PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851230

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851230

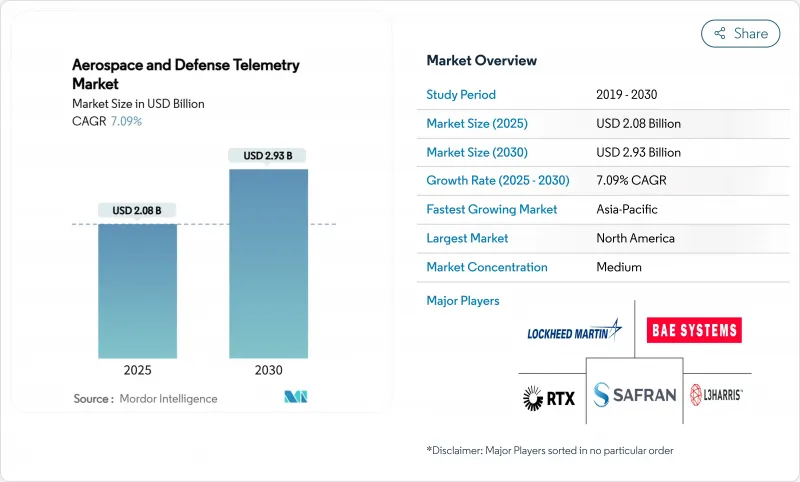

Aerospace And Defense Telemetry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The aerospace and defense telemetry market size is estimated at USD 2.08 billion in 2025, and is expected to reach USD 2.93 billion by 2030, reflecting a CAGR of 7.09% during the forecast period.

Demand growth reflects the transition from legacy data pipes to edge-enabled telemetry architectures that process mission data in real time and compress non-essential traffic before transmission. Hypersonic weapon programs, proliferating satellite constellations, and onboard artificial intelligence collectively reshape telemetry design rules. At the same time, NATO and Indo-Pacific modernization plans elevate bandwidth requirements across airborne ISR, naval, and missile platforms. Radio Frequency links retain scale advantages, yet laser and optical systems secure rapid adoption where spectrum congestion threatens mission continuity. Ongoing integration of space-based edge AI allows satellites to triage data on-orbit, trimming ground-station backlogs and improving decision speed. Consolidation activity-exemplified by BAE Systems' USD 5.5 billion purchase of Ball Aerospace-shows how incumbents bolt on specialized telemetry assets to retain strategic dominance.

Global Aerospace And Defense Telemetry Market Trends and Insights

Expansion of Hypersonic and Reusable Launch Vehicle Programs

Hypersonic flight places unprecedented thermal and plasma-induced stress on data links, forcing designers to develop telemetry modules that sustain lock at velocities above Mach 5. Stratolaunch's Talon-A2 test flights in 2024 proved the need for shock-hardened antennas that survive multiple sorties while delivering health-monitoring data at kilohertz refresh rates. Reusability compounds the engineering challenge because avionics must tolerate repeated heat-cycle loading without drifts in calibration. L3Harris has embedded multi-band transmitters inside its hypersonic glide vehicles to stream trajectory and seeker-status packets that feed real-time fire-control algorithms. The cumulative effect elevates the Aerospace and Defense Telemetry market as defense ministries allocate dedicated budgets for survivable flight-test instrumentation and production-grade weapon telemetry.

Proliferation of Small Satellite Constellations Requiring High-Bandwidth Telemetry

Starlink's deployment of more than 10,000 laser communication terminals has set the reference architecture for low-earth-orbit mesh networks that shuttle traffic laterally before downlink. Smaller operators emulate the approach, driving sustained demand for optical terminals and software-defined radios that negotiate bandwidth dynamically across thousands of nodes. The Aerospace and Defense Telemetry market benefits because military planners value inter-satellite links for resilient command-and-control when adversaries jam ground gateways. Dynamic waveform agility allows constellation managers to throttle bandwidth toward urgent sensor data while compressing housekeeping traffic, honing resource utilization, and protecting margins.

Spectrum Congestion and International Coordination Delays Impacting Bandwidth Access

The ITU's Master International Frequency Register faces mounting backlogs as operators file for thousands of constellations overlapping Ku-, Ka-, and V-band allocations. Defense platforms seeking protected bands must now wait several months for clearance, impeding program schedules. In national jurisdictions like the United States, FCC auctions repurpose legacy C-band for 5G, squeezing telemetry users into narrower slices. Cross-border coalition exercises suffer when frequency conflicts force last-minute re-planning, reducing training value. Adaptive spectrum-sharing radios show promise, yet regulators have not fully codified real-time coordination rules, prolonging uncertainty for the Aerospace and Defense Telemetry market.

Other drivers and restraints analyzed in the detailed report include:

- Modernization of Airborne ISR Platforms Across Defense Alliances

- Emergence of Space-Based Edge AI for Real-Time Data Processing

- Size, Weight, and Power (SWaP) Limitations in Small UAV Platforms Constrain Telemetry Integration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Laser/optical links recorded the strongest expansion, advancing at a 9.23% CAGR between 2025 and 2030. Adoption surged after the Space Development Agency published its Optical Communication Terminal Standard v4.0.0, giving primes a clear compliance roadmap. Compared with microwave systems, optical beams deliver 10 to 100-fold bandwidth with tighter spatial confinement that curtails interception risk. In conjunction with adaptive beam-steering mirrors, satellites now switch companions in microseconds, supporting mesh routing no longer bottlenecked by ground relays.

Radio Frequency architectures retained 52.90% revenue in 2024, underscoring the deep installed base and all-weather robustness that militaries trust for command-critical tasks. Spectrum pressure and growing anti-spoofing demands push integrators to blend the two modalities, launching hybrid terminals that can hop between Ka-band and optical carrier. This duality sustains Radio Frequency procurement while infusing new revenue into the aerospace and defense telemetry market. The Starlink rollout creates double-digit demand for optical terminal components, positioning laser equipment suppliers for sustained backlog growth.

Software and data analytics platforms post the fastest 8.56% CAGR over 2025-2030 as operators shift from raw packet storage to predictive insight generation. Integrated dashboards now fuse telemetry, logistics, and environmental feeds to produce maintenance recommendations minutes after flight termination. For instance, Boeing's Condition-Based Smart Maintenance suite blends engine vibration spectra with flight regime tags to flag parts approaching fatigue thresholds.

Transmitters and sensors remained the largest slice at 26.54% in 2024 because every node-a hypersonic vehicle, a nanosatellite, or a UAV-needs physical transducers and power-amplifier chains. Continuous miniaturization compresses these elements into chip-scale packages, freeing space for edge processors. Improved component yields and declining ASIC mask costs lower entry barriers, attracting new suppliers into the Aerospace and Defense Telemetry market and fueling price competition that accelerates volume adoption.

The Aerospace and Defense Telemetry Market Report is Segmented by Communication Technology (Radio Frequency, Satellite, and More), Component (Transmitters and Sensors, Signal Processing Units, and More), Platform (Aircraft, Spacecraft and Launch Vehicles, and More), End User (Aerospace and Defense), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained the largest 36.14% share in 2024 as the US Department of Defense contracts for hypersonic glide vehicles and next-generation ISR platforms kept domestic lines busy. Prime contractors bundle telemetry R&D with full-system bids, keeping value onshore and sustaining robust engineering pipelines. Strong venture-capital appetite for space start-ups further cements regional leadership.

Asia-Pacific posts the most rapid 9.01% CAGR through 2030. China scales factory output of small satellite buses that ship with plug-and-play optical terminals, while India's reusable launch ambitions drive consistent telemetry component requisitions for thermal-cycle testing. Japan channels robotics expertise into miniaturized lunar and asteroid probes' transceivers, turning regional suppliers into global price setters for ultra-compact hardware.

Europe pursues autonomous and sustainable air-traffic goals under SESAR 3.0, prompting local integrators to adopt cyber-resilient software-defined radios inside crewed and uncrewed airframes. The forthcoming EU Space Act, scheduled for late-2025 implementation, will mandate compliance logs for telemetry encryption algorithms operating in EU orbital slots. This new rulebook could marginally slow procurement, yet ultimately harmonizes standards, enlarging addressable demand for certified vendors within the aerospace and defense telemetry market.

- BAE Systems plc

- Lockheed Martin Corporation

- L3Harris Technologies, Inc.

- Safran SA

- Honeywell International Inc.

- Thales Group

- RTX Corporation

- Kongsberg Gruppen ASA

- Curtiss-Wright Corporation

- Leonardo S.p.A

- AstroNova Inc.

- Orbit Communications Systems Ltd.

- Kratos Defense & Security Solutions, Inc.

- Teledyne Technologies Incorporated

- Viasat Inc.

- General Dynamics Mission Systems (General Dynamics Corporation)

- Rohde & Schwarz GmbH & Co KG

- Sierra Nevada Company, LLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of hypersonic and reusable launch vehicle programs

- 4.2.2 Proliferation of small satellite constellations requiring high-bandwidth telemetry

- 4.2.3 Modernization of airborne ISR platforms across defense alliances

- 4.2.4 Emergence of space-based edge AI for real-time data processing

- 4.2.5 Increased adoption of commercial software-defined radios in defense telemetry

- 4.2.6 Growing use of passive telemetry for condition-based maintenance

- 4.3 Market Restraints

- 4.3.1 Spectrum congestion and international coordination delays impacting bandwidth access

- 4.3.2 Size, weight, and power (SWaP) limitations in small UAV platforms constrain telemetry integration

- 4.3.3 Export controls and cyber-sovereignty clauses restricting cross-border technology transfer

- 4.3.4 Rising satellite launch insurance costs limiting available budgets for telemetry systems

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Communication Technology

- 5.1.1 Radio Frequency

- 5.1.2 Satellite

- 5.1.3 Laser/Optical

- 5.1.4 Ethernet/Fiber-Optic

- 5.2 By Component

- 5.2.1 Transmitters and Sensors

- 5.2.2 Antennas and Modulators

- 5.2.3 Software and Data Analytics Platforms

- 5.2.4 Signal Processing Units

- 5.2.5 Ground Receiving Equipment

- 5.3 By Platform

- 5.3.1 Aircraft

- 5.3.2 Spacecraft and Launch Vehicles

- 5.3.3 Unmanned Aerial Vehicles (UAVs)

- 5.3.4 Missiles and Projectiles

- 5.3.5 Marine Vessels

- 5.3.6 Ground Stations

- 5.4 By End User

- 5.4.1 Aerospace

- 5.4.2 Defense

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Paific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BAE Systems plc

- 6.4.2 Lockheed Martin Corporation

- 6.4.3 L3Harris Technologies, Inc.

- 6.4.4 Safran SA

- 6.4.5 Honeywell International Inc.

- 6.4.6 Thales Group

- 6.4.7 RTX Corporation

- 6.4.8 Kongsberg Gruppen ASA

- 6.4.9 Curtiss-Wright Corporation

- 6.4.10 Leonardo S.p.A

- 6.4.11 AstroNova Inc.

- 6.4.12 Orbit Communications Systems Ltd.

- 6.4.13 Kratos Defense & Security Solutions, Inc.

- 6.4.14 Teledyne Technologies Incorporated

- 6.4.15 Viasat Inc.

- 6.4.16 General Dynamics Mission Systems (General Dynamics Corporation)

- 6.4.17 Rohde & Schwarz GmbH & Co KG

- 6.4.18 Sierra Nevada Company, LLC.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment