PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851030

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851030

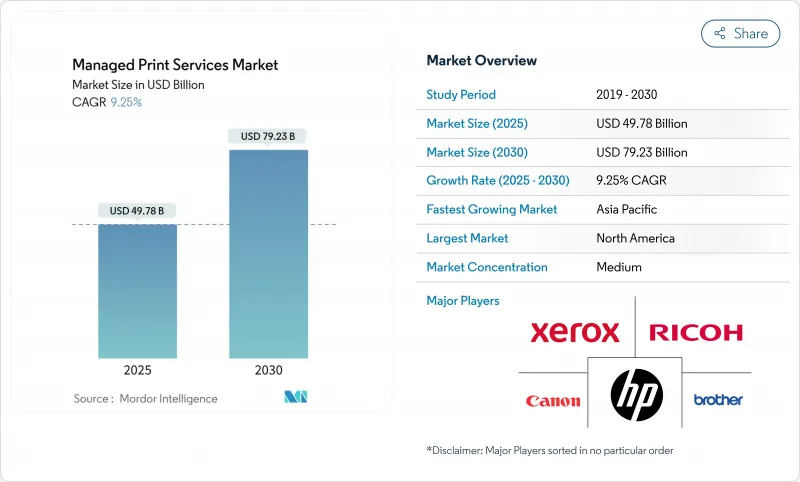

Managed Print Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The managed print services market size is estimated at USD 49.78 billion in 2025 and is is forecast to reach USD 79.23 billion by 2030, expanding at a 9.25% CAGR.

Cloud connectivity, hybrid-work infrastructure, and subscription pricing are converging to lift adoption across large enterprises and an expanding base of small and medium businesses. Security-rich fleets, real-time IoT diagnostics, and automated consumables replenishment are proving decisive in lowering total cost of ownership and reducing unplanned downtime. Demand also reflects mounting sustainability mandates that reward providers able to quantify duplex usage, carbon savings, and paper-waste avoidance. Competitive positioning is shifting as hardware-centric incumbents blend analytics, workflow automation, and device-as-a-service bundles to defend share against cloud-native entrants specializing in AI-driven optimisation. Regional momentum is most pronounced in Asia-Pacific, where large manufacturers and export-oriented enterprises view predictive maintenance as an operational efficiency lever.

Global Managed Print Services Market Trends and Insights

Remote Work Print Infrastructure Optimisation Driving MPS Adoption in North America

Hybrid work has turned distributed print into a cost and security risk, prompting firms to consolidate device management in the cloud. Enterprises are adopting secure-print release, user authentication, and encrypted job routing to maintain compliance while supporting employees who print at headquarters, branch offices, or home. Sharp's Synappx Cloud Print targets this requirement, retaining job metadata only and reinforcing Zero Trust principles, a design favoured by US-based financial institutions and healthcare systems. Subscription pricing aligns spending to usage, eliminates server upkeep, and offers dashboards that benchmark sustainability metrics.

Sustainability and Carbon Footprint Mandates Accelerating EU Corporate MPS

EU climate policies now make verified CO2 reduction a procurement criterion. Duplex defaults, automated toner recycling, and paper-use analytics enable documented 60% emissions cuts relative to single-sided workflows, satisfying Corporate Climate Responsibility Monitor benchmarks that call for 30-33% footprint reductions by 2030. Corporates therefore award multi-year MPS contracts to providers demonstrating auditable lifecycle analytics and low-energy devices, putting a premium on fleets certified to Blue Angel or EPEAT Gold standards.

Declining Office Print Volumes Amid Digital Transformation in Nordics

Scandinavian corporations lead in e-signatures and digital archives, cutting per-employee print by double digits. Traditional cost-per-page models suffer as baseline volumes drop, prompting providers to broaden scopes to workflow digitisation and content management. Nordic lessons foreshadow demand in other mature economies as e-invoicing becomes compulsory and paper elimination targets spread.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Subscription-based Everything-as-a-Service Models Among SMEs

- Rising Print-Device Security and Compliance Requirements in Healthcare and Government

- Data Sovereignty Concerns Hindering Cloud-based MPS in Government Agencies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Printer/Copier Manufacturers owned a 41% stake of managed print services market share in 2024 by bundling devices, firmware, and consumables into integrated service agreements. Their captive install base, intellectual property, and direct field-service networks create switching costs that defend renewals. HP logged Printing segment revenue of USD 4.2 billion with a 19.5% margin in FY25, demonstrating hardware-anchored profitability. System Integrators/Resellers, expanding at 10.8% CAGR, capitalise on multi-vendor neutrality to architect bespoke fleets for regulated clients. Their growth signals customer appetite for service depth over device brand. Independent Software Vendors target workflow bottlenecks, embedding analytics and print-security APIs that overlay diverse hardware, thereby widening the managed print services market for niche solutions.

Customers increasingly award contracts to partners able to quantify uptime, security compliance, and environmental metrics rather than sell per-unit toner. Manufacturers answer by opening device telemetry to integrators, co-developing analytics, and funding channel training. Resellers, meanwhile, cultivate vertical specialisation-such as HIPAA compliance templates-that lets them penetrate national account rosters previously dominated by OEMs.

On-premise fleets still represent 65% of managed print services market size in 2024, anchored by financial services, defence, and utilities whose governance policies restrict external data transit. Yet cloud deployments will grow 11.2% annually as enterprises migrate print servers to SaaS platforms, offloading patching, queue management, and driver certification. Sharp's Synappx architecture secures metadata only, leaving raw documents behind the firewall, a design pattern that mitigates sovereignty risks while capturing cloud scalability. Providers now package hybrid offerings that orchestrate on-premise output for sensitive workflows and cloud spooling for standard jobs, enabling firms to ease into public-cloud adoption while maintaining risk controls.

Cyber insurance prerequisites further accelerate cloud, given that SaaS vendors certify against SOC-2, ISO 27001, and FedRAMP faster than many enterprises can audit internal print servers. Early movers report 30-40% support ticket reductions, freeing IT staff for higher-value initiatives. The managed print services industry therefore pivots from device break-fix toward continuous optimisation supported by always-updated cloud analytics.

Managed Print Services Market is Segmented by Channel Type (Printer/Copier Manufacturers, System Integrators/Resellers, Independent Software Vendors (ISVs)), Deployment Mode (On-Premise, Cloud-Based), Organization Size (Small and Medium Enterprises (SMEs), Large Enterprises), End-User Vertical (BFSI, Healthcare, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America heads the managed print services market with a 37% slice, underpinned by mature IT ecosystems, early cloud adoption, and stringent governance standards. Enterprises routinely integrate secure-print release with identity-and-access-management suites, streamlining Zero Trust rollouts. Channel ecosystems are deep, with OEMs, resellers, and ISVs collaborating to deliver end-to-end automation from document capture to archiving. The market also benefits from aggressive sustainability commitments by US Fortune 500 firms, many of which have pledged carbon neutrality by 2030 and rely on print fleet optimisation for scope-3 reductions.

Asia-Pacific is the fastest climber, logging a 12.1% CAGR to 2030. Chinese manufacturers procure predictive-maintenance analytics to offset labour shortages and ensure 24 X 7 production, an opportunity seized by Canon, whose Printing Group sales hit Yen 2,522.7 billion (USD 16.8 billion) in 2024. India's outsourcing hubs increasingly embed secure pull printing in ISO 27001 compliance frameworks demanded by Western clients. Japan and South Korea balance advanced robotics with paper-workflow legacies, making cloud print orchestration a bridge technology for digital transformation. Southeast Asian SMEs adopt subscription MPS to avoid capex, contributing incremental but rapid volumes.

Europe exhibits high digital maturity yet remains lucrative owing to sustainability policy headwinds. Companies must document lifecycle impacts under the EU Corporate Sustainability Reporting Directive, prompting widespread fleet audits and device consolidation. Nordic markets, in particular, show declining page volumes but buy workflow digitisation layered onto remaining devices. Germany, the United Kingdom, and France sustain demand through complex multi-site enterprises and public-sector contracts that require advanced security certifications such as BSI C5. Providers differentiate by offering carbon-footprint dashboards and automated carbon offset purchasing tied to print metrics.

- Xerox Corporation

- Ricoh Company, Ltd.

- HP Inc.

- Canon Inc.

- Brother Industries, Ltd.

- Lexmark International, Inc.

- Konica Minolta, Inc.

- Samsung Electronics Co., Ltd.

- Kyocera Document Solutions Inc.

- Sharp Corporation

- Epson (Seiko Epson Corporation)

- Toshiba Tec Corporation

- FujiFilm Business Innovation Corp.

- Dell Technologies Inc.

- PrintFleet (ECI Software Solutions)

- PaperCut Software International

- Quadient SA

- Arc Document Solutions, Inc.

- EFI (Electronics For Imaging, Inc.)

- FlexPrint Managed Print Solutions

- OKI Electric Industry Co., Ltd.

- Pitney Bowes Inc.

- Wipro Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Remote Work Print Infrastructure Optimization Driving MPS Adoption in North America

- 4.2.2 Sustainability and Carbon Footprint Mandates Accelerating EU Corporate MPS

- 4.2.3 Shift Toward Subscription-based Everything-as-a-Service Models Among SMEs Drives the Market

- 4.2.4 Rising Print-Device Security and Compliance Requirements in Healthcare and Government

- 4.2.5 IoT-Enabled Fleet Analytics Reducing Downtime in Large Asian Enterprises Drives the Market

- 4.3 Market Restraints

- 4.3.1 Declining Office Print Volumes Amid Digital Transformation in Nordics Hinders the Market

- 4.3.2 Data Sovereignty Concerns Hindering Cloud-based MPS in Government Agencies

- 4.3.3 Vendor Lock-in Perception and Contract Complexity Discouraging SMEs

- 4.3.4 Capex-to-Opex Accounting Shift Resistance in Emerging South Asian Markets Restraints the Market

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Channel Type

- 5.1.1 Printer/Copier Manufacturers

- 5.1.2 System Integrators/Resellers

- 5.1.3 Independent Software Vendors (ISVs)

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud-based

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-user Vertical

- 5.4.1 BFSI

- 5.4.2 Healthcare

- 5.4.3 IT and Telecom

- 5.4.4 Government

- 5.4.5 Education

- 5.4.6 Other End-user Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC (Saudi Arabia, UAE, Qatar)

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Xerox Corporation

- 6.4.2 Ricoh Company, Ltd.

- 6.4.3 HP Inc.

- 6.4.4 Canon Inc.

- 6.4.5 Brother Industries, Ltd.

- 6.4.6 Lexmark International, Inc.

- 6.4.7 Konica Minolta, Inc.

- 6.4.8 Samsung Electronics Co., Ltd.

- 6.4.9 Kyocera Document Solutions Inc.

- 6.4.10 Sharp Corporation

- 6.4.11 Epson (Seiko Epson Corporation)

- 6.4.12 Toshiba Tec Corporation

- 6.4.13 FujiFilm Business Innovation Corp.

- 6.4.14 Dell Technologies Inc.

- 6.4.15 PrintFleet (ECI Software Solutions)

- 6.4.16 PaperCut Software International

- 6.4.17 Quadient SA

- 6.4.18 Arc Document Solutions, Inc.

- 6.4.19 EFI (Electronics For Imaging, Inc.)

- 6.4.20 FlexPrint Managed Print Solutions

- 6.4.21 OKI Electric Industry Co., Ltd.

- 6.4.22 Pitney Bowes Inc.

- 6.4.23 Wipro Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment