PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851225

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851225

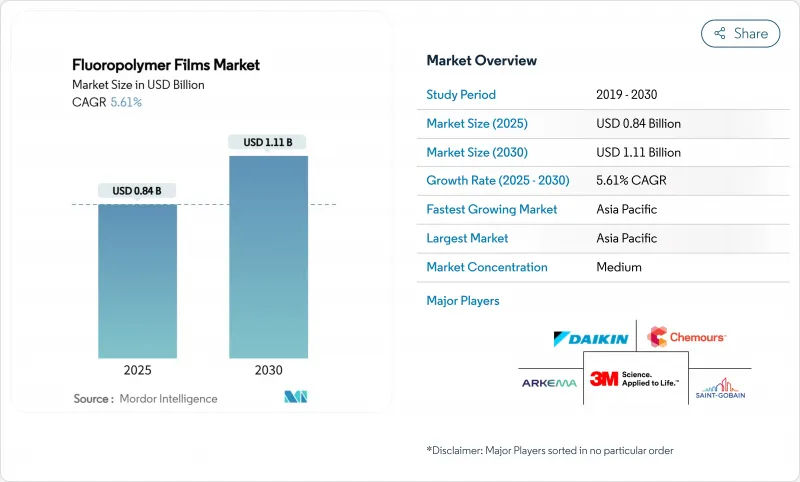

Fluoropolymer Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Fluoropolymer Films Market size is estimated at USD 0.84 billion in 2025, and is expected to reach USD 1.11 billion by 2030, at a CAGR of 5.61% during the forecast period (2025-2030).

This growth outlook underscores how irreplaceable performance attributes, notably chemical inertness, low surface energy, and wide-temperature stability, continue to outweigh mounting regulatory pressures on per- and polyfluoroalkyl substances (PFAS). Rapid photovoltaic (PV) build-out, electric-vehicle (EV) light-weighting, and semiconductor contamination control remain the three most influential demand engines. Incumbent producers are widening product portfolios for mission-critical applications rather than chasing volume alone, while downstream customers signal rising willingness to pay for durability and safety assurances. Asia Pacific retains structural cost advantages and end-use proximity, Northern American buyers prioritize high-purity and traceability, and European policy makers drive innovation in PFAS-compliant chemistries. Together, these forces point to a steady, rather than exponential, expansion path for the fluoropolymer films market over the next five years.

Global Fluoropolymer Films Market Trends and Insights

Accelerating Demand for PV Solar Front-Sheet and Back-Sheet Films

Flexible PV installations rely on transparent and weather-resistant fluoropolymer laminates to displace heavier glass. Lower water-vapor-transmission rates help perovskite modules retain 84% efficiency after 2,000 hours of damp-heat testing, extending module warranties to 25 years. Asia Pacific's consumption share mirrors its photovoltaic assembly dominance, while U.S. community-solar policies reinforce demand peaks. Consequently, barrier films remain the largest application slice of the fluoropolymer films market.

Rising Pharmaceutical and Medical Packaging Adoption

Biologics and personalized therapies require stringent moisture and chemical barriers. Chemours confirms that PTFE and PVDF grades remain essential in pre-filled syringes and micro-catheters because of their low extractables and biocompatibility. U.S. FDA guidance on container-closure integrity pushes drug makers to specify high-purity fluoropolymer liners to protect sensitive actives. Matching trends in EU Annex 1 revisions strengthen demand for medical-grade films.

Global PFAS Regulatory Tightening

The U.S. EPA has barred production of 329 PFAS without agency review and designated PFOA and PFOS as hazardous substances. Minnesota and California ban PFAS in select consumer products from January 2025, while an EU REACH proposal seeks to restrict more than 10,000 substances above threshold concentrations. Compliance costs and potential substitution risks collectively shave 1.4 percentage points off the forecast CAGR for the fluoropolymer films market.

Other drivers and restraints analyzed in the detailed report include:

- EV-Led Uptake of Release Films for Lightweight Composites

- Fluoropolymer Proton-Exchange Membranes in Green-Hydrogen Electrolysers

- Volatile Feedstock Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polytetrafluoroethylene (PTFE) held a 46.55% share. High melt viscosity yet unmatched chemical inertness anchors its use in semiconductor fabrication chambers, gasket sheets, and high-frequency cables. Continued fab expansions in Taiwan and the United States support demand resilience. The material's low friction coefficient also keeps PTFE relevant in surgical device liners despite looming regulatory review.

Fluorinated Ethylene-Propylene's (FEP) 6.09% CAGR positions it as the fastest-growing polymer family through 2030. Lower melt temperature enables melt-extruded tubing, color-matchable sheets, and increasingly 3-D printed filaments for consumer electronics housings. Arkema's FluorX filament release illustrates how FEP addresses processing constraints that limit PTFE uptake in additive manufacturing. Users value optical clarity combined with 200 °C continuous-use temperature, broadening adoption in flexible printed circuits.

The Fluoropolymer Films Report is Segmented by Type (Polytetrafluoroethylene (PTFE), Polyvinylidene Fluoride (PVDF), and More), Application (Barrier Films, Release Films, Microporous Films, and Security Films), End-User Industry (Automotive/Aerospace/Defense, Construction, Packaging, Industrial, Electronics/Semiconductor, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia Pacific generated 48.62% of global sales in 2024, with the fluoropolymer films market size expanding at a region-leading 6.20% CAGR. China's integrated PV supply chain consumes vast volumes of PVF backsheets and ETFE frontsheets, while government incentives accelerate rooftop-solar retrofits. India's electronics manufacturing scheme promotes domestic sourcing of high-purity PTFE tapes, elevating baseline demand. Japan's automotive platforms shift to 800-V architectures, favouring PEEK and PTFE dielectric films for improved thermal management.

North America benefits from strong semiconductor capital expenditure and medical-device innovation. Chip fabs under the U.S. CHIPS Act upgrade clean-room standards, driving PTFE and FEP consumables. EV platforms from Michigan to Georgia require composite release films for body-in-white panels.

Europe balances regulatory stringency with climate-policy pull. Green-hydrogen electrolyser pilots in Germany and Spain incorporate fluoropolymer PEMs. Automotive OEMs in Germany and France integrate ETFE roof skins for weight savings. Yet proposed EU-wide PFAS restrictions inject uncertainty, prompting producers to invest in closed-loop recovery and waste-gas abatement. Such measures sustain supply, albeit at higher compliance cost.

- 3M

- AGC Inc.

- Arkema

- Daikin Industries Ltd.

- DuPont

- Fluortek AB

- Honeywell International Inc.

- Jiangsu Meilan Chemical Co. Ltd

- Nitto Denko Corporation

- Saint-Gobain

- Solvay

- The Chemours Company

- TORAY INDUSTRIES, INC.

- Zeus Industrial Products Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Demand for PV Solar Front-Sheet and Back-Sheet Films

- 4.2.2 Rising Pharmaceutical and Medical Packaging Adoption

- 4.2.3 EV-Led Uptake of Release Films for Lightweight Composites

- 4.2.4 Fluoropolymer Proton-Exchange Membranes in Green-Hydrogen Electrolysers

- 4.2.5 Microporous PTFE Separators for Solid-State E-Aviation Batteries

- 4.3 Market Restraints

- 4.3.1 Global PFAS Regulatory Tightening

- 4.3.2 Volatile Feedstock Costs

- 4.3.3 Rise of Fluorine-Free High-Barrier Multilayer Films

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Polytetrafluoroethylene (PTFE)

- 5.1.2 Polyvinylidene Fluoride (PVDF)

- 5.1.3 Fluorinated Ethylene-Propylene (FEP)

- 5.1.4 Ethylene Tetrafluoroethylene (ETFE)

- 5.1.5 Perfluoroalkoxy Alkane (PFA)

- 5.1.6 Polyvinyl Fluoride (PVF)

- 5.1.7 Others

- 5.2 By Application

- 5.2.1 Barrier Films

- 5.2.2 Release Films

- 5.2.3 Microporous Films

- 5.2.4 Security Films

- 5.3 By End-User Industry

- 5.3.1 Automotive, Aerospace and Defense

- 5.3.2 Construction

- 5.3.3 Packaging

- 5.3.4 Industrial

- 5.3.5 Electronics and Semiconductor

- 5.3.6 Others (Textiles, Graphics)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 AGC Inc.

- 6.4.3 Arkema

- 6.4.4 Daikin Industries Ltd.

- 6.4.5 DuPont

- 6.4.6 Fluortek AB

- 6.4.7 Honeywell International Inc.

- 6.4.8 Jiangsu Meilan Chemical Co. Ltd

- 6.4.9 Nitto Denko Corporation

- 6.4.10 Saint-Gobain

- 6.4.11 Solvay

- 6.4.12 The Chemours Company

- 6.4.13 TORAY INDUSTRIES, INC.

- 6.4.14 Zeus Industrial Products Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment