PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851166

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851166

Smart Plug - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

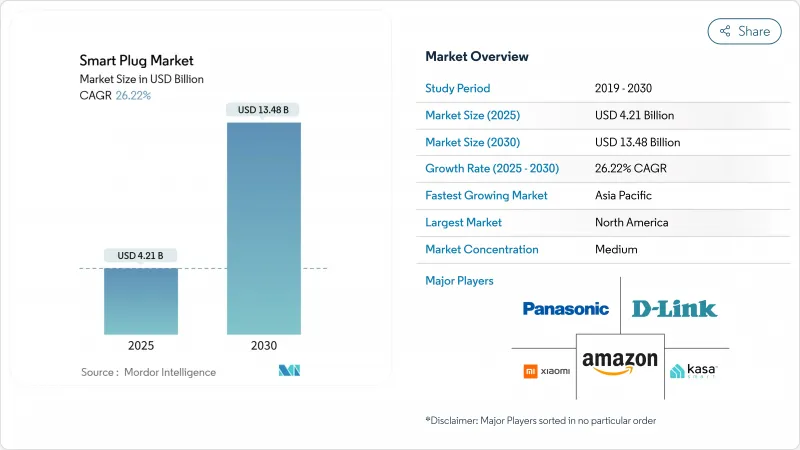

The smart plug market stands at USD 4.21 billion in 2025 and is on course to reach USD 13.48 billion in 2030, charting a 26.22% CAGR.

This acceleration stems from mandatory energy-efficiency rules that make plug-load controls a building-code staple, the rapid decline of Wi-Fi chipset prices that brings sub-USD 10 retail tags into play, and the Matter 1.3 interoperability standard that dissolves long-standing ecosystem silos. Voice-assistant ecosystems now anchor purchasing decisions, while ultra-low-power Wi-Fi 6 MCUs shrink standby draw to micro-amp levels and enable multi-year battery use. Rising industrial interest, driven by audits showing up to 36.8 kW in annual plug-load waste per facility, positions smart plugs as a frontline efficiency retrofit. Regional momentum tilts toward Asia Pacific, where Alexa device connections have tripled in India and local chipset suppliers cut bill-of-materials costs for domestic brands.

Global Smart Plug Market Trends and Insights

Soaring Adoption of Voice-Assistant Ecosystems

Voice control has shifted from novelty to necessity as Amazon reports a 200% jump in connected smart-home devices in India within three years. The 2025 debut of the USD 19.99-per-month Alexa+ generative-AI service, bundled into Prime, redefines the value proposition from simple on/off switching to multi-device scene orchestration. Subscription economics incentivize deeper engagement, positioning smart plugs as foundational nodes that extend voice-assistant reach to legacy appliances. With more than 140,000 compatible devices in the Alexa catalogue, network effects reduce adoption friction and lift attach rates across income bands. Comparable strategies from Google and Apple reinforce the perception that voice-ready control is now the baseline expectation for every new plug-in device.

Falling ASPs of Wi-Fi Chipsets

Silicon Labs' SiWx917 MCU trims connected-sleep current to 22 micro amp, slicing component costs and enabling sub-USD 15 retail pricing without sacrificing energy reporting features. Synaptics and Chinese newcomer AIC Micro have entered the USD 3.2 billion ultra-low-power IoT SoC arena, intensifying price competition and widening vendor choice. Mass-market volumes allow ODMs to package dual Wi-Fi/BLE modules inside compact casings while retaining Matter-ready firmware. Emerging economies benefit most, as unit economics now align with middle-income household budgets, expanding the install base beyond early adopters.

Persistent Device Cybersecurity Breaches

Smart-device cyberattacks more than doubled in 2024, eroding consumer trust as high-profile flaws surfaced in major brands. TP-Link's exposure of local-communication vulnerabilities and the Mars Hydro incident that leaked 2.7 billion IoT records underscore systemic risk. The U.S. FCC's upcoming Cyber Trust Mark, backed by Amazon and Google, promises clearer labeling but final rules are not yet in force. Product recalls such as Emporia Energy's withdrawal of 80,000 smart plugs due to shock hazards illustrate the financial toll of insufficient security controls. Until certification regimes become mandatory, lingering doubts may slow first-time purchases, especially in professionally managed facilities with stricter IT policies.

Other drivers and restraints analyzed in the detailed report include:

- Government Energy-Efficiency Mandates for Plug-Load Control

- Matter 1.3 Interoperability Push

- Fragmented RF Spectrum in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bluetooth retained the largest 31.7% slice of smart plug market share in 2024, but Zigbee/Thread protocols are accelerating at a 26.8% CAGR on the back of Matter certification momentum. The smart plug market size for Thread-enabled models is projected to swell sharply as enhanced credential-sharing in Thread 1.4 unlocks enterprise-grade deployments. Tuya's 15-day turnkey module program signals how standardization compresses time-to-market and lowers engineering hurdles. Wi-Fi enjoys cost-led ubiquity and excels in bandwidth-heavy use-cases such as high-resolution energy metering, while Z-Wave remains entrenched in legacy US security systems. Proprietary stacks risk obsolescence as consumers align around cross-platform purchase assurance.

Thread's real-time energy-reporting offers clear advantages in utility demand-response. Matter 1.3 now lets smart plugs feed instantaneous consumption data to broader home-energy-management dashboards. Consequently, utility rebates are beginning to single out Thread-capable hardware, incentivizing installers to pivot away from Wi-Fi-only SKUs. Vendors that overlay energy analytics atop Thread's low-latency mesh can charge premium ASPs, cushioning margin erosion in a commoditizing category.

Residential premises still represent 56.2% of the 2024 smart plug market size, buoyed by voice-assistant bundling and DIY convenience. Yet industrial and commercial buildings are set to expand at a 27.7% CAGR as facility managers chase quantified returns; field studies show 36.8 kW of annual plug-load savings per site when IoT scheduling is applied. Honeywell's plug-load module for enterprise building-management systems exemplifies the pivot to data-driven energy compliance.

In factories and warehouses, skinned industrial-grade smart plugs add thermal-overload protection and over-current analytics that residential units lack. Hospitals and elder-care facilities deploy smart plugs to verify medical-device uptime and prevent unplanned disconnection, aided by subsidy programs for remote monitoring in aging societies. The commercial appetite for SLA-backed hardware supports higher price points, widening the total addressable smart plug market for specialist OEMs.

Smart Plug Market is Segmented by Technology (Bluetooth, Wi-Fi, and More), Application (Residential, Commercial, and More), Sales Channel (Online and Offline), Plug Form Factor (Wall-Plug Adapter, In-Wall Outlet, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 32.1% leadership in 2024 on the strength of Energy Star SHEMS rules and broadband ubiquity, with utilities offering rebates for demand-response-certified plugs. The region's mature voice-assistant penetration fosters ecosystem lock-in that reduces churn and encourages whole-home retrofits. Canada's updated Energy Efficiency Regulations mirror U.S. standards, giving manufacturers a unified North American certification roadmap.

Asia Pacific is projected to clock a 28.3% CAGR, making it the fastest-expanding territory of the smart plug market. Localized voice-assistant dialect support and competitive pricing have tripled the Alexa device count in India since 2022. China's domestic chipset output curbs BOM volatility and allows white-label brands to proliferate. Government-funded smart-city pilots in Japan and South Korea integrate plug-level energy monitoring into district-wide carbon dashboards, seeding institutional demand for Thread-mesh deployments.

Europe presents a mixed picture. WEEE Directive 2024/884 places full end-of-life costs on manufacturers, pressuring gross margins. Conversely, the UK's 2025 smart-appliance rules require grid-aware functionality, widening the pool of devices that can benefit from retrofitting with Matter-ready smart plugs. Tuya's London retrofit forum underscored the role that low-cost plugs play in hitting net-zero targets for aging housing stock.

South America and the Middle East-Africa trail in installed base but register double-digit growth as 5G rollouts improve latency and coverage. High import duties remain a hurdle, prompting local assembly joint ventures that leverage regional free-trade zones. Developers tapped into hotel chains in the Gulf Cooperation Council to trial centralized energy dashboards, illustrating how smart plugs serve as a gateway product for broader IoT infrastructure.

- TP-Link Technologies

- Belkin (WeMo)

- Xiaomi

- D-Link

- Panasonic

- Amazon (First-Party)

- Broadlink

- Ankuoo

- EDIMAX

- Vesync (Etekcity, Levoit, Cosori)

- Lenovo

- Leviton

- Wipro

- Sariana (Satechi)

- Sonoff (ITEAD)

- Shelly

- Gosund / Nooie

- Eve Systems

- Aeotec

- Sengled

- Wyze Labs

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soaring adoption of voice-assistant ecosystems

- 4.2.2 Falling ASPs of Wi-Fi chipsets

- 4.2.3 Government energy-efficiency mandates for plug-load control

- 4.2.4 Matter 1.3 interoperability push

- 4.2.5 Subsidy programs for senior-care tele-monitoring

- 4.2.6 Rising demand for outdoor weather-proof plugs

- 4.3 Market Restraints

- 4.3.1 Persistent device cybersecurity breaches

- 4.3.2 Fragmented RF spectrum in emerging markets

- 4.3.3 EU WEEE recycling costs hitting margins

- 4.3.4 Inaccurate energy-metering claims triggering recalls

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Force Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Trends on Market

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Technology

- 5.1.1 Wi-Fi

- 5.1.2 Bluetooth

- 5.1.3 Zigbee / Thread

- 5.1.4 Z-Wave

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Others (Hospitality, Healthcare)

- 5.3 By Sales Channel

- 5.3.1 Online

- 5.3.2 Offline

- 5.4 By Plug Form Factor

- 5.4.1 Wall-Plug Adapter

- 5.4.2 In-Wall Outlet

- 5.4.3 Power Strip

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 Turkey

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 TP-Link Technologies

- 6.4.2 Belkin (WeMo)

- 6.4.3 Xiaomi

- 6.4.4 D-Link

- 6.4.5 Panasonic

- 6.4.6 Amazon (First-Party)

- 6.4.7 Broadlink

- 6.4.8 Ankuoo

- 6.4.9 EDIMAX

- 6.4.10 Vesync (Etekcity, Levoit, Cosori)

- 6.4.11 Lenovo

- 6.4.12 Leviton

- 6.4.13 Wipro

- 6.4.14 Sariana (Satechi)

- 6.4.15 Sonoff (ITEAD)

- 6.4.16 Shelly

- 6.4.17 Gosund / Nooie

- 6.4.18 Eve Systems

- 6.4.19 Aeotec

- 6.4.20 Sengled

- 6.4.21 Wyze Labs

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment