PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910592

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910592

China Online Travel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

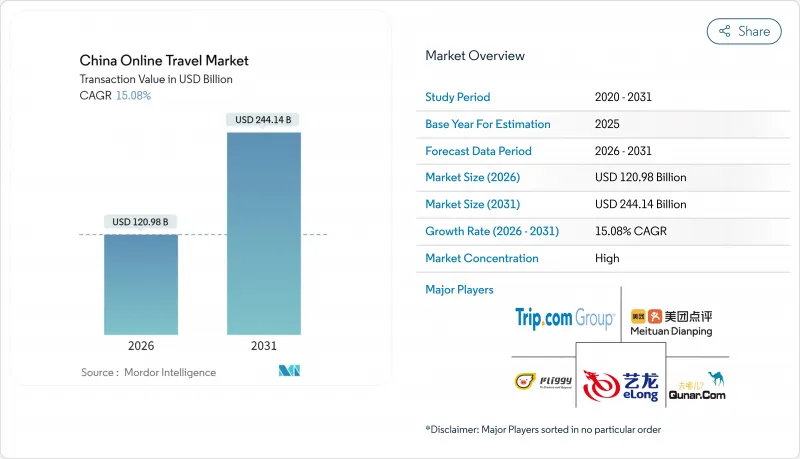

The China online travel market was valued at USD 105.12 billion in 2025 and estimated to grow from USD 120.98 billion in 2026 to reach USD 244.14 billion by 2031, at a CAGR of 15.08% during the forecast period (2026-2031).

Rising digital literacy, a nationwide pivot toward mobile commerce, and supportive tourism policies collectively keep the growth curve steep. Tier-3 to Tier-5 cities, where first-time travelers now transact almost entirely through super-apps, add a fresh layer of momentum. Established online travel agencies (OTAs) reinforce their positions through AI-powered personalization, dynamic pricing, and bundled lifestyle offerings that raise user stickiness. Relaxed visa regimes and expanded airlift unlock outbound demand, while domestic tourism benefits from high-speed rail connectivity and government-funded destination upgrades.

China Online Travel Market Trends and Insights

High Internet and Smartphone Penetration

Smartphone subscriptions now exceed 1.7 billion, and 5G coverage is near-ubiquitous. This connectivity removes physical barriers to booking, especially in smaller cities where brick-and-mortar agencies were scarce. Ubiquitous mobile wallets such as Alipay and WeChat Pay compress checkout times to seconds, even for first-time travelers. Younger cohorts translate that convenience into spontaneous weekend trips, while platforms harvest clickstream data to refine real-time recommendations. The virtuous cycle of wider access, better personalization, and simplified payment keeps the China online travel market on a steep uptake curve.

Government Support for Domestic Tourism

Beijing's three-year plan for cultural tourism established 19 May as China Tourism Day and bundles tax concessions with bank-subsidized travel coupons to spur local trips. Provincial governments replicate the model with heritage-themed festivals and transport subsidies that lift mid-week hotel occupancy. Policy clarity reduces operator risk, prompting sustained investment in cloud-based reservation systems and data analytics. By directly linking subsidies to digital transactions, authorities funnel incremental traffic toward online platforms, reinforcing the structural shift away from offline channels.

Regulatory Crackdowns on Tech and Data

The Cross-border Data Flow Provisions require security assessments for outbound data deemed sensitive, compelling OTAs to localize servers and deploy encryption. Compliance outlays erode smaller players' margins and slow feature roll-outs. Yet clarified guidelines are also reducing gray zones, letting well-capitalized incumbents incorporate privacy-preserving AI models with government-approved safeguards. Long-run effects, therefore, skew toward consolidation rather than outright contraction.

Other drivers and restraints analyzed in the detailed report include:

- Economic Uncertainty and Consumer Caution

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Accommodation booking steered 42.14% of the China online travel market in 2025, translating to deep commission pools that fund aggressive loyalty campaigns. AI-powered filters parse guest reviews and real-time rate parity to surface room types aligned with individual budgets and amenity priorities. That granular targeting keeps cancellation rates low, boosting hotel-OTA alignment. Holiday package booking, projected to grow at 16.61% CAGR, appeals to new travelers from Tier 3 cities who prefer turnkey itineraries that bundle transport, lodging, and insurance under one QR code.

The accommodation subsector now spills into alternative inventory: homestays, serviced apartments, and pop-up "glamping" pods in lesser-known scenic zones. Major OTAs integrate user-generated micro-videos to preview properties, converting inspiration to booking within the same scroll cycle. Meanwhile, add-on services are airport transfers, local SIM cards, and attraction e-tickets to create ancillary revenue streams that move platforms closer to one-stop lifestyle ecosystems.

Leisure accounted for 75.10% of the China online travel market in 2025, buoyed by social-media storytelling and flash-sale channels that spark impromptu getaways. Short-distance "micro-vacations" drive weekday demand spikes, smoothing seasonality for operators. Business travel, growing at 12.41% CAGR, rebounds as corporations resume in-person deal-making. Digital travel-management dashboards cum expense platforms integrate policy compliance, decision support, and live rebooking, letting finance teams track carbon output and per-diem metrics.

Hybrid "bleisure" itineraries blur segment lines: executives tack a weekend onto a client visit, swelling average stay lengths and cab ride receipts. OTAs curate bundles that align corporate hotel caps with leisure upgrade options, such as spa credits or attraction passes financed through employee wellness budgets.

The China Online Travel Market is Segmented by Service Type (Accommodation Booking, Travel Tickets Booking, and More), Traveler Type (Leisure, Business, VFR, and Others), Mode of Booking (OTA / Travel Agent, and Supplier Direct), Destination Type (Domestic, Outbound, and Inbound) Age Group (Gen Z, Millennials and More), Region (Central China, East China and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Jin Jiang International Holdings Co., Ltd.

- Huazhu Group Ltd.

- BTG Homeinns Hotels Group Co., Ltd.

- GreenTree Hospitality Group Ltd.

- Atour Lifestyle Holdings Ltd.

- Dossen International Group

- Dongcheng International Hotel Group

- Plateno Group

- Zhejiang New Century Hotel Management Co., Ltd.

- Shanghai Jin Mao Hotel Investments & Mgmt

- Marriott International Inc.

- Hilton Worldwide Holdings Inc.

- InterContinental Hotels Group PLC

- Accor SA

- Wyndham Hotels & Resorts Inc.

- Hyatt Hotels Corp.

- Shangri-La Asia Ltd.

- MGM China Holdings Ltd.

- Sunac Culture & Tourism Group

- Tongcheng-Elong Holdings Ltd.*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urbanization & Infrastructure Development

- 4.2.2 Government Support & Policies Promoting Inbound and Domestic Tourism

- 4.2.3 Expansion of Luxury and Boutique Hotels

- 4.2.4 Increase in Event-Driven Tourism (MICE, Sports, Mega-Events)

- 4.2.5 Growth in Domestic Tourism

- 4.3 Market Restraints

- 4.3.1 Lingering Pandemic-Era Visa & Quarantine Friction for Inbound Travelers

- 4.3.2 Intensifying Price Competition Among Domestic Hotel Chains

- 4.3.3 Rising ESG Compliance Costs for Hotel Properties

- 4.3.4 Geopolitical Tensions Dampening Long-Haul Source Markets

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Supplier Power

- 4.6.2 Buyer Power

- 4.6.3 Threat of Substitutes

- 4.6.4 Threat of New Entrants

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Tourism Type

- 5.1.1 Domestic Tourism

- 5.1.2 Inbound Tourism

- 5.1.3 Outbound Tourism

- 5.2 By Purpose

- 5.2.1 Leisure & Adventure & Eco-Tourism

- 5.2.2 Business / MICE

- 5.3 By Traveler Age

- 5.3.1 Generation Z (18-24)

- 5.3.2 Millennials (25-40)

- 5.3.3 Generation X (41-56)

- 5.3.4 Baby Boomers (57+)

- 5.4 By Booking Channel

- 5.4.1 Online Travel Agencies (OTAs)

- 5.4.2 Direct Hotel Websites & Apps

- 5.4.3 Offline Travel Agencies

- 5.5 By Hotel Category

- 5.5.1 Economy / Budget Hotels

- 5.5.2 Mid-scale Hotels

- 5.5.3 Upscale Hotels

- 5.5.4 Luxury Hotels

- 5.5.5 Serviced Apartments & Long-Stay

- 5.6 By Ownership / Branding

- 5.6.1 Independent Hotels

- 5.6.2 Domestic Chain-Affiliated Hotels

- 5.6.3 International Chain-Affiliated Hotels

- 5.7 By Region

- 5.7.1 Central China

- 5.7.2 East China

- 5.7.3 North China

- 5.7.4 Northeast China

- 5.7.5 Northwest China

- 5.7.6 South China

- 5.7.7 Southwest China

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Jin Jiang International Holdings Co., Ltd.

- 6.4.2 Huazhu Group Ltd.

- 6.4.3 BTG Homeinns Hotels Group Co., Ltd.

- 6.4.4 GreenTree Hospitality Group Ltd.

- 6.4.5 Atour Lifestyle Holdings Ltd.

- 6.4.6 Dossen International Group

- 6.4.7 Dongcheng International Hotel Group

- 6.4.8 Plateno Group

- 6.4.9 Zhejiang New Century Hotel Management Co., Ltd.

- 6.4.10 Shanghai Jin Mao Hotel Investments & Mgmt

- 6.4.11 Marriott International Inc.

- 6.4.12 Hilton Worldwide Holdings Inc.

- 6.4.13 InterContinental Hotels Group PLC

- 6.4.14 Accor SA

- 6.4.15 Wyndham Hotels & Resorts Inc.

- 6.4.16 Hyatt Hotels Corp.

- 6.4.17 Shangri-La Asia Ltd.

- 6.4.18 MGM China Holdings Ltd.

- 6.4.19 Sunac Culture & Tourism Group

- 6.4.20 Tongcheng-Elong Holdings Ltd.*

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment