PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851060

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851060

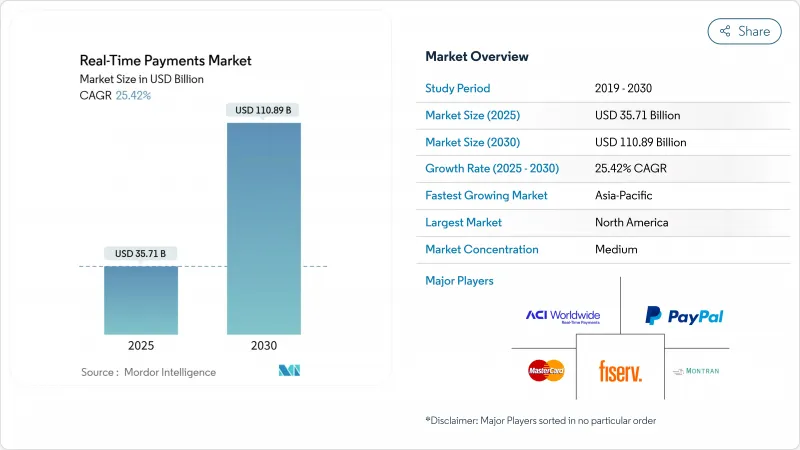

Real-Time Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Real Time Payments market size stands at USD 35.71 billion in 2025 and is forecast to achieve USD 110.89 billion by 2030, reflecting a compelling 25.42% CAGR.

Surging adoption originates from regulatory mandates, the November 2025 ISO 20022 deadline, and customer demand for instantaneous settlement across retail, payroll, and bill-payment workflows. In North America, the FedNow rail welcomed 1,300 institutions by April 2025 and processed 1.31 million transactions worth USD 48.6 billion during Q1 2025, underscoring strong network effects. Europe's Instant Payments Regulation, effective January 2025, requires 24/7 euro-zone coverage, accelerating bank technology investment. Asia-Pacific's momentum is reinforced by India's UPI expansion into additional corridors and Singapore's Project Nexus, while Brazil's PIX processed 42 billion transactions worth BRL 17.2 trillion (USD 3.44 trillion) in 2023, highlighting the scale benefits of government-sponsored schemes.

Global Real-Time Payments Market Trends and Insights

ISO 20022 migration accelerates infrastructure modernization

The November 2025 ISO 20022 deadline compels banks to update messaging and processing engines simultaneously, making real-time payment rail adoption the most cost-efficient compliance path. SWIFT notes that 32.9% of cross-border messages already ride ISO 20022, up six percentage points in Q4 2024. Richer data payloads improve sanctions screening, and Deutsche Bank showcases real-time compliance benefits for corporates. The looming end of the coexistence period forces institutions to avoid dual-system overhead. Community banks mitigate capability gaps by outsourcing to third-party processors that bundle ISO 20022 translation with instant-payment connectivity.

FedNow expansion drives Americas market leadership

FedNow's network effects were evident with a 43.1% quarterly volume spike in Q1 2025 and a 140.8% value leap, signalling widening commercial use cases. The Federal Reserve's ambition to onboard 8,000 institutions positions the rail for nationwide ubiquity. In parallel, Brazil's PIX 2.0 will introduce recurring and instalment capabilities in September 2025, showing how mature systems evolve into multifunction platforms. Combined, these initiatives set cross-continental performance benchmarks that other markets emulate.

Fraud monitoring complexity constrains adoption velocity

Verification-of-Payee frameworks differ across schemes, obliging banks to invest in separate rule sets for FedNow, PIX, and SEPA Instant. ACI Worldwide's European PoC with Banfico illustrates workaround partnerships to meet the EU's October 2025 compliance deadline. Visa's Featurespace acquisition underscores the capital-intensive nature of AI-based instant fraud detection. Smaller institutions face operational strain from parallel systems, slowing onboarding to multiple networks.

Other drivers and restraints analyzed in the detailed report include:

- Earned-wage access transforms payroll economics

- Cross-border RTP corridors reshape international payments

- Legacy infrastructure modernization challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Peer-to-peer transfers accounted for 55.1% of Real Time Payments market revenue in 2024, underscoring widespread consumer adoption. Business-driven flows now outpace personal transfers, with peer-to-business transactions growing 28.61% annually as instant payroll disbursements and merchant settlement take hold. FedNow's early corporate pilots in payroll and supplier payments highlight this pivot, signalling that working-capital benefits resonate with finance executives. Business-to-business adoption remains in early stages but promises the largest addressable pool, given ACH's multi-day settlement drag. Consumer-to-business flows gain momentum where buy-now-pay-later (BNPL) providers embed account-to-account settlement to minimise interchange costs. Brazil's PIX demonstrates this migration, with e-commerce merchants projected to book USD 30 billion in instant-payment turnover during 2025. Government-to-person mandates across GCC economies create a new baseline expectation for 24/7 disbursement, cementing instant infrastructure as a public-service standard.

Real-time salary advances reshape payroll economics, enlarging transaction frequency rather than ticket size, thus increasing absolute rail volume. Corporates synchronise treasury and AP processes, shifting from weekly payment runs to on-demand pushes. Cross-border organisations leverage bilateral links such as UPI-PayNow to shorten supplier settlement cycles in Southeast Asia. Market platforms introduce split-payment models that route commission and principal amounts simultaneously, removing reconciliation delays. These combined use cases reinforce the Real Time Payments market as indispensable for liquidity optimisation.

Platform & solution spending captured 75.6% of 2024 revenue, signalling that banks favour holistic overhauls versus tactical bolt-ons. ISO 20022 migration serves as the triggering event, since message translation, fraud analysis, and API orchestration are most efficient on unified stacks. Yet service revenue rises 29.23% annually, reflecting heavy reliance on specialist integrators for phased rollout. Consulting engagements cover readiness assessments, roadmap design, and regulatory gap analysis. Institutions outsource managed services for SLAs covering 24/7 uptime, ensuring compliance while containing headcount. Integration partners such as ACI Worldwide logged 42% software-segment growth in Q1 2025, proving that combinational platform-plus-professional-services deals resonate with mid-tier institutions.

Over the forecast period, middleware capable of orchestrating real-time and batch flows side-by-side becomes critical. Hybrid-cloud orchestrators with containerised microservices enable progressive decoupling from legacy cores. This architecture allows banks to retire mainframe modules gradually while front-ending customers with instant-payment APIs. Training programmes address the operational culture shift to continuous settlement and real-time liquidity monitoring.

The Global Real-Time Payments Market is Segmented by Transaction Type (Peer-To-Peer (P2P), Peer-To-Business (P2B)), Component (Platform / Solution, Services), Deployment (Cloud, On-Premise), Enterprise Size (Large Enterprises, Small and Medium Enterprises), End-User Industry (Retail and E-Commerce, BFSI, Utilities & Telecom, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America posted 38.1% revenue share in 2024, anchored by FedNow and The Clearing House RTP network maturity. Volume growth accelerates as regional banks join en masse, aided by packaged cloud connectors. Regulatory clarity on interchange treatment for instant debit pushes merchant adoption. Canada plans Real-Time Rail launch in 2026, which could open a USD-denominated cross-border corridor with the United States.

Asia-Pacific delivers the highest CAGR at 29.33% to 2030. India's UPI handled 131 billion transactions worth INR 200 trillion (USD 2.4 trillion) in FY24, illustrating scale benefits of a government-backed open API model. Singapore's Project Nexus presents a template for multi-country clearing, while Australia's NPP finalises PayTo mandates, expanding business billing capabilities. Japan's regional banks accelerate modernization to meet the national cashless-ratio target.

Europe's mandatory 24/7 receiving requirement effective January 2025 induced a 27% instant-payment jump at Deutsche Bank that same month. Full send capability by October 2025 will drive further adoption yet may squeeze fee margins given regulation-imposed price caps. Nordic P27's pause leaves SEPA Instant as the de-facto cross-border option inside Europe, pushing banks toward bilateral links with the UK's FPS.

South America's trajectory centres on PIX, now extending to instalment and offline modes that remove the last cash use-cases. Colombia, Chile, and Argentina examine replicating PIX's public-private partnership structure. The Middle East experiences policy-driven growth where Saudi Arabia's Sarie rail and the UAE's IPP mandate instant salary credits for government workers. Africa witnesses mobile-money players integrating open-loop instant rails, blending wallet ubiquity with bank-grade clearing.

- ACI Worldwide Inc.

- Fiserv Inc.

- PayPal Holdings Inc.

- Mastercard Inc.

- Montran Corporation

- FIS Global

- Temenos AG

- Volante Technologies Inc.

- Finastra Inc.

- Ant Group (Alipay)

- Tencent Holdings Ltd. (WeChat Pay)

- The Clearing House Payments Co.

- Visa Inc.

- SWIFT SCRL

- Worldline SA

- Nets Group

- Nexi SpA

- Ripple Labs Inc.

- Wise PLC

- Pay.UK

- GoCardless Ltd.

- Jack Henry and Associates Inc.

- Infosys Finacle

- VSoft Corporation

- OpenPayd Holdings Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of ISO 20022-enabled domestic rails in Europe and Asia-Pacific

- 4.2.2 Expansion of FedNow and upcoming PIX 2.0 accelerating adoption in the Americas

- 4.2.3 Real-time payroll and earned-wage access (EWA) demand among U.S. gig workers

- 4.2.4 BNPL players shifting to RTP for instant merchant settlement in Europe

- 4.2.5 Government mandates for instant salary and welfare disbursement in GCC countries

- 4.2.6 Surging cross-border RTP corridors via RippleNet and Visa Direct

- 4.3 Market Restraints

- 4.3.1 Fragmented fraud-monitoring standards across RTP schemes

- 4.3.2 Legacy core-bank modernisation backlog in Tier-2 Asian banks

- 4.3.3 Interoperability gaps between card tokenisation and account-to-account rails

- 4.3.4 Merchant surcharge regulation uncertainty in the U.S.

- 4.4 Value Chain Analysis

- 4.5 Regulatory and Standards Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of Macro Economic Trends on the Market

- 4.8 Case Studies and Use-cases

- 4.9 RTP Transactions as % of All Transactions - Regional and Key-Country Split

- 4.10 RTP Transactions as % of Non-Cash Transactions - Regional and Key-Country Split

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Transaction Type

- 5.1.1 Peer-to-Peer (P2P)

- 5.1.2 Peer-to-Business (P2B)

- 5.2 By Component

- 5.2.1 Platform / Solution

- 5.2.2 Services

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-Premise

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End-User Industry

- 5.5.1 Retail and E-Commerce

- 5.5.2 BFSI

- 5.5.3 Utilities and Telecom

- 5.5.4 Healthcare

- 5.5.5 Government and Public Sector

- 5.5.6 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Spain

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Colombia

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)}

- 6.4.1 ACI Worldwide Inc.

- 6.4.2 Fiserv Inc.

- 6.4.3 PayPal Holdings Inc.

- 6.4.4 Mastercard Inc.

- 6.4.5 Montran Corporation

- 6.4.6 FIS Global

- 6.4.7 Temenos AG

- 6.4.8 Volante Technologies Inc.

- 6.4.9 Finastra Inc.

- 6.4.10 Ant Group (Alipay)

- 6.4.11 Tencent Holdings Ltd. (WeChat Pay)

- 6.4.12 The Clearing House Payments Co.

- 6.4.13 Visa Inc.

- 6.4.14 SWIFT SCRL

- 6.4.15 Worldline SA

- 6.4.16 Nets Group

- 6.4.17 Nexi SpA

- 6.4.18 Ripple Labs Inc.

- 6.4.19 Wise PLC

- 6.4.20 Pay.UK

- 6.4.21 GoCardless Ltd.

- 6.4.22 Jack Henry and Associates Inc.

- 6.4.23 Infosys Finacle

- 6.4.24 VSoft Corporation

- 6.4.25 OpenPayd Holdings Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment