PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850395

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850395

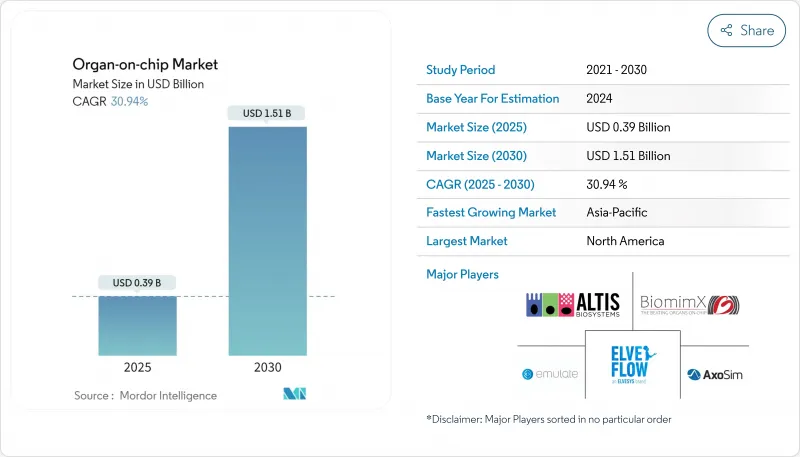

Organ-on-chip - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Organ-on-chip Market size is estimated at USD 0.39 billion in 2025, and is expected to reach USD 1.51 billion by 2030, at a CAGR of 30.94% during the forecast period (2025-2030).

Demand is rising as regulators validate microphysiological systems, pharmaceutical firms redirect R&D funds toward animal-free testing, and 3D printing lowers device fabrication costs. Early commercial traction is strongest in North America, where the FDA Modernization Act 2.0 and the ISTAND Pilot Program have shortened approval timelines. Asia-Pacific is set for the fastest expansion on the back of heavy public spending, while Europe benefits from standardization roadmaps that ease cross-border adoption. Competitive intensity is growing as companies integrate artificial intelligence, strike co-development deals, and scale automated production lines.

Global Organ-on-chip Market Trends and Insights

Global Shift Toward Animal-Free Preclinical Testing Mandates

The FDA's decision in October 2025 to phase out compulsory animal studies for monoclonal antibodies, coupled with the FDA Modernization Act 2.0, is accelerating uptake of human-relevant test beds. The agency's pilot program that lets developers submit non-animal data has prompted pharmaceutical groups to revise internal protocols and divert screening budgets to organ chips. Europe is moving in parallel as regulators tighten restrictions on animal research. These policy moves create a stable demand floor, drive procurement frameworks among contract research organizations, and shorten sales cycles for platform vendors. Firms that combine chips with AI-enabled analytics stand to benefit most because they offer a turnkey path that aligns with post-2025 compliance deadlines. The animal-free mandate therefore anchors medium-term revenue visibility in the organ-on-chip market.

High Burden of Chronic & Complex Diseases Requiring Better Models

Chronic disorders such as metabolic syndrome, non-alcoholic fatty liver disease, and neurodegenerative conditions account for an expanding share of global morbidity. A 2024 study using Hesperos' multi-organ chip replicated NAFLD progression and highlighted therapeutic windows that animal models miss. This ability to mimic human pathophysiology supports go-no-go R&D decisions and lowers clinical attrition costs. Demand is especially pronounced in markets with aging populations and sizable public insurance schemes, which now prioritize translational research that directly benefits patient outcomes. As these health systems push for higher predictive validity, organ chips emerge as indispensable tools, sustaining long-term momentum in the organ-on-chip market.

Technical Complexity & Skill Gap Hindering Broad Adoption

Operating microfluidic platforms demands cross-disciplinary expertise in cell biology, engineering, and sensor integration. A May 2024 review in Frontiers in Lab-on-a-Chip Technology surveyed smaller laboratories and found limited access to trained personnel and standardized protocols. Multi-organ systems exacerbate the burden because each module requires tight flow control and synchronized data capture. To bridge the gap, industry groups advocate modular devices, automated media exchange, and cloud-based analytics. Yet, until these tools become mainstream, complexity will temper uptake, particularly outside tier-one research hubs.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Precision Medicine & Patient-Derived Chips

- Need for Early Detection of Drug Toxicity and New Product Launches

- High Capital & Operating Costs of Microfluidic Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lung chips commanded 34.8% of the organ-on-chip market share in 2024 due to their utility in respiratory toxicity, infectious-disease research, and aerosol delivery studies. The launch of high-fidelity 3D-bioprinted alveolar constructs by POSTECH researchers has strengthened model relevance and drawn funding from vaccine makers. These platforms mimic airway biomechanics, enable endpoints such as ciliary beat frequency, and integrate immune cell layers. With regulatory agencies prioritizing respiratory-drug safety following COVID-19, procurement remains steady. In parallel, heart-on-chip devices are on track for the fastest 33.4% CAGR through 2030, driven by arrhythmia screening and cardiotoxicity testing for oncology compounds. Automated fabrication that embeds force-sensing microwires reduces hands-on time and encourages broader deployment across academic core facilities.

The brain and central-nervous-system subsegment is gaining momentum as researchers seek alternatives to rodent models in neurodegenerative research. Kidney- and liver-based chips hold strong positions; the latter benefits from the ISTAND-validated human Liver-Chip, which anchors safety packages for metabolic candidates. Multi-organ arrays linking vascular, epithelial, and immune components represent the next frontier. Vendors that offer ready-to-use, modular plates stand to capture incremental orders as sponsors move toward systemic pharmacology studies.

The Organ-On-Chip Market Report Segments the Industry Into by Organ Type (Liver, Heart, Lung, and More), Application (Drug Discovery and Lead Identification, and More), End User (Pharmaceutical and Biotechnology Companies, Academic and Research Institutes, and More) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 42.8% of 2024 revenue for the organ-on-chip market, buoyed by the FDA's ISTAND framework, deep venture pools, and collaborations between Ivy League universities and big pharma. The United States hosts most early-stage chip trials, while Canada supplies polymer microfabrication expertise that feeds contract manufacturers. Reimbursement pilots under Medicare's coverage-with-evidence paradigm further encourage hospital-based translational studies.

Asia-Pacific is on course for the swiftest 35.3% CAGR through 2030. China leverages state grants that subsidize microfluidic tooling, and its contract research ecosystem scales at speed to handle multinational outsourcing. Japan's Pharmaceuticals and Medical Devices Agency has issued guidance on microphysiological data submissions, giving local developers a route to domestic approval. South Korean consortia align chip production with national initiatives in cell and gene therapy, creating synergistic demand.

Europe maintains a robust share powered by Horizon Europe grants and a consolidated academic network. The CEN/CENELEC roadmap published in July 2024 maps pathways for material qualification, sterilization, and cell integrity that foster cross-lab comparability. France and Germany finance industry clusters that pair nanoscale engineering with primary human-cell banks. The region's stringent animal-welfare rules accelerate substitution of in vivo assays with chip models, especially in safety pharmacology and cosmetics.

- Emulate

- Mimetas

- CN Bio Innovations

- TissUse

- Hesperos

- AxoSim Technologies

- Altis Biosystems

- InSphero

- Nortis

- Kirkstall Ltd

- Netri SAS

- BiomimX

- Bi/ond BV

- Organovo

- Allevi Inc. (3D Systems)

- Elveflow (Elvesys)

- Hurel

- Valo Health (Tara Biosystems)

- SynVivo (CFD Research)

- BioChip Technologies GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Global Shift Toward Animal-Free Preclinical Testing Mandates

- 4.2.2 High Burden of Chronic & Complex Diseases Requiring Better Models

- 4.2.3 Rising Demand for Precision Medicine & Patient-Derived Chips

- 4.2.4 Need for Early Detection of Drug Toxicity and New Products Launches

- 4.2.5 Strategic Investments & Partnerships Accelerating Commercialization

- 4.2.6 Technological Advances in Microfabrication & 3D Bioprinting

- 4.3 Market Restraints

- 4.3.1 Technical Complexity & Skill Gap Hindering Broad Adoption

- 4.3.2 High Capital & Operating Costs of Microfluidic Infrastructure

- 4.3.3 Limited Regulatory Validation & Harmonized Guidelines

- 4.3.4 High CapEx for Automated Microfluidic Tool-chains

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Organ Type

- 5.1.1 Liver

- 5.1.2 Heart

- 5.1.3 Lung

- 5.1.4 Kidney

- 5.1.5 Intestine

- 5.1.6 Brain & CNS

- 5.1.7 Skin

- 5.1.8 Multi-Organ & Other Complex Systems

- 5.2 By Application

- 5.2.1 Drug Discovery & Lead Identification

- 5.2.2 ADME/Toxicology Screening

- 5.2.3 Disease Modeling

- 5.2.4 Precision Medicine & Personalized Therapy

- 5.2.5 Other Applications

- 5.3 By End User

- 5.3.1 Pharmaceutical & Biotechnology Companies

- 5.3.2 Contract Research Organizations

- 5.3.3 Academic & Research Institutes

- 5.3.4 Cosmetics & Personal Care Industry

- 5.3.5 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Emulate Inc.

- 6.4.2 MIMETAS BV

- 6.4.3 CN Bio Innovations

- 6.4.4 TissUse GmbH

- 6.4.5 Hesperos Inc.

- 6.4.6 AxoSim Technologies

- 6.4.7 Altis Biosystems

- 6.4.8 InSphero AG

- 6.4.9 Nortis Inc.

- 6.4.10 Kirkstall Ltd

- 6.4.11 Netri SAS

- 6.4.12 BiomimX SRL

- 6.4.13 Bi/ond BV

- 6.4.14 Organovo Holdings Inc.

- 6.4.15 Allevi Inc. (3D Systems)

- 6.4.16 Elveflow (Elvesys)

- 6.4.17 Hurel Corporation

- 6.4.18 Valo Health (Tara Biosystems)

- 6.4.19 SynVivo (CFD Research)

- 6.4.20 BioChip Technologies GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment