PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851014

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851014

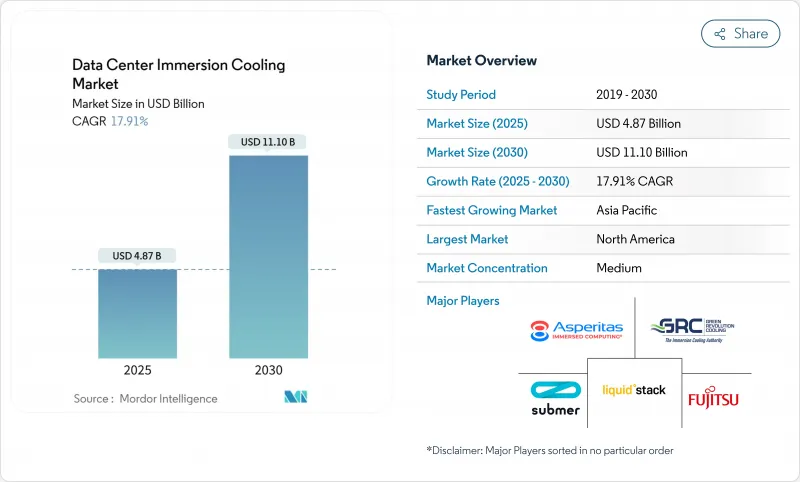

Data Center Immersion Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The data center immersion cooling market is valued at USD 4.87 billion in 2025 and is forecast to reach USD 11.10 billion by 2030, registering a 17.91% CAGR.

This rapid climb mirrors the industry's response to soaring rack power densities driven by AI and machine-learning workloads that regularly exceed 50 kW per rack. Operators view immersion technology as a route to maintain performance, shrink facility footprints, and comply with upcoming restrictions on PFAS-based coolants. North America anchors adoption through production-scale rollouts by the hyperscale cloud providers, while Asia-Pacific exhibits the steepest growth as Japan, China, and South Korea champion liquid-cooled AI clusters. On the technology front, single-phase systems retain the lion's share because of installation familiarity, yet two-phase designs are winning pilots where extreme density and pump-free architectures are essential.

Global Data Center Immersion Cooling Market Trends and Insights

Proliferation of Hyperscale Data Centers

Surging demand for generative-AI services compels the leading cloud providers to erect new hyperscale sites that often target rack densities above 100 kW. Google's use of immersion-cooled TPU pods illustrates how large providers are standardizing liquid technologies to curtail real-estate requirements and capex for building expansion. Microsoft has validated production two-phase tanks at its Quincy, Washington, campus, citing easier density scaling and favorable total-cost-of-ownership metrics. When applied atthe portfolio level, immersion cooling enables operators to pack 10-15X more compute into the same footprint, directly translating into faster time-to-revenue for AI services. The ability to drive higher utilization from every square foot remains the strongest economic lever motivating hyperscale adoption.

Rising Rack-Power Densities from AI/ML Workloads

Field data from KDDI's containerized sites shows single-phase immersion cutting server-rack power draw by 43% while achieving PUE below 1.07. Operators in energy-constrained locales exploit such savings to offset rising electricity tariffs and carbon taxes. European facilities face the EU Energy Efficiency Directive's mandated 11.7% reduction in energy use by 2030; immersion's ability to hit sub-1.1 PUE values provides a practical compliance pathway. Further benefits emerge at the server level, as sustained higher boost frequencies translate into more compute per watt.

Expansion of Edge Micro-Data Centers for 5G/IoT

Telecom carriers and industrial firms are rolling out micro-modules close to end-users to meet 5G latency targets. In regions with limited HVAC infrastructure or hostile climates, sealed single-phase tanks enable autonomous edge nodes that run without chilled-water plants. Early pilots across Southeast Asia illustrate that immersion systems can survive dust, humidity and temperature swings that cripple traditional air-cooled racks.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push Toward PFAS-Free, Bio-Based Coolants

- Fragmented Standards and Vendor Interoperability Gaps

- High Upfront CAPEX and Facility-Redesign Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-phase systems dominated 2024 with 80.9% share; however, two-phase designs are forecast to compound at 21.6% annually to 2030. That acceleration reflects superior heat-flux removal through low-pressure boiling, which allows passive condensers to reject heat without pumps or secondary loops. Microsoft's Quincy deployment showcases how phase-change tanks sustain 100 kW racks in production.

In enterprise pilots, operators prefer single-phase solutions for ease of maintenance and established supply chains, particularly where mineral oil or synthetic hydrocarbons offer predictable viscosity and broad component compatibility. Yet AI fabs built on the latest 1 kW GPUs increasingly select two-phase setups to eliminate pump failures and tap datacenter waste heat for district-heating schemes. As suppliers shrink tank footprints and introduce pre-charged cassettes, the learning curve shortens, setting the stage for two-phase systems to claim incremental share over the forecast horizon. The data center immersion cooling market consequently evolves toward a dual-track ecosystem where single-phase dominates legacy refresh spend while two-phase captures new-build footprints geared for extreme density.

Synthetic hydrocarbon fluids held 41.2% of 2024 revenue thanks to their low viscosity and strong material compatibility, making them the de-facto baseline across most single-phase deployments. Mineral oils, once relegated to cryptocurrency mines, re-enter mainstream consideration and are projected to grow 18.4% through 2030 as refiners deliver cleaner cuts that meet extended service-life targets. In comparison, fluorocarbon blends face heightened scrutiny under PFAS regulation, a headwind that propels bio-derivatives into pilot stages.

Lubrizol's CompuZol family demonstrates synthetic hydrocarbons pushing thermal conductivity to 0.15 W/m-K while preserving flash points above 170 °C. TotalEnergies' BioLife products illustrate how traceable plant-based stocks can equal petrochemical performance yet biodegrade rapidly, satisfying EU waste directives. Because coolant selection dictates seal compatibility, dielectric strength and disposal pathways, operators continue to conduct lengthy qualification programs, reinforcing fluid suppliers' influence over the data center immersion cooling market trajectory.

Data Center Immersion Cooling Market is Segmented by Type ( Single-Phase Immersion Cooling System, Two-Phase Immersion Cooling System), Cooling Fluid ( Mineral Oil, De-Ionized Water, and More), Application ( High-Performance Computing (HPC), Edge Computing, and More), Data Center Type (Hyperscale/Self-Built, Colocation / Wholesale, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 44.8% of 2024 revenue, underpinned by hyperscale capital expenditure and an innovation culture that embraces pilot-to-production transitions rapidly. LiquidStack's new Texas facility triples local tank output, shortening lead times and reinforcing domestic supply chains Policy frameworks focused on voluntary efficiency goals rather than prescriptive equipment mandates grant operators leeway to trial immersion without regulatory delays.

Asia-Pacific is the fastest-growing region at 19.6% CAGR, spurred by government-backed AI supercomputers and data-sovereignty initiatives. Japan's KDDI recorded PUE values approaching 1.05 after deploying containerized single-phase rigs, validating immersion for telecom edge use cases. China's coastal underwater data center proofs of concept illustrate novel siting strategies that rely on immersion to mitigate corrosion and humidity.

Europe leans on regulation as the primary adoption driver. The 2024 EU sustainability disclosure requirement pushes operators to cut both energy and water usage, making immersion attractive. The Netherlands enforces 27 °C supply-air ceilings that air-cooling systems struggle to meet, accelerating liquid retrofits in Amsterdam facilities. Heat-reuse pilots, such as feeding swimming pools in Denmark, further improve immersion project economics, enabling operators to recoup costs via heat-offtake agreements.

- Fujitsu Limited

- Green Revolution Cooling (GRC) Inc.

- Submer Technologies SL

- LiquidStack Inc.

- Asperitas

- LiquidCool Solutions

- Midas Green Technologies

- Iceotope Technologies Ltd.

- Wiwynn Corporation

- DCX Ltd.

- Dell Technologies

- Intel Corporation

- Schneider Electric SE

- Vertiv Holdings Co.

- NVIDIA Corporation

- Asetek A/S

- Shell plc (Immersion Cooling Fluids)

- Cargill Inc. (NatureCool)

- 3M Company

- Chemours Company

- Molex LLC

- Hypertec Group

- Alibaba Cloud

- Tencent Cloud

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of hyperscale data centers

- 4.2.2 Rising rack-power densities from AI/ML workloads

- 4.2.3 Superior energy-efficiency and PUE gains over air cooling

- 4.2.4 Regulatory push toward PFAS-free, bio-based coolants

- 4.2.5 Expansion of edge micro-data-centers for 5G/IoT

- 4.2.6 Launch of immersion-ready silicon packages greater than1 kW TDP

- 4.3 Market Restraints

- 4.3.1 High upfront CAPEX and facility-redesign costs

- 4.3.2 Fragmented standards and vendor interoperability gaps

- 4.3.3 Supply-chain risk for fluorinated dielectrics

- 4.3.4 Material-compatibility concerns voiding warranties

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 Evolution of Data-Center Cooling

- 4.6.2 Energy-consumption and compute-density metrics

- 4.6.3 Teardown of fluids, processors, GPUs, racks and infra

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Degree of Competition

- 4.7.5 Threat of Substitutes

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE and GROWTH FORECASTS(VALUE)

- 5.1 By Type

- 5.1.1 Single-Phase Immersion Cooling System

- 5.1.2 Two-Phase Immersion Cooling System

- 5.2 By Cooling Fluid

- 5.2.1 Mineral Oil

- 5.2.2 De-ionized Water

- 5.2.3 Fluorocarbon-based Fluids

- 5.2.4 Synthetic Hydrocarbon Fluids

- 5.2.5 Bio-based Fluids

- 5.3 By Application

- 5.3.1 High-Performance Computing (HPC)

- 5.3.2 Edge Computing

- 5.3.3 Artificial Intelligence and Machine Learning

- 5.3.4 Cryptocurrency Mining

- 5.3.5 Cloud and Hyperscale Data Centers

- 5.3.6 Other Applications

- 5.4 By Data Center Type

- 5.4.1 Hyperscale/Self-Built

- 5.4.2 Colocation / Wholesale

- 5.4.3 Enterprise/Edge Data Centers

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Netherlands

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Fujitsu Limited

- 6.4.2 Green Revolution Cooling (GRC) Inc.

- 6.4.3 Submer Technologies SL

- 6.4.4 LiquidStack Inc.

- 6.4.5 Asperitas

- 6.4.6 LiquidCool Solutions

- 6.4.7 Midas Green Technologies

- 6.4.8 Iceotope Technologies Ltd.

- 6.4.9 Wiwynn Corporation

- 6.4.10 DCX Ltd.

- 6.4.11 Dell Technologies

- 6.4.12 Intel Corporation

- 6.4.13 Schneider Electric SE

- 6.4.14 Vertiv Holdings Co.

- 6.4.15 NVIDIA Corporation

- 6.4.16 Asetek A/S

- 6.4.17 Shell plc (Immersion Cooling Fluids)

- 6.4.18 Cargill Inc. (NatureCool)

- 6.4.19 3M Company

- 6.4.20 Chemours Company

- 6.4.21 Molex LLC

- 6.4.22 Hypertec Group

- 6.4.23 Alibaba Cloud

- 6.4.24 Tencent Cloud

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment