated with Pharmacogenomic Testing

Comprehensive panels range from USD 200-2,000, creating affordability gaps for uninsured patients and small clinics. Rural providers also shoulder training and IT integration expenses, delaying roll-outs. Upfront investment in decision-support engines strains capital budgets, although modeling shows long-run savings from fewer adverse reactions. Bulk-purchasing consortia and machine-learning triage tools help curb per-test charges. Cost declines in reagents and sequencing hardware are expected to ease this restraint in the medium term.

Other drivers and restraints analyzed in the detailed report include:

- Growing Prevalence of Chronic and Genetic Diseases

- Increasing Research and Development Investments

- Limited Reimbursement Coverage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents and kits represented 44.34% of pharmacogenomics market share in 2024, underpinned by high test volumes and consumable pull-through. Yet software and services are expanding fastest at 11.01% CAGR, reflecting a pivot toward actionable insights over raw sequence data. Hospitals favor AI-assisted decision-support modules that plug directly into electronic health records, reducing interpretation time from hours to minutes. PGxAI's Deneb model exemplifies this shift by blending pharmacogenetic calls with drug-response algorithms to inform dosing adjustments. Instruments remain a steady contributor as vendors integrate sample prep, amplification and analytics into single bencheside units, easing workflow complexity.

The convergence of wet-lab and digital components is redefining solution bundles within the pharmacogenomics market. QIAGEN's QIAcuity digital PCR line added 100 assays in 2024 to support oncology, cardiology and pain panels. Service contracts now include tele-genetic counseling to meet accreditation standards for informed consent. As cloud infrastructure matures, subscription-based bioinformatics is displacing perpetual licenses, smoothing cash flow for both suppliers and clinics. These trends reinforce the pharmacogenomics market size trajectory by shifting revenue toward recurring analytics and support offerings.

DNA sequencing already commands 32.66% of pharmacogenomics market share and is projected to grow at 12.12% CAGR, lifted by falling reagent costs and richer variant detection. Illumina's NovaSeq X platform reduced per-genome costs, unlocking population-scale screening for large health networks. Long-read instruments from PacBio map complex CYP2D6 rearrangements critical for opioid dosing.

Microarrays remain relevant for high-throughput targeted panels, especially the Infinium Global Diversity Array with 1.9 million PGx markers. PCR assays win where rapid turnaround is vital, such as perioperative antiplatelet management. Mass-spectrometry and electrophoresis retain niche roles. The net effect is continued consolidation around multi-omics sequencing hubs, strengthening the pharmacogenomics market.

The Pharmacogenomics Market is Segmented by Product & Service (Instruments, Reagents & Kits, and More), Technology (Polymerase Chain Reaction, DNA Sequencing, and More), Sample Type (Blood, and More), Application (Drug Discovery & Development, Oncology, Neurology, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 41.91% of the pharmacogenomics market in 2024, underpinned by mature lab infrastructure, CPIC implementation resources and supportive FDA frameworks. Mayo Clinic and University of Colorado provide blueprints for workflow integration, while the Veterans Affairs program extends reach across 9 million enrollees. Nonetheless, payer variability persists, with UnitedHealthcare's 2024 coverage curbs dampening multigene panel uptake myriad.com.

Europe shows steady advances as the European Medicines Agency finalized AI-driven pharmacogenomic guidance in 2024, giving manufacturers clarity to scale companion-diagnostic submissions. National health services in France, Germany and the Nordics are piloting population panels to measure long-term cost offsets, promoting broader pharmacogenomics market penetration.

Asia-Pacific is the fastest-growing region, forecast at 14.75% CAGR. China's Five-Year Health Plan embeds pharmacogenomic screening into public hospitals and secures domestic sequencing supply chains. Indian start-ups like Acrannolife provide locally priced PGx bundles for cardiology and psychiatry. Singapore research found 46.1% of participants carried actionable CYP2D6 alleles, underscoring unmet need nature.com. Expansive population cohorts and diverse haplotypes augment global biomarker discovery pipelines, amplifying the overall pharmacogenomics market size.

- Abbott Laboratories

- Agilent Technologies

- Beckton Dickinson

- bioMerieux

- Bio-Rad Laboratories

- Eurofins

- Roche

- Illumina

- Merck

- Pacific Biosciences

- PerkinElmer

- QIAGEN

- Thermo Fisher Scientific

- Myriad Genetics

- Genomind

- OneOme

- Admera Health

- Genelex

- Coriell Life Sciences

- Danaher

- Luminex

- Color Health

- Natera

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Personalized Medicine

- 4.2.2 Advancements in Genetic Sequencing Technologies

- 4.2.3 Growing Prevalence of Chronic and Genetic Diseases

- 4.2.4 Increasing Research and Development Investments

- 4.2.5 High Incidence of Adverse Drug Reactions (ADRs)

- 4.2.6 Expanding Pharmaceutical and Biotechnology Industries

- 4.3 Market Restraints

- 4.3.1 High Costs Associated with Pharmacogenomic Testing

- 4.3.2 Limited Reimbursement Coverage

- 4.3.3 Ethical and Privacy Concerns

- 4.3.4 Lack of Clear Regulatory Guidelines

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product & Service

- 5.1.1 Instruments

- 5.1.2 Reagents & Kits

- 5.1.3 Software & Services

- 5.2 By Technology

- 5.2.1 Polymerase Chain Reaction (PCR)

- 5.2.2 DNA Sequencing

- 5.2.3 Microarray

- 5.2.4 Mass Spectrometry

- 5.2.5 Electrophoresis

- 5.2.6 Other Technologies

- 5.3 By Sample Type

- 5.3.1 Blood

- 5.3.2 Saliva

- 5.3.3 Other Biospecimens

- 5.4 By Application

- 5.4.1 Drug Discovery & Development

- 5.4.2 Oncology

- 5.4.3 Neurology

- 5.4.4 Cardiology

- 5.4.5 Pain Management

- 5.4.6 Other Therapeutic Areas

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Agilent Technologies

- 6.3.3 Becton, Dickinson & Co.

- 6.3.4 bioMerieux

- 6.3.5 Bio-Rad Laboratories

- 6.3.6 Eurofins Scientific

- 6.3.7 F. Hoffmann-La Roche AG

- 6.3.8 Illumina

- 6.3.9 Merck KGaA

- 6.3.10 Pacific Biosciences

- 6.3.11 PerkinElmer

- 6.3.12 Qiagen

- 6.3.13 Thermo Fisher Scientific Inc.

- 6.3.14 Myriad Genetics

- 6.3.15 Genomind

- 6.3.16 OneOme

- 6.3.17 Admera Health

- 6.3.18 Genelex

- 6.3.19 Coriell Life Sciences

- 6.3.20 Danaher Corporation

- 6.3.21 Luminex Corporation

- 6.3.22 Color Health

- 6.3.23 Natera

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment