PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851193

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851193

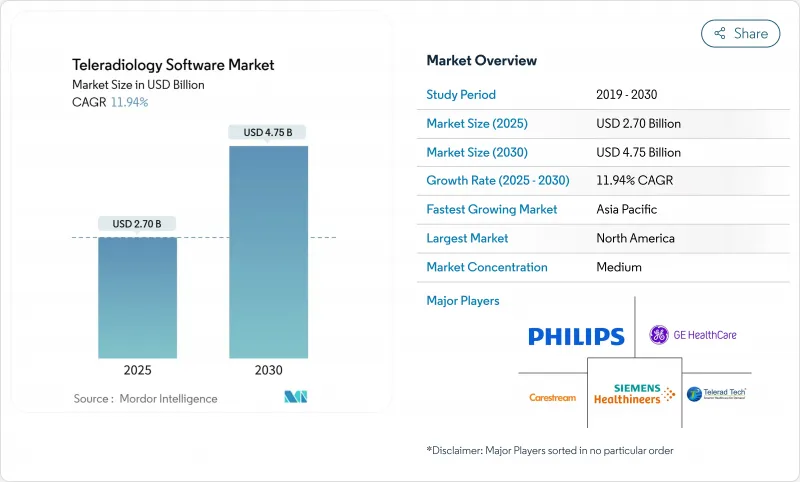

Teleradiology Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Teleradiology Software Market size is estimated at USD 2.70 billion in 2025, and is expected to reach USD 4.75 billion by 2030, at a CAGR of 11.94% during the forecast period (2025-2030).

The teleradiology software market size trajectory rests on three mutually reinforcing forces: a widening global radiologist shortfall, imaging volumes that climb 3-4% a year, and cloud architectures that allow instant scale. Hospitals deploy the platforms to secure 24/7 subspecialist coverage, while diagnostic centers harness them to extend hours without hiring on-site radiologists. Technology vendors are embedding AI triage and structured-report modules, which boost reading productivity by up to 30% and help mitigate burnout. Regulations now formally recognize remote preliminary reads, and growing reimbursement parity is steering budgets toward digital infrastructure. Together, these dynamics sustain double-digit growth while intensifying competition around cloud-native, AI-ready ecosystems.

Global Teleradiology Software Market Trends and Insights

Growing Chronic Disease Burden and Imaging Volume

Medical imaging demand is set to climb another 27% by 2055, amplifying pressure on limited radiology resources. CT studies alone could rise 25.1%, while nuclear medicine and X-ray work keep pace. With 4.2 billion examinations already performed each year, health systems depend on teleradiology to flex reading capacity, distribute subspecialist expertise, and keep turnaround times within quality benchmarks. The ability to route overflow studies across national or even continental networks preserves continuity of care and mitigates appointment backlogs.

Global Radiologist Shortage and Outsourcing Surge

The United States may face a deficit of up to 124,000 physicians by 2034, and radiology posts are among the hardest to fill. The United Kingdom reports a 30% radiologist gap, while attrition sits near 13% annually. Productivity metrics show teleradiology groups processing as many as one-third more studies per reader than conventional onsite teams. As rural and community hospitals struggle to staff night and weekend shifts, outsourcing becomes a structural solution, solidifying demand for software that coordinates multi-site workflows and credentialing.

Stringent Data-Privacy Compliance (HIPAA/GDPR) Costs

Meeting HIPAA encryption rules in the United States and GDPR restrictions in Europe raises deployment expenses, particularly for smaller clinics that lack dedicated security staff. Organizations managing cross-border reads must navigate overlapping consent regulations and incident-reporting duties, often commissioning third-party audits that inflate total cost of ownership. Cybersecurity investments become mandatory as healthcare organizations address increasing cyber threats, with legal implications for clinicians requiring robust incident response plans and encryption protocols.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Cloud PACS / VNA Architectures

- Rise of Telehealth and Remote-Care Trends

- Cross-Border Medico-Legal Liability for AI Preliminary Reads

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PACS remained the anchor technology with 45.32% share in 2024. At the same time, VNA logged a 13.12% CAGR outlook, signaling a pivot toward vendor neutrality and enterprise imaging consolidation. The teleradiology software market size attached to VNA is set to rise sharply as organizations migrate away from siloed archives. Children's Hospital of Philadelphia reported USD 3 million savings in five years after its VNA transition.

RIS and nascent enterprise platforms now integrate over 110 certified AI apps through single interfaces, as shown by CARPL.ai's FDA-cleared hub. Such interoperability compresses report-turnaround times and reduces costly data migrations, giving VNAs tangible economic and clinical advantages.

Cloud installations represented 62.44% of the teleradiology software market in 2024 and are on track for a 12.88% CAGR. Amazon Web Services underpins GE HealthCare's Genesis portfolio, which promises one-click elasticity and AI scalability.

On-premise systems persist in defense and academic centers with bespoke latency or sovereignty mandates. Yet hybrid setups emerge, allowing sensitive studies to remain local while leveraging cloud analytics for population health. This balanced approach reconciles compliance with innovation and keeps demand for multi-tier deployment orchestration strong within the teleradiology software market.

The Teleradiology Software Market Report is Segmented by Solution Type (Radiology Information System (RIS), Picture Archiving & Communication System (PACS) and More), Deployment Mode (Cloud-Based and On-Premise), Imaging Modality Supported (X-Ray, Computed Tomography (CT), and More), End User (Hospitals, and More), and Geography (North America, Europe and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 39.83% share in 2024, buoyed by reimbursable telehealth policies and FDA clearance of more than 1,000 clinical AI tools, 758 of which target radiology. Rural access initiatives channel grants to small hospitals, further propelling the teleradiology software market. Ongoing mergers, such as ONRAD absorbing Direct Radiology, extend independent coverage networks and promote standardized workflow software.

Asia-Pacific registers the quickest 13.64% CAGR, underpinned by India's Ayushman Bharat Digital Mission that issues unique health IDs ready for image exchange. Indonesia's launch of PT. Teleradiologi Center Indonesia widens subspecialist access, while Australia's National Digital Health Strategy funds secure image-sharing grids. Combined, these initiatives lower entry barriers for cloud PACS vendors and local startups.

Europe shows steady adoption, aided by the EUR 4 billion Hospital Future Act that scored German hospitals at just 33.3 on a 100-point digitization index, spotlighting investment gaps. The EU Recovery and Resilience Facility stipulates that a fifth of spending targets digital infrastructure, catalyzing cross-border image-sharing pilots and harmonized medico-legal frameworks. Middle East, Africa, and South America remain nascent, yet public cloud rollouts and urban cancer-center build-outs are laying foundational demand for the teleradiology software market.

- GE Healthcare

- Koninklijke Philips

- Siemens Healthineers

- Sectra

- Change Healthcare

- Carestream Health

- Agfa-Gevaert

- FUJIFILM

- Visage Imaging

- Telerad Tech

- Comarch

- Medsynaptic

- Perfect Imaging

- Imagebytes Pvt Ltd

- Morton & Partners Radiologists

- Radical Imaging

- ONRAD Inc.

- Everrtech

- TeleSpecialists LLC

- Virtual Radiologic (vRad)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Chronic Disease Burden and Imaging Volume

- 4.2.2 Global Radiologist Shortage and Outsourcing Surge

- 4.2.3 Rapid Adoption of Cloud PACS / VNA Architectures

- 4.2.4 Rise of Telehealth and Remote Care Trends

- 4.2.5 Stronger Regulatory and Infrastructure Support

- 4.2.6 Hardware and Edge AI Integration at Point-of-Care

- 4.3 Market Restraints

- 4.3.1 Stringent Data-Privacy Compliance (HIPAA/GDPR) Costs

- 4.3.2 High Integration and Change-Management Costs for Small Sites

- 4.3.3 Cloud-Vendor Lock-In Via High Egress Fees

- 4.3.4 Cross-Border Medico-Legal Liability for AI Preliminary Reads

- 4.4 Technological Outlook

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Solution Type

- 5.1.1 Radiology Information System (RIS)

- 5.1.2 Picture Archiving & Communication System (PACS)

- 5.1.3 Vendor-Neutral Archive (VNA)

- 5.1.4 Other Solution Types

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.3 By Imaging Modality Supported

- 5.3.1 X-ray

- 5.3.2 Computed Tomography (CT)

- 5.3.3 Magnetic Resonance Imaging (MRI)

- 5.3.4 Ultrasound

- 5.3.5 Nuclear Imaging (PET/SPECT)

- 5.3.6 Mammography

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Diagnostic Imaging Centers

- 5.4.3 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 GE HealthCare

- 6.3.2 Koninklijke Philips N.V.

- 6.3.3 Siemens Healthineers AG

- 6.3.4 Sectra AB

- 6.3.5 Change Healthcare

- 6.3.6 Carestream Health

- 6.3.7 Agfa-Gevaert NV

- 6.3.8 Fujifilm Healthcare

- 6.3.9 Visage Imaging

- 6.3.10 Telerad Tech

- 6.3.11 Comarch SA

- 6.3.12 Medsynaptic Pvt Ltd

- 6.3.13 Perfect Imaging LLC

- 6.3.14 Imagebytes Pvt Ltd

- 6.3.15 Morton & Partners Radiologists

- 6.3.16 Radical Imaging LLC

- 6.3.17 ONRAD Inc.

- 6.3.18 Everrtech

- 6.3.19 TeleSpecialists LLC

- 6.3.20 Virtual Radiologic (vRad)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment