PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851139

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851139

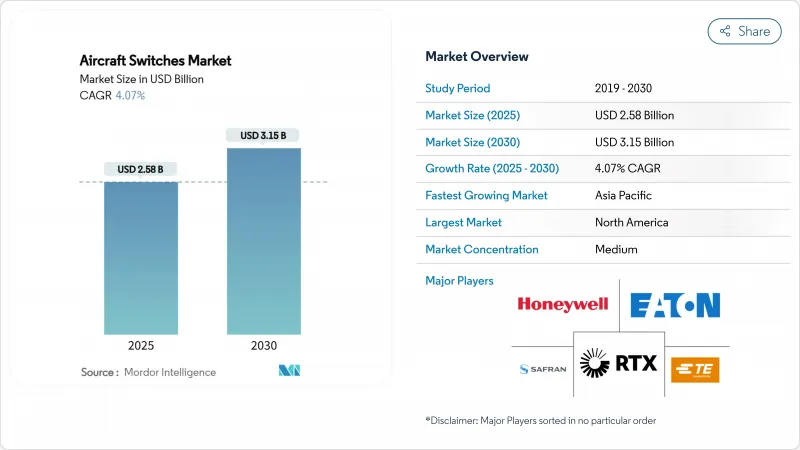

Aircraft Switches - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The aircraft switches market size was valued at USD 2.58 billion in 2025 and is forecasted to expand to USD 3.15 billion by 2030, advancing at a 4.07% CAGR.

This trajectory mirrors the aviation sector's steady pivot toward more-electric architectures, where electrical subsystems replace legacy mechanical and hydraulic components, multiplying the number of switching points across each airframe. Airlines' fleet-renewal schedules and defense modernization programs ensured a consistent order flow for both commercial and military platforms in 2024 and early 2025. Solid-state power controllers, silicon-carbide devices, and smart switches with built-in diagnostics became mainstream as the emphasis shifted from discrete electromechanical parts to software-defined, data-sharing modules capable of predictive maintenance integration. Vendor selection criteria increasingly include cybersecurity compliance and supply-chain integrity, forcing mid-tier suppliers either to invest in certification upgrades or accept consolidation offers from larger peers. Across regions, North America retained the revenue lead owing to sustained defense spending. Yet, Asia-Pacific posted the fastest growth as China and India accelerated aircraft production and MRO capacity expansion.

Global Aircraft Switches Market Trends and Insights

Fleet Renewal Wave in Next-Gen Narrow-Body Programs

Airlines accelerated replacement of aging single-aisle fleets in 2024, specifying electrical architectures that require denser switching networks for power distribution and flight-deck controls. Boeing's B777X certification effort and Air India's large multitype order packages typified how every new delivery triggered bundled switch installations spanning cockpit, avionic bay, and cabin zones.Operators insisted on future-proof hardware able to accommodate software upgrades across the 20-year airframe life, favoring suppliers offering configurable solid-state units with health-monitoring outputs.

Surge in More-Electric Subsystems Requiring Solid-State Switching

Aircraft electrification expanded from secondary systems to high-power actuation lines, pushing switch ratings beyond 500A and 1,000V. Collins Aerospace prototyped megawatt-class power-distribution modules under the Clean Aviation SWITCH program, validating silicon-carbide devices for continuous high-temperature operation. Honeywell's silicon-on-insulator CMOS processes supported components rated to 300°C, enabling power-conversion bays to migrate closer to engines and reducing harness weight. These advances underpinned the aircraft switches market as platform OEMs shifted to distributed electrical propulsion concepts.

Qualified-Component Certification Queue Delays

FAA and EASA engineering directorates faced case backlogs as cybersecurity and software assurance reviews deepened, stretching component approval lead times from 12 months to more than 24 months. Boeing's B777X program delays highlighted the cascading impact on tier-1 and tier-2 suppliers waiting for type-certification data to finalize production release. Smaller switch vendors lacking dedicated certification teams risked losing line-fit positions, tempering overall aircraft switches market momentum.

Other drivers and restraints analyzed in the detailed report include:

- Cabin-Retrofit Boom for IFEC and Lighting Upgrades

- Rapid Military Rotorcraft Recapitalization Budgets

- Cyber-Hardening Requirements Raising BOM Cost of Smart Switches

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cockpit switches retained 35.65% of 2024 revenue as pilots relied on tactile pushbuttons, guarded toggles, and rotary selectors for flight-critical tasks. Manual designs dominated because regulators required physical backup control lines in case of display or data bus failure. The segment benefited from sustained deliveries of single-aisle aircraft, where standardized overhead panels simplified integration and lowered per-unit costs.

Avionics installations generated the fastest 5.04% CAGR forecast through 2030. Multi-function displays, flight-management computers, and health-monitoring units demanded high-density, low-bounce automatic relays linked over Ethernet-based backbones. Airlines embedded smart switches that streamed usage data into predictive-maintenance platforms, improving dispatch reliability. Overall, avionics growth supported incremental additions to the aircraft switches market size for integrated modular avionics suites.

Manual units supplied 65.40% revenue in 2024, led by pushbutton assemblies preferred for clear tactile affirmation and straightforward line maintenance. Rocker variants won cabin positions where design language and illumination effects improved passenger perception. Manual demand preserved manufacturing economies of scale and stable replacement part numbers across multiple fleets.

Automatic switches are projected to climb at a 5.91% CAGR as more-electric architectures substitute electromechanical contactors with solid-state controllers. Hybrid relays that pair arc-free semiconductor paths with mechanical redundancy entered serial production, combining low voltage drop with fail-safe positioning. This migration enlarges the aircraft switches market as each power-distribution center now contains dozens of intelligent, addressable switches instead of a handful of legacy breakers.

The Aircraft Switches Market Report is Segmented by Application (Cockpit, Cabin, Engine and Power Auxiliary Power Unit (APU), Avionics, and Others), Switch Type (Manual and Automatic), Platform (Fixed-Wing Aircraft, Rotary-Wing Aircraft, and Unmanned Aerial Vehicles), End User (OEM and Aftermarket), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 37.80% of 2024 revenue, underpinned by comprehensive defense budgets and active commercial production lines. Boeing, Honeywell, Curtiss-Wright, and Eaton anchored the regional supplier ecosystem, while FAA certification expertise concentrated program approvals within the United States borders. Several USD 10 billion-plus contracts for NGAD and helicopter upgrades ensured consistent switch demand across fighter, tanker, and rotorcraft categories.

Asia-Pacific, forecast to expand at 5.60% CAGR, benefited from China's climb up the MRO value chain and India's surging aircraft orders. Airbus projected China's services segment to reach USD 61 billion by 2043, with maintenance representing 83%-a switch-intensive activity. India's government earmarked USD 12 billion for airport expansion and encouraged local component production, prompting Western suppliers to establish joint ventures, as seen in Eaton's partnership with SIAEC. The region's focus on indigenization opened opportunities for mid-sized players to license technology and capture domestic content quotas.

Europe remained stable, supported by Airbus assembly, defense cooperation under GCAP, and R&D projects backed by EU climate funds. Collins Aerospace's Clean Aviation SWITCH prototypes in France and Ireland validated high-voltage distribution strategies for hybrid-electric demonstrators, elevating regional intellectual-property stakes. Simultaneously, EASA's cybersecurity mandates heightened certification complexity, favoring suppliers with in-house compliance resources and thus maintaining moderate barriers to entry within the aircraft switches market.

- Safran SA

- Honeywell International Inc.

- Eaton Corporation plc

- TE Connectivity Corporation

- RTX Corporation

- AMETEK, Inc.

- ITT Inc.

- CandK COMPONENTS LLC

- Electro-Mech Components, Inc.

- Unison Industries, LLC.

- Hydra-Electric Company

- Sensata Technologies, Inc.

- Vishay Intertechnology, Inc.

- Curtiss-Wright Corporation

- Schurter Holding AG

- Cygnet Aerospace Corp.

- Barantech

- Pressure Controls, Inc.

- AstroNova, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Fleet renewal wave in next-gen narrow-body programs

- 4.2.2 Surge in more-electric subsystems requiring solid-state switching

- 4.2.3 Cabin-retrofit boom for IFEC and lighting upgrades

- 4.2.4 Rapid military rotorcraft recapitalization budgets

- 4.2.5 Data-driven predictive-maintenance contracts bundling smart switches

- 4.2.6 Silicon-on-insulator (SOI) power-device breakthroughs enabling ultra-compact relays

- 4.3 Market Restraints

- 4.3.1 Qualified-component certification queue delays at FAA and EASA

- 4.3.2 Raw-material price volatility for silver-cadmium oxide contacts

- 4.3.3 Counterfeit part infiltration in MRO supply chains

- 4.3.4 Cyber-hardening requirements raising BOM cost of smart switches

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Cockpit

- 5.1.2 Cabin

- 5.1.3 Engine and Power Auxiliary Power Unit (APU)

- 5.1.4 Avionics

- 5.1.5 Others

- 5.2 By Switch Type

- 5.2.1 Manual

- 5.2.1.1 Pushbutton Switches

- 5.2.1.2 Toggle Switches

- 5.2.1.3 Rocker Switches

- 5.2.1.4 Rotary Switches

- 5.2.1.5 Others

- 5.2.2 Automatic

- 5.2.2.1 Pressure Swicthes

- 5.2.2.2 Temperature Switches

- 5.2.2.3 Flow Switches

- 5.2.2.4 Relays and Contactor Switches

- 5.2.2.5 Others

- 5.2.1 Manual

- 5.3 By Platform

- 5.3.1 Fixed-wing Aircraft

- 5.3.2 Rotary-wing Aircraft

- 5.3.3 Unmanned Aerial Vehicles (UAV)

- 5.4 By End User

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Safran SA

- 6.4.2 Honeywell International Inc.

- 6.4.3 Eaton Corporation plc

- 6.4.4 TE Connectivity Corporation

- 6.4.5 RTX Corporation

- 6.4.6 AMETEK, Inc.

- 6.4.7 ITT Inc.

- 6.4.8 CandK COMPONENTS LLC

- 6.4.9 Electro-Mech Components, Inc.

- 6.4.10 Unison Industries, LLC.

- 6.4.11 Hydra-Electric Company

- 6.4.12 Sensata Technologies, Inc.

- 6.4.13 Vishay Intertechnology, Inc.

- 6.4.14 Curtiss-Wright Corporation

- 6.4.15 Schurter Holding AG

- 6.4.16 Cygnet Aerospace Corp.

- 6.4.17 Barantech

- 6.4.18 Pressure Controls, Inc.

- 6.4.19 AstroNova, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment