PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851249

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851249

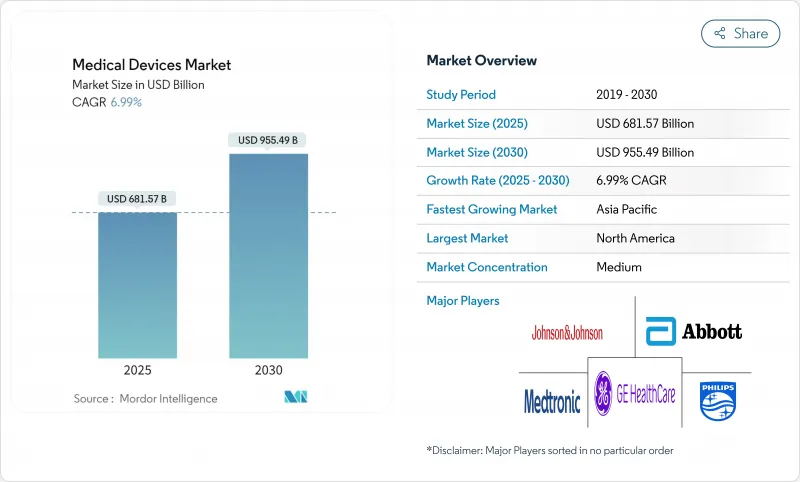

Medical Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The medical devices market currently values at USD 681.57 billion in 2025 and is forecast to reach USD 955.49 billion by 2030, advancing at a 6.99% CAGR.

Steady demand stems from growing chronic disease prevalence, rapid adoption of artificial intelligence in diagnostics and therapeutics, and regulatory reforms that simplify global product approvals while elevating safety standards. Manufacturers are prioritizing connected, software-driven solutions that improve real-time decision support, supported by 5G infrastructure that reduces latency for critical procedures. Cybersecurity obligations introduced by the Food and Drug Administration (FDA) in 2025 are accelerating investment in secure-by-design architectures, and quality system harmonization effective 2026 is lowering duplication costs for multinational launches. Capital continues to flow toward neurology, remote monitoring, augmented reality training tools and ambulatory care technologies, reflecting an industry shift away from hospital-centric delivery models toward decentralized, data-rich ecosystems.

Global Medical Devices Market Trends and Insights

Aging Population and Chronic Disease Prevalence

Adults aged 65 or older will form 22% of the world's population by 2030, with 85% experiencing at least one chronic condition, ensuring sustained demand for diagnostics, monitoring and therapeutic devices. Global chronic-disease-related economic burden is projected at USD 47 trillion through 2030, prompting payers to favor prevention and remote monitoring. Neurology benefits as Parkinson's disease incidence may double by 2040, catalyzing investment in adaptive deep-brain stimulation and brain-computer interfaces. Wearables for fall detection and medication adherence open new high-volume categories, while value-based reimbursement models reward devices that demonstrate outcome improvement.

Technological Advancements in AI and Digital Health

The FDA cleared 69 AI-enabled devices in 2024, a 40% year-over-year increase, spanning imaging, surgical robotics and decision support. Machine-learning algorithms now tune therapy parameters in real time; for example, cardiac ablation systems dynamically adjust energy delivery using tissue impedance data and shorten procedure times by 30%. 5G connectivity enables sub-millisecond latency for remote interventions, while digital therapeutics merge software with hardware to personalize chronic-care regimens. These capabilities are enlarging the addressable medical devices market by embedding intelligence into legacy form factor

Supply Chain Disruptions and Material Shortages

Semiconductor scarcity extended medical component lead times to 52 weeks for 78% of OEMs in 2024 mddionline.com. Reliance on regionally concentrated suppliers of PTFE and rare-earth metals exposes manufacturers to geopolitical shocks. Medtronic cut its vendor base 40% and consolidated distribution hubs to reinforce resilience, yet near-shoring and dual-sourcing inflate costs 15-20% and require multi-year rollouts. FDA shortage lists that include pediatric tracheostomy tubes underscore direct patient-care risks, forcing contingency redesigns and strategic safety-stock programs.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Modernization and Harmonization

- Healthcare Infrastructure Development in Emerging Markets

- Cybersecurity Threats and Data Privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional electro-mechanical and disposable products delivered 56.47% of 2024 revenue, cementing their role in critical care due to proven reliability, established workflows and cost efficiency. Their breadth, from basic syringes to ICU ventilators, makes them indispensable to both emerging and high-income systems. However, augmented and virtual reality devices are accelerating at a 7.78% CAGR as surgeons adopt immersive visualization tools for complex procedures. FDA authorizations for AR-guided navigation systems provide clinical evidence of shorter operating times and fewer complications.

Remote-monitoring wearables now support 50 million U.S. users, reflecting a tripling in program enrollments since 2021. Robotic surgery platforms such as Johnson & Johnson's Velys Spine leverage AI to refine trajectory planning, while 3D-printed implants move from prototypes to permanent musculoskeletal applications following the first laser-printed total knee clearance in 2024. Telehealth peripherals integrate seamlessly with cloud dashboards, enabling clinicians to oversee multiple vitals remotely, a capability magnified as mHealth platforms embed diagnostic algorithms. Nanotechnology remains early-stage but draws R&D funding for targeted drug delivery and high-resolution in-vivo sensors.

The Medical Devices Market Report is Segmented by Technology Platform (Conventional Electro-Mechanical & Disposable Devices, Wearable & Remote Monitoring, and More), Therapeutic Application (Cardiology, Orthopedics, Neurology, and More), End User (Hospitals, Clinics, Ambulatory Surgical Centers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains 40.23% of 2024 revenue due to advanced reimbursement, integrated research campuses and proximity to regulators. Strong venture funding and clinician buy-in accelerate first-in-class releases, ensuring early adoption of robotics, AI imaging and leadless cardiac devices. Nevertheless, Asia-Pacific drives expansion at a 9.23% CAGR, spurred by China's projection to reach a USD 210 billion medical devices market size by 2025 through domestic innovation incentives and digital hospital pilots. Aging demographics amplify chronic-disease burdens; the region will host 60% of the global 65-plus population by 2030, sustaining long-term volume growth.

Europe's unified Medical Device Regulation promotes cross-border harmonization, sustaining demand for outcome-validated solutions. Germany and the United Kingdom lead in robotic surgery and imaging penetration, while France and Italy allocate recovery funds to tele-monitoring infrastructure. The United Kingdom's post-Brexit pathway maintained market continuity but necessitates dual labeling for continental products, a manageable burden for large corporations with in-house regulatory teams.

South America and the Middle East & Africa present emerging opportunities as public-private models finance new hospitals and specialty centers. Brazil's universal system extends imaging capability to underserved regions, creating pull for rugged CT and ultrasound. Gulf Cooperation Council states channel oil revenue into medical tourism, purchasing high-spec radiotherapy and cardiology suites. Currency fluctuations and import tariffs remain barriers, pushing multinationals to establish local assembly or partner with regional distributors to ease access and price volatility.

- Johnson & Johnson

- Abbott Laboratories

- Medtronic

- Siemens Healthineers

- GE Healthcare Technologies Inc.

- Stryker

- Boston Scientific

- Koninklijke Philips

- Beckton Dickinson

- Cardinal Health

- Zimmer Biomet

- Smiths Group

- Edward Lifesciences

- Intuitive Surgical

- Baxter

- Terumo

- FujiFilm Holdings Corporation

- Canon

- Hologic

- Resmed

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging population & rise in chronic diseases

- 4.2.2 Technological convergence in minimally invasive & AI-enabled devices

- 4.2.3 Healthcare infrastructure expansion & spending in emerging markets

- 4.2.4 Digital twins & in-silico trials speeding R&D

- 4.2.5 Point-of-care 3D printing enabling decentralized manufacturing

- 4.2.6 Cybersecure-by-design regulations driving device refresh

- 4.3 Market Restraints

- 4.3.1 Stringent, fragmented regulatory pathways

- 4.3.2 Reimbursement cuts & pricing pressure

- 4.3.3 Geopolitical supply-chain localization complexity

- 4.3.4 Limited availability of rare-earth materials for imaging components

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Pricing Analysis

5 Market Size & Growth Forecasts

- 5.1 By Device Type (Value)

- 5.1.1 Diagnostic Imaging Devices

- 5.1.2 Therapeutic Devices

- 5.1.3 Surgical Devices

- 5.1.4 Monitoring Devices

- 5.1.5 In-Vitro Diagnostics

- 5.1.6 Assistive & Mobility Aids

- 5.1.7 Dental Devices

- 5.1.8 Others

- 5.2 By Technology Platform (Value)

- 5.2.1 Conventional Electro-mechanical & Disposable Devices

- 5.2.2 Wearable & Remote Monitoring

- 5.2.3 Telehealth & mHealth

- 5.2.4 Robotic Surgery

- 5.2.5 3D Printing

- 5.2.6 Augmented / Virtual Reality (AR / VR)

- 5.2.7 Nanotechnology

- 5.2.8 Others

- 5.3 By Therapeutic Application (Value)

- 5.3.1 Cardiology

- 5.3.2 Orthopedics

- 5.3.3 Neurology

- 5.3.4 Ophthalmology

- 5.3.5 General Surgery

- 5.3.6 Others

- 5.4 By End User (Value)

- 5.4.1 Hospitals

- 5.4.2 Clinics

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Home Healthcare

- 5.4.5 Diagnostic Laboratories

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Johnson & Johnson

- 6.3.2 Abbott Laboratories

- 6.3.3 Medtronic plc

- 6.3.4 Siemens Healthineers AG

- 6.3.5 GE Healthcare Technologies Inc.

- 6.3.6 Stryker Corporation

- 6.3.7 Boston Scientific Corporation

- 6.3.8 Philips Healthcare

- 6.3.9 Becton, Dickinson and Company

- 6.3.10 Cardinal Health Inc.

- 6.3.11 Zimmer Biomet Holdings Inc.

- 6.3.12 Smith & Nephew plc

- 6.3.13 Edwards Lifesciences Corporation

- 6.3.14 Intuitive Surgical Inc.

- 6.3.15 Baxter International Inc.

- 6.3.16 Terumo Corporation

- 6.3.17 FujiFilm Holdings Corporation

- 6.3.18 Canon Medical Systems Corporation

- 6.3.19 Hologic Inc.

- 6.3.20 ResMed Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment