PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851215

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851215

Radiation Hardened Electronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

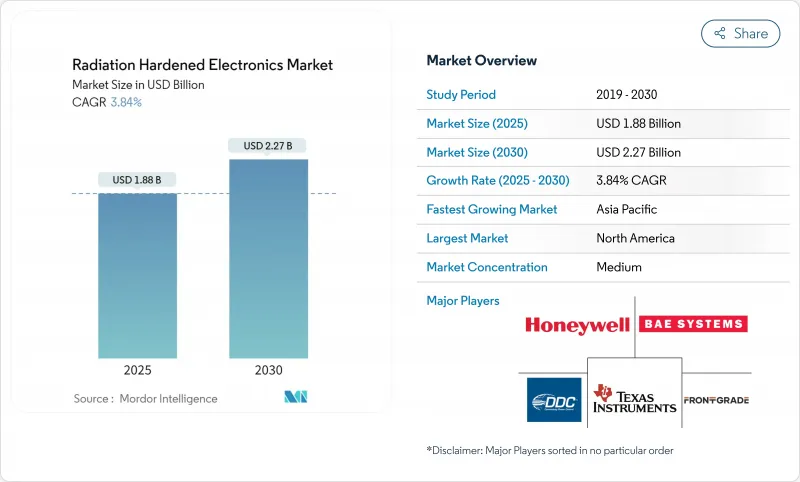

The radiation hardened electronics market size stands at USD 1.88 billion in 2025 and is forecast to climb to USD 2.27 billion by 2030, reflecting a 3.84% CAGR.

Demand continues to bifurcate between ultra-high-reliability parts for deep-space and strategic defense missions and cost-optimized, radiation-tolerant devices for proliferated low-Earth-orbit (LEO) constellations and stratospheric platforms. Geopolitical drivers-most notably NATO nuclear-modernization programs, renewed nuclear-power construction in Asia, and the ramp-up of small-satellite launches-are reshaping product road maps and qualification priorities. Commercial foundries are partnering with defense primes to stretch mature silicon nodes while integrating gallium nitride (GaN) and silicon carbide (SiC) for next-generation power systems. Supply-chain bottlenecks in <=90 nm radiation-hard-by-process (RHBP) capacity, together with evolving export-control regimes, spur a parallel push toward radiation-hard-by-design (RHBD) methodologies that shorten development cycles and lower cost.

Global Radiation Hardened Electronics Market Trends and Insights

Surge in LEO and Deep-Space Satellite Constellations

LEO mega-constellations are driving a new stratification of performance targets: 30-50 krad(Si) tolerant parts for mass-manufactured satellites versus >=100 krad(Si) parts for geostationary and deep-space assets. Device vendors now run parallel product lines, such as miniaturized GaN power stages that blend higher integration with lower shielding mass.Smaller spacecraft footprints intensify the need for size-, weight-, and power-optimized (SWaP) solutions while preserving single-event-effect immunity. Concurrently, on-orbit reconfigurability via radiation-tolerant FPGAs allows operators to refresh mission software without physical access, extending constellation life cycles. Strong backlog for lunar logistics and Mars relay satellites further cements deep-space demand.

Modernisation of Strategic and Tactical Defense Electronics in NATO Region

The United States and European defense ministries are channeling funds into trusted domestic microelectronics to shield critical systems from high-altitude electromagnetic pulse scenarios. The FY 2025 United States DoD budget allocates USD 24.884 million to accelerate radiation-hardened RF and opto-electronic prototypes. Test infrastructure follows suit: Naval Surface Warfare Center Crane's Short Pulse Gamma facility underpins a USD 100 million modernization drive, enabling concurrent nuclear-modernization programs.

High Design-for-Reliability Cost & Long Qualification Cycles

Developing radiation-hardened ASICs costs 5-10 times more than commercial equivalents. The Strategic Radiation-Hardened Electronics Council forecasts SEE test-beam oversubscription of up to 6,000 hours annually by 2025, a gap that stretches qualification queues. Space operators therefore pilot streamlined COTS-based selection processes to cut lead times, balancing life-orbit risk against launch cadence.

Other drivers and restraints analyzed in the detailed report include:

- Nuclear-New-Build Momentum in Asia and Middle-East

- High-Altitude UAV and Supersonic Aircraft Electronics Resilience Needs

- Restricted Foundry Capacity for RHBP Nodes <= 90 nm

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The space segment accounted for 46.3% of the radiation hardened electronics market in 2024, anchoring specification baselines for total-ionizing-dose and single-event-effect immunity. Operators moving from bespoke GEO spacecraft to proliferated LEO constellations now trade some resilience for lower cost and rapid refresh, catalyzing hybrid product lines that mate 30 krad(Si) design targets with lower shielding mass. NASA's Artemis lunar program and commercial cislunar logistics underpin steady demand for >=100 krad(Si) devices that survive deep-space radiation belts.

High-Altitude UAV/HAPS platforms, forecast to grow at 4.2% to 2030, extend aerospace electronics into a quasi-space radiation spectrum. Designers leverage RHBD FPGAs for adaptive payloads and use wide-band-gap power stages to meet tight energy budgets. The radiation hardened electronics market size for this sub-segment is projected to broaden as 6G network backhaul trials migrate from prototypes to operational fleets.

Integrated circuits held 31.5% radiation hardened electronics market share in 2024, with mixed-signal ASICs consolidating multiple analog front ends and power-management functions onto a single die to trim board-level mass. Supply risks around SEE-capable beam time are prompting chip houses to qualify identical IP blocks simultaneously on two foundry flows, bolstering continuity plans.

Field-programmable gate arrays represent the fastest 4.6% CAGR as satellite operators prize in-orbit reconfiguration. The latest Kintex UltraScale XQRKU060 class blends 2 million logic cells with on-chip scrub controllers that mitigate configuration memory upsets. The radiation hardened electronics market sees FPGAs bridging the gap between fixed-function silicon and software-only fault mitigation, carving share from discrete logic.

The Radiation Hardened Electronics Market Report is Segmented by End-User (Space, and More), Component (Discrete Semiconductors, and More), Product Type (Analog and Mixed-Signal, Digital Logic, and More), Manufacturing Technique (Rad-Hard-By-Design (RHBD), and More), Semiconductor Material (Silicon, and More), Radiation Type (Total Ionizing Dose (TID), and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 39.8% of 2024 sales, buoyed by sustained defense budgets and NASA exploration initiatives. Trusted domestic foundries, plus dedicated beam-line capacity at facilities such as NSWC Crane, shorten certification loops and anchor many prime-contractor supply chains. Space commerce diversification into lunar communications and asteroid-prospecting missions should further support regional demand.

Asia Pacific posts the quickest 4.1% CAGR to 2030 as China, India, and South Korea scale rocket fleets and commission new-build nuclear reactors. Government space agencies co-invest with local universities in RHBD design centers to decrease reliance on imported parts. Emerging commercial launch providers likewise adopt radiation-tolerant FPGAs to meet agile-satellite business models.

Europe combines ESA's large mission pipeline with strong nuclear-plant refurbishment schedules. Neuromorphic on-board processing programs such as the NEUROSPACE initiative underscore the region's pivot toward ultra-low-power compute. Middle-East space offices in the UAE and Saudi Arabia pursue Mars probes and Earth-observation clusters, opening niche opportunities for localized assembly and test. South America remains nascent but benefits from Brazilian and Argentine small-satellite projects seeking home-grown avionics.

- Honeywell International Inc.

- BAE Systems plc

- CAES (Cobham Advanced Electronic Solutions)

- Texas Instruments Inc.

- STMicroelectronics N.V.

- Microchip Technology Inc.

- Infineon Technologies AG

- Frontgrade Technologies

- Teledyne e2v Semiconductors

- Xilinx (RT Series, AMD)

- Renesas Electronics Corp.

- Solid State Devices Inc.

- Micropac Industries Inc.

- Everspin Technologies Inc.

- Vorago Technologies

- Analog Devices HiRel

- International Rectifier HiRel (Infineon)

- Maxwell Technologies (ES-capacitors)

- 3D Plus

- GSI Technology, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in LEO and Deep-Space Satellite Constellations

- 4.2.2 Modernisation of Strategic and Tactical Defence Electronics in NATO Region

- 4.2.3 Nuclear-New-Build Momentum in Asia and Middle-East

- 4.2.4 High-Altitude UAV and Supersonic Aircraft Electronics Resilience Needs

- 4.2.5 Mandated Radiation-Tolerance Standards in Medical Imaging (U-S FDA, EU MDR)

- 4.2.6 Rapid Adoption of SiC/GaN Rad-Hard Power Devices in Spacecraft PPU

- 4.3 Market Restraints

- 4.3.1 High Design-for-Reliability Cost and Long Qualification Cycles

- 4.3.2 Restricted Foundry capacity for RHBP (Rad-Hard-by-Process) Nodes ? 90 nm

- 4.3.3 Performance Trade-offs vs COTS Chips (Speed, Density)

- 4.3.4 ITAR/Export-Control Supply-Chain Bottlenecks

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By End-User

- 5.1.1 Space

- 5.1.2 Aerospace and Defense (Air, Land, Naval)

- 5.1.3 Nuclear Power Generation and Fuel Cycle

- 5.1.4 Medical Imaging and Radiotherapy

- 5.1.5 High-Altitude UAV/HAPS Platforms

- 5.1.6 Industrial Particle Accelerators and Research Labs

- 5.2 By Component

- 5.2.1 Discrete Semiconductors

- 5.2.2 Sensors (Optical, Image, Environmental)

- 5.2.3 Integrated Circuits (ASIC, SoC)

- 5.2.4 Microcontrollers and Microprocessors

- 5.2.5 Memory (SRAM, MRAM, FRAM, EEPROM)

- 5.2.6 Field-Programmable Gate Arrays (FPGA)

- 5.2.7 Power Management ICs

- 5.3 By Product Type

- 5.3.1 Analog and Mixed-Signal

- 5.3.2 Digital Logic

- 5.3.3 Power and Linear

- 5.3.4 Processors and Controllers

- 5.4 By Manufacturing Technique

- 5.4.1 Rad-Hard-by-Design (RHBD)

- 5.4.2 Rad-Hard-by-Process (RHBP)

- 5.4.3 Rad-Hard-by-Software/Firmware Mitigation

- 5.5 By Semiconductor Material

- 5.5.1 Silicon

- 5.5.2 Silicon Carbide (SiC)

- 5.5.3 Gallium Nitride (GaN)

- 5.5.4 Others (InP, GaAs)

- 5.6 By Radiation Type

- 5.6.1 Total Ionizing Dose (TID)

- 5.6.2 Single-Event Effects (SEE)

- 5.6.3 Displacement Damage Dose (DDD)

- 5.6.4 Neutron and Proton Fluence

- 5.7 By Geography

- 5.7.1 North America

- 5.7.2 Europe

- 5.7.3 Asia-Pacific

- 5.7.4 South America

- 5.7.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JV, Funding, Tech-Roadmaps)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-Level Overview, Market-Level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Honeywell International Inc.

- 6.4.2 BAE Systems plc

- 6.4.3 CAES (Cobham Advanced Electronic Solutions)

- 6.4.4 Texas Instruments Inc.

- 6.4.5 STMicroelectronics N.V.

- 6.4.6 Microchip Technology Inc.

- 6.4.7 Infineon Technologies AG

- 6.4.8 Frontgrade Technologies

- 6.4.9 Teledyne e2v Semiconductors

- 6.4.10 Xilinx (RT Series, AMD)

- 6.4.11 Renesas Electronics Corp.

- 6.4.12 Solid State Devices Inc.

- 6.4.13 Micropac Industries Inc.

- 6.4.14 Everspin Technologies Inc.

- 6.4.15 Vorago Technologies

- 6.4.16 Analog Devices HiRel

- 6.4.17 International Rectifier HiRel (Infineon)

- 6.4.18 Maxwell Technologies (ES-capacitors)

- 6.4.19 3D Plus

- 6.4.20 GSI Technology, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Emerging Opportunities in Modular Small-Sat Avionics

- 7.3 On-Orbit Servicing and Manufacturing Electronics

- 7.4 Radiation-Tolerant AI Accelerators for Edge-Space Computing

- 7.5 Additive Manufacturing of Rad-Hard Packages