PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850982

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850982

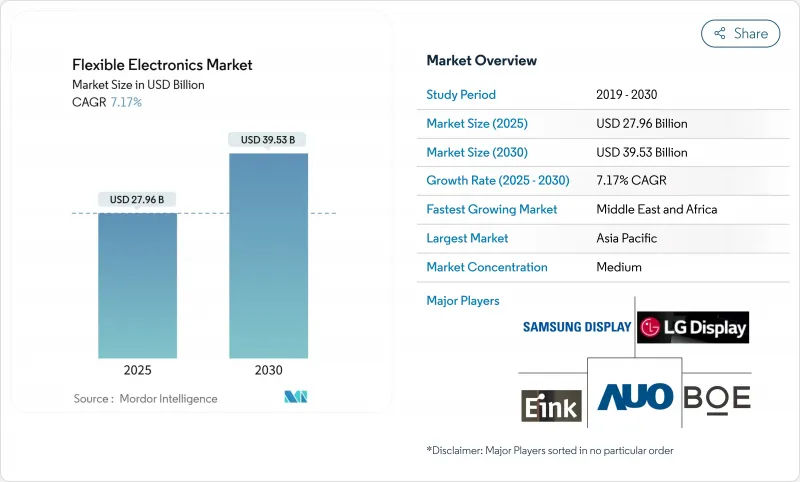

Flexible Electronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The flexible electronics market size reached USD 27.96 billion in 2025 and is forecast to climb to USD 39.53 billion by 2030, reflecting a 7.17% CAGR over 2025-2030.

The expansion stems from a shift away from niche prototypes toward mainstream deployments in smartphones, automobiles, and healthcare wearables, supported by ultra-thin OLED stacks, conformal sensor breakthroughs, and roll-to-roll production economics that lower entry costs. Demand accelerates as curved automotive head-up displays (HUDs) reshape cockpit design, while North American healthcare systems validate continuous monitoring patches that rely on stretchable biosensors. Investments from BOE and Samsung in Gen-8.6 AMOLED and ultra-thin OLED lines, coupled with Middle East defense programs prioritizing lightweight conformal antennas, further elevate the flexible electronics market's momentum. At the same time, supply-chain concentration in high-barrier encapsulation films and the absence of universal reliability standards for stretchable interconnects temper growth prospects by raising qualification hurdles and cost uncertainty.

Global Flexible Electronics Market Trends and Insights

Improved durability of ultra-thin OLED stacks enabling foldable smartphones

Samsung Display's Flex Magic Pixel demonstrator passed military-grade durability tests, eliminating visible creases and meeting user expectations for robust folding screens. Apple's 2026 foldable iPhone order for 9-15 million 7.8-inch panels validates commercial readiness and signals mass adoption. Weight reductions of 30% and power savings of 30% in 2026 laptop panels widen the addressable device pool beyond phones. These advances resonate across the flexible electronics market as OEMs migrate tablets and laptops toward bendable formats, reinforcing supply-chain demand for high-barrier encapsulation and ultra-thin glass.

Demand for conformal sensors in wearable medical patches across North America

FDA clearance for X-trodes' Smart Skin and UC San Diego's 1,024-channel brain sensor array legitimizes flexible biosensors for continuous monitoring. Health-system reimbursement models pivot toward outcome-based care, favoring devices that capture longitudinal patient data. Flexible substrates reduce motion artifacts, maintaining signal integrity during everyday activities. Device makers tap organic electrochemical transistors for in-sensor computing, minimizing latency and protecting patient privacy. As reimbursement codes codify remote monitoring, the flexible electronics market benefits from recurrent sensor and patch replacements.

Limited standardization of stretchable interconnect reliability tests

Rigid-electronics standards fail to capture simultaneous bending, twisting, and temperature cycling seen in wearable use. IEEE's draft bladder-inflation method measures multi-axis stretch but remains voluntary, deterring automotive and medical OEMs that require certified lifetime data. Researchers propose polymer interlayer designs to curb substrate cracking under strain, yet without consensus metrics investors hesitate to fund high-volume tooling. The flexible electronics market thus faces slower design-win cycles until unified protocols emerge.

Other drivers and restraints analyzed in the detailed report include:

- Automotive cockpit digitization driving curved HUD adoption in Europe

- Roll-to-roll manufacturing cost reduction in Asia for printed ICs

- Yield Losses in Large-area Printing of Metallic Inks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flexible displays accounted for 54.7% of flexible electronics market share in 2024, powered by relentless foldable smartphone launches and curved automotive dashboards. Samsung's 18.1-inch foldable prototype proves scalability into laptops, while LG's stretchable micro-LED panel unlocks 3D surfaces in fashion and in-vehicle lighting. Complementing displays, the sensor category yields a 9.2% CAGR over 2025-2030 as hospitals adopt epidermal ECG and EEG patches for chronic care. Quantum-dot display-sensor hybrids that tolerate 1.5X stretching herald multifunctional surfaces that both show and sense data, positioning sensors as the next growth catalyst. Despite progress, flexible batteries and memory lag due to safety and yield hurdles, limiting fully integrated flexible systems today.

The flexible electronics market benefits from panel makers leveraging transparent OLED stacks to embed fingerprint and SpO2 reading directly under the screen, condensing component count and thinning device profiles. Integrated biosensing displays open new monetization avenues for smartphone vendors seeking differentiation. Energy-harvesting films that convert vibration into micro-watts reduce battery load in wearables and industrial tags, though commercialization awaits stable supply of high-performance piezoelectric polymers. As cross-component synergies mature, device architects can design seamless form factors that merge visual, haptic, and sensing capabilities.

Plastic substrates represented 61.6% of flexible electronics market size in 2024, driven by mature polyimide supply chains aligned with display fabs. Their thermal stability up to 400 °C pairs well with copper traces, minimizing delamination in automotive dashboards exposed to wide temperature swings. Metal foils, chiefly copper and stainless steel, post an 8.4% CAGR thanks to innate conductivity and EMI shielding valued in defense radios and high-speed data cables. Graphene-coated copper nanowires offer lower sheet resistance than indium-tin-oxide while retaining flexibility, attracting interest for roll-to-roll touch sensors.

Ultra-thin glass gains traction in premium foldable devices requiring pristine optics and scratch resistance. At just 30 µm, Corning's latest glass can bend to 5 mm radius without fracture, albeit at a higher price point than polymer. Silver-nanowire ink advances, accelerated by DuPont's 2024 C3Nano asset purchase, improve transparency and mechanical resilience for smart windows. Carbon-based conductive inks address ESG mandates by eliminating scarce indium and toxic solvents, appealing to builders of flexible photovoltaics integrated into facades. Material selection now balances cost, performance, and recyclability as regulators scrutinize electronic waste.

The Flexible Electronics Market Report is Segmented by Component (Flexible Displays, Flexible Sensors, and More), Material (Plastic Substrate, Glass, and More), Technology (Printed Electronics, Organic Electronics, and More), Application (Sensing, Lighting, Display, and More), End-User Industry (Consumer Electronics, Automotive and Transportation, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 45.7% of flexible electronics market share in 2024, anchored by China's manufacturing scale and Korea's OLED innovation pipeline. BOE's USD 9 billion Gen-8.6 AMOLED fab in Chengdu-the city's largest single industrial investment-expands panel capacity for tablets and automotive cockpits. Korean institutes pushed piezoelectric harvester output 280X, underscoring regional leadership across displays, sensors, and energy devices. Japan contributes precision deposition tools and ultra-thin glass that support foldable handset reliability.

North America focuses on high-value healthcare and defense niches, leveraging FDA clearances for flexible biosensors and Pentagon funding for battlefield antenna arrays. Samsung's USD 240 million Yokohama packaging R&D hub highlights cross-border collaboration, as Asian suppliers co-locate near U.S. system integrators. Silicon Valley startups pioneer flexible IC design automation, shortening tape-out cycles for printed logic that feeds disposable diagnostics.

Europe prioritizes automotive digitization and sustainability. German OEMs mandate holographic HUD integration by 2028, driving demand for bendable displays meeting stringent glare and impact standards. EU directives on building-integrated photovoltaics spur trials of facade-embedded flexible PV skins. Simultaneously, strict e-waste rules push recyclability, accelerating research into biodegradable substrates.

Middle East and Africa posts the highest 11.3% CAGR as defense modernization and smart-city programs embrace conformal electronics for weight-sensitive drones and harsh-climate sensors. Governments fast-track 5G and edge networks, creating pull for flexible antennas resistant to sand and heat. Regional universities partner with European labs on organic PV to power off-grid IoT nodes, broadening application diversity.

- Samsung Display Co. Ltd

- LG Display Co. Ltd

- BOE Technology Group Co. Ltd

- AU Optronics Corp.

- Royole Corporation

- E Ink Holdings Inc.

- OLEDWorks LLC

- FlexEnable Ltd

- PragmatIC Semiconductor Ltd

- Imprint Energy Inc.

- Blue Spark Technologies Inc.

- Flexpoint Sensor Systems Inc.

- Universal Display Corporation

- Kyocera Corporation

- Panasonic Holdings Corp.

- Sony Group Corp.

- Polyera Corporation

- Cambrios Advanced Materials Corp.

- Heliatek GmbH

- First Solar Inc. (Flex PV Division)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Improved Durability of Ultra-thin OLED Stacks Enabling Foldable Smartphones

- 4.2.2 Demand for Conformal Sensors in Wearable Medical Patches across North America

- 4.2.3 Automotive Cockpit Digitization Driving Curved HUD Adoption in Europe

- 4.2.4 Roll-to-Roll Manufacturing Cost Reduction in Asia for Printed ICs

- 4.2.5 Defense Push for Lightweight, Conformal Antennas in Middle East UAVs

- 4.2.6 ESG-Led Push toward Flexible PV Skins on Commercial Buildings

- 4.3 Market Restraints

- 4.3.1 Yield Losses in Large-area Printing of Metallic Inks

- 4.3.2 Limited Standardization of Stretchable Interconnect Reliability Tests

- 4.3.3 Supply-chain Concentration of High-barrier Encapsulation Films

- 4.3.4 Disposal and Recycling Complexities of Poly-imide Substrates

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Flexible Displays

- 5.1.1.1 OLED

- 5.1.1.2 E-Paper

- 5.1.1.3 Others

- 5.1.2 Flexible Sensors

- 5.1.2.1 Biosensors

- 5.1.2.2 Pressure Sensors

- 5.1.2.3 Temperature Sensors

- 5.1.2.4 Others

- 5.1.3 Flexible Batteries

- 5.1.4 Flexible Memory

- 5.1.5 Flexible Photovoltaics

- 5.1.6 Others

- 5.1.1 Flexible Displays

- 5.2 By Material

- 5.2.1 Plastic Substrate

- 5.2.2 Glass (Ultra-thin)

- 5.2.3 Metal Foils

- 5.2.4 Conductive Inks

- 5.2.5 Dielectrics/Encapsulation

- 5.3 By Technology

- 5.3.1 Printed Electronics

- 5.3.2 Organic Electronics

- 5.3.3 Thin-Film Inorganic Electronics

- 5.3.4 Hybrid Systems

- 5.4 By Application

- 5.4.1 Sensing

- 5.4.2 Lighting

- 5.4.3 Display

- 5.4.4 Energy Harvesting

- 5.4.5 RFID and Smart Labels

- 5.4.6 Others

- 5.5 By End-User Industry

- 5.5.1 Consumer Electronics

- 5.5.2 Automotive and Transportation

- 5.5.3 Healthcare and Medical Devices

- 5.5.4 Military and Defense

- 5.5.5 Industrial and IoT

- 5.5.6 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Nordics

- 5.6.2.5 Rest of Europe

- 5.6.3 South America

- 5.6.3.1 Brazil

- 5.6.3.2 Rest of South America

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South-East Asia

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Gulf Cooperation Council Countries

- 5.6.5.1.2 Turkey

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Display Co. Ltd

- 6.4.2 LG Display Co. Ltd

- 6.4.3 BOE Technology Group Co. Ltd

- 6.4.4 AU Optronics Corp.

- 6.4.5 Royole Corporation

- 6.4.6 E Ink Holdings Inc.

- 6.4.7 OLEDWorks LLC

- 6.4.8 FlexEnable Ltd

- 6.4.9 PragmatIC Semiconductor Ltd

- 6.4.10 Imprint Energy Inc.

- 6.4.11 Blue Spark Technologies Inc.

- 6.4.12 Flexpoint Sensor Systems Inc.

- 6.4.13 Universal Display Corporation

- 6.4.14 Kyocera Corporation

- 6.4.15 Panasonic Holdings Corp.

- 6.4.16 Sony Group Corp.

- 6.4.17 Polyera Corporation

- 6.4.18 Cambrios Advanced Materials Corp.

- 6.4.19 Heliatek GmbH

- 6.4.20 First Solar Inc. (Flex PV Division)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment