PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850404

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850404

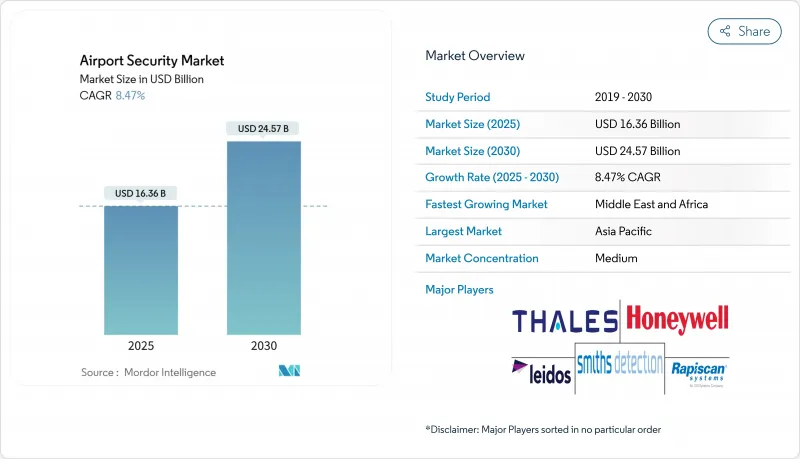

Airport Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The airport security market size stands at USD 16.36 billion in 2025 and is forecasted to reach USD 24.57 billion by 2030, supported by an 8.47% CAGR.

Strong growth stems from steady passenger recovery, sizeable capital outlays for terminal upgrades, and rapid adoption of AI-enabled screening and perimeter solutions. Airports are accelerating biometric enrolment programs, linking passenger identity to boarding data and baggage status to streamline journeys. At the same time, integrated command-and-control platforms give operators unified views of checkpoints, airside movements, and cyber alerts, improving incident response speed. Investments also track heightened geopolitical risk, driving demand for high-resolution radar, drone interdiction tools, and resilient cloud architectures that safeguard data flows across airline, government, and airport systems.

Global Airport Security Market Trends and Insights

Rising Passenger Traffic Driving Screening Automation

Air travel is rebounding, with global volumes touching 9.5 billion in 2024, a 10% year-on-year lift. Screening checkpoints, therefore, face sustained throughput pressure. Programs such as TSA PreCheck and EU Smart Security require imaging systems that clear more passengers while matching or exceeding current detection rates. TSA now screens over 3 million travelers on busy travel days, prompting roll-outs of computed-tomography lanes and automated tray return systems at major hubs. Miami International Airport's biometric boarding deployment demonstrates how facial recognition can cut individual verification to two seconds, easing queues without lowering security. These outcomes reinforce the business case for self-service kiosks and AI analytics that keep passengers moving even during peak bank departures.

Harmonised International Regulatory Upgrades

The European requirement that all primary checkpoints install CT scanners by 2025 is now influencing procurement cycles worldwide. Alignment with ICAO Annex 17 and ECAC testing protocols offers equipment vendors a single pathway to multi-region acceptance, reducing duplication yet raising baseline performance criteria. TSA's USD 11.8 billion FY 2025 budget earmarks additional funds for advanced screening, reflecting Washington's comparable push to modernize domestic checkpoints. Regulatory clarity shapes airport tenders, incentivising suppliers to pre-certify AI algorithms for prohibited-item detection and to demonstrate low false-alarm rates in independent laboratories.

Lengthy Certification and Operational Qualification Cycles

Before new scanners or software enter live lanes, they face multi-step lab tests, field pilots, and regulatory sign-off. ECAC's Common Evaluation Process can exceed 18 months from submission to approval, prolonging vendor cash-burn and extending legacy system life. TSA's Air Cargo Screening Technology List applies similar vetting, segmenting equipment into Qualified, Approved, or Grandfathered categories. Such rigor ensures performance consistency but delays widespread installation of AI-native platforms, moderating short-term revenue growth for newer entrants in the airport security market.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Integrated Command-and-Control and AI Video Analytics

- Cyber-Physical Convergence and Cloud Migration

- Scarcity of Skilled Aviation Security Technologists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Screening and scanning systems delivered 36.19% of 2024 revenue, anchored by mandatory CT deployments and consolidated tray return lanes. Asia-Pacific hubs adopt dual-view X-ray and body scanners at new terminals to keep pace with rising traffic. The airport security market size for access control and biometrics is set to climb swiftly, and this is supported by an 11.62% CAGR tied to frictionless passenger processing initiatives.

Programs like TSA's nationwide facial-verification expansion illustrate how airports substitute physical boarding passes for biometric tokens, trimming document checks and hygiene concerns. Perimeter Intrusion Detection Systems are gaining visibility as drone incursions push operators to network radar, electro-optical, and RF jamming assets into layered defences. Command-and-control software unifies these feeds, granting security managers a consolidated dashboard and audit trail.

Beyond the checkpoint, AI-based video analytics augment surveillance by auto-tracking abandoned items or loitering near sensitive doors. Cybersecurity suites encrypt data flows from edge scanners to cloud servers, shielding traveller PII and threat-image libraries. With regulators tightening breach-reporting windows, integrated SOC solutions that merge cyber and physical alerts are now a procurement priority. All these converging needs keep the airport security market on an innovation cycle centred on software-defined capabilities rather than standalone hardware refreshes.

Facilities handling more than 50 million passengers commanded 42.58% of the airport security market share in 2024 as their capex programs funded multi-layered ecosystems and digital ID rollouts. Large hubs like Dubai, Atlanta, and Beijing standardise checkpoint layouts across concourses, facilitating bulk procurement of identical CT lanes that simplify operator training. However, airports in the 15-30 million passenger bracket post the quickest 11.68% CAGR, driving demand for scaled-down but future-proof platforms that slot into existing footprints. These mid-tier stations often act as national secondary gateways, deploying cloud-hosted access control to maintain cyber resilience without building local data centres.

Smaller regional airports with budgets below 5 million travellers face restricted budgets, yet must comply with the same emerging standards. Public-sector grants and centralised service contracts help them procure certified scanners and managed SOC support. Policy alerts from aviation associations spotlight the risk that under-funded perimeter fences pose to network-level aviation security. Consequently, central governments allocate targeted funds, mirroring the Irish example, where regional facilities received EUR 7.8 million (USD 8.92 million) for security and sustainability works.

The Airport Security Market Report is Segmented by Security System (Screening and Scanning Systems, Surveillance Systems, Access Control and Biometrics, and More), Airport Size (Less Than 5 Million, 5 To 15 Million, and More), Technology (Hardware, Software, and Services), Application (Terminal, Airside, Landside, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 33.67% of global revenue in 2024, buoyed by aggressive capacity additions and digital-first passenger experience mandates. Regional governments intend to invest USD 240 billion from 2025 to 2035, with USD 136 billion allocated to upgrades and USD 104 billion earmarked for new airports, boosting passenger capacity by 1.24 billion seats. China, India, and Indonesia each announced multiyear runway and terminal builds that embed CT checkpoints and biometric gates at the blueprint stage, embedding security by design.

The Middle East and Africa segment posts the fastest 12.18% CAGR. Gulf carriers are raising fleet counts, and host states fund mega-terminal projects linked to tourism diversification plans. Up to USD 151 billion may flow into security-relevant upgrades by 2040, including integrated surveillance and drone interdiction suites. Saudi Arabia's Vision 2030 target of 300 million passengers reinforces sustained demand for screening automation and cyber-physical monitoring.

North America remains a technology bellwether as TSA pilots HD-Advanced Imaging Technology that lets travellers keep light jackets on during scans, cutting carry-on divest time. Federal grants also back regional facilities replacing legacy X-ray units with CT systems. Europe aligns equipment policies through mandatory CT adoption and entry-exit biometric databases, encouraging airports to centralise identity verification and risk assessment.

- Smiths Detection Group Ltd. (Smiths Group plc)

- Rapiscan Systems, Inc. (OSI Systems, Inc.)

- Leidos, Inc.

- Thales Group

- Honeywell International, Inc.

- Siemens AG

- KEENINFINITY (Robert Bosch GmbH)

- Teledyne FLIR LLC (Teledyne Technologies Incorporated)

- Collins Aerospace (RTX Corporation)

- SITA

- NEC Corporation

- IDEMIA

- Nuctech Technology Co., Ltd.

- Garrett Electronics Inc.

- ICTS Europe S.A.

- Rohde & Schwarz USA, Inc.

- Hart Security Limited

- Senstar Corp

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising passenger traffic and touchless screening

- 4.2.2 Harmonised international security regulations

- 4.2.3 Integrated command-and-control with AI analytics

- 4.2.4 Cyber-physical convergence and cloud migration

- 4.2.5 Biometric One-ID and seamless travel initiatives

- 4.2.6 Drone and UAS threats lifting perimeter demand

- 4.3 Market Restraints

- 4.3.1 Lengthy certification and qualification cycles

- 4.3.2 Scarcity of skilled aviation security technologists

- 4.3.3 Integration debt from legacy infrastructure

- 4.3.4 Capex compression amid uneven traffic recovery

- 4.4 Value Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Security System

- 5.1.1 Screening and Scanning Systems

- 5.1.2 Surveillance Systems

- 5.1.3 Access Control and Biometrics

- 5.1.3.1 Fingerprint Recognition

- 5.1.3.2 Facial Recognition

- 5.1.3.3 Iris and Retina Recognition

- 5.1.4 Perimeter Intrusion Detection Systems

- 5.1.5 Fire and Life-Safety Systems

- 5.1.6 Cybersecurity and Network Protection

- 5.1.7 Command, Control and Integration Platforms

- 5.2 By Airport Size

- 5.2.1 Less than 5 Million

- 5.2.2 5 to 15 Million

- 5.2.3 15 to 30 Million

- 5.2.4 30 to 50 Million

- 5.2.5 More than 50 Million

- 5.3 By Technology

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.4 By Application

- 5.4.1 Terminal

- 5.4.2 Airside

- 5.4.3 Landside

- 5.4.4 Perimeter and Restricted Areas

- 5.4.5 Cargo and Logistics Facilities

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 United Arab Emirates

- 5.5.4.1.2 Saudi Arabia

- 5.5.4.1.3 Qatar

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Rest of Africa

- 5.5.5 Asia-Pacific

- 5.5.5.1 China

- 5.5.5.2 India

- 5.5.5.3 Japan

- 5.5.5.4 South Korea

- 5.5.5.5 Singapore

- 5.5.5.6 Rest of Asia-Pacific

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Smiths Detection Group Ltd. (Smiths Group plc)

- 6.4.2 Rapiscan Systems, Inc. (OSI Systems, Inc.)

- 6.4.3 Leidos, Inc.

- 6.4.4 Thales Group

- 6.4.5 Honeywell International, Inc.

- 6.4.6 Siemens AG

- 6.4.7 KEENINFINITY (Robert Bosch GmbH)

- 6.4.8 Teledyne FLIR LLC (Teledyne Technologies Incorporated)

- 6.4.9 Collins Aerospace (RTX Corporation)

- 6.4.10 SITA

- 6.4.11 NEC Corporation

- 6.4.12 IDEMIA

- 6.4.13 Nuctech Technology Co., Ltd.

- 6.4.14 Garrett Electronics Inc.

- 6.4.15 ICTS Europe S.A.

- 6.4.16 Rohde & Schwarz USA, Inc.

- 6.4.17 Hart Security Limited

- 6.4.18 Senstar Corp

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment