PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851250

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851250

Smart Thermostat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

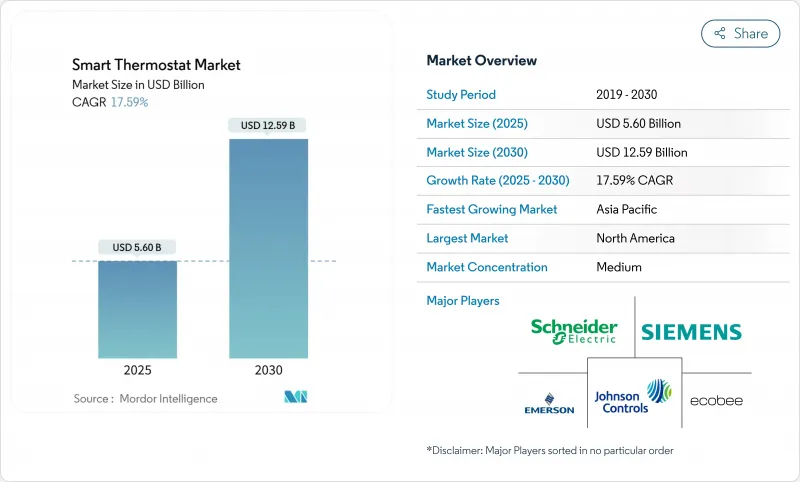

The smart thermostat market stands at USD 5.60 billion in 2025 and is projected to reach USD 12.59 billion by 2030, reflecting a solid 17.59% CAGR through the forecast period.

Growth is primarily driven by a tightening policy focus on energy efficiency, steady grid-modernization investments, and the spread of the Matter interoperability standard that removes ecosystem lock-in. Utilities are treating connected thermostats as grid assets, enrolling them in virtual power plants to shave peak demand and reduce reserve-margin costs.Uptake is further supported by falling sensor prices, the availability of Wi-Fi and Thread dual-band chips, and AI-based optimization that fine-tunes HVAC operation to weather forecasts and occupancy patterns. At the same time, manufacturers are absorbing higher semiconductor and copper costs by emphasizing premium software features rather than competing purely on hardware prices.

Global Smart Thermostat Market Trends and Insights

Government Incentives Drive Accelerated Market Penetration

Generous subsidy programs and dynamic tariffs are moving the smart thermostat market beyond early adopters. Japan's "Energy Saving 2025 Project" covers high-efficiency connected heating systems and offers bonus payments for removing legacy equipment, influencing replacement cycles in condominiums and single-family homes.California has earmarked USD 50 million for low-income households to install intelligent HVAC controls, linking energy equity to flexible-load adoption. Similar rebate structures appear in France, Germany, and South Korea, trimming payback periods to less than three years for most households. Together, these measures lift adoption in regions with both high power prices and climate-policy targets, reinforcing volume growth among retrofit projects and spurring builder demand for pre-installed controls in new homes.

Smart-Home Ecosystem Integration Amplifies Value Proposition

Thread 1.4, released in late 2024, makes credential sharing and self-healing mesh networking standard features for home IoT. The update lets thermostats serve as border routers, routing traffic when Wi-Fi falters and improving whole-home reliability.Apple, Google, and Amazon have publicly committed to Thread 1.4 support in their hub products by 2026, guaranteeing cross-platform pairing without vendor apps. Consumers experience faster onboarding and fewer drop-offs during initial setup, which translates to higher retention for subscription-based energy-services plans. For commercial facilities, open APIs simplify integration with existing building-management software and reduce installer training time. These network effects enlarge addressable demand by rewarding ecosystems that can span lighting, security, and HVAC in a single interface.

Supply Chain Cost Inflation Pressures Affordability

Semiconductor shortages and copper-price swings raised bill-of-materials costs for connected thermostats by 15-20% between 2024 and 2025. U.S. tariffs on Chinese-made smart-home devices compound the increase, leaving brands with a choice of thinner margins or higher shelf prices. Some producers are shifting final assembly to Taiwan, Vietnam, and Mexico to navigate trade barriers and diversify supply risk. Installers report that total retrofit costs, including labor, frequently exceed USD 400, outpacing willingness-to-pay in emerging economies. As a result, several vendors now bundle financing or utility rebate documentation inside their sales portals to soften the initial outlay.

Other drivers and restraints analyzed in the detailed report include:

- Virtual Power Plant Monetization Creates New Revenue Streams

- Matter Protocol Standardization Eliminates Interoperability Friction

- Cybersecurity Vulnerabilities Undermine Consumer Confidence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wi-Fi-enabled units accounted for 64.30% of shipments in 2024, reflecting near-universal router penetration and straightforward installation workflows. This stronghold gives Wi-Fi the single-largest smart thermostat market share in the base year. The segment continues to benefit from higher residential replacement activity, but growth moderates as mesh-capable Thread chips enter mass production. Thread devices are expected to post 21.05% CAGR through 2030, steadily eroding Wi-Fi's lead by offering lower power draw, seamless onboarding, and automatic network healing. Meanwhile, Zigbee remains popular in commercial retrofits because it integrates cleanly with legacy BMS software. Z-Wave keeps a niche among security-system installers that prioritize sub-GHz interference-free links. The rising ability of Matter controllers to bridge Wi-Fi and Thread traffic suggests future homes will carry mixed-stack deployments that optimize cost, range, and battery life without locking owners into one vendor.

Second-generation Thread silicon already embeds dual-stack capability, allowing fallback to 2.4 GHz Wi-Fi if border routers fail. Apple's commitment to release Thread 1.4 firmware to its set-top boxes by 2026 will enlarge the potential addressable base by tens of millions of hubs. For commercial properties, Thread's deterministic latency and multi-path routing improve reliability for occupant-comfort applications, which are sensitive to dropouts. Vendors anticipating this shift are loading mobile apps with network-quality dashboards that highlight Thread link status, easing installer troubleshooting and reinforcing confidence among corporate facility managers.

Retrofit projects represented 57.80% of 2024 unit demand, capitalizing on the vast installed base of standard programmable thermostats ready for replacement. This activity positions retrofit as the largest slice of the smart thermostat market size across the forecast window. The category prospers as device makers introduce universal mounting plates and C-wire adapters that let homeowners self-install in under 30 minutes. In parallel, building-code revisions and green-bond incentives accelerate new-construction demand, driving a 20.21% CAGR for pre-installed systems in homes built after 2025. Larger multifamily developers often specify open-protocol thermostats so that property-management software can aggregate energy data portfolio-wide, enhancing ESG reporting credibility.

Commercial retrofits now draw attention because a single office tower can swap 1,000 conventional wall stats in a weekend, generating immediate energy reductions and fast payback. Regional utilities sweeten the proposition with performance-based rebates that refund up to 30% of project cost once load-shifting metrics are validated. In new buildings, integrated design approaches place thermostats on a shared IP backbone with lighting and access control, simplifying commissioning. Market participants therefore segment their product lines: value-priced do-it-yourself units target homeowners, while professional-grade, BACnet-compatible models satisfy contractors bidding large projects.

Smart Thermostat Market Report is Segmented by Connectivity Type (Wired and Wireless), Installation Type (New Construction and Retrofit), Product Type (Connected/Programmable, Connected/Programmable, and More), End-User (Residential, Commercial, and More), Connectivity Protocol (Wi-Fi, Zigbee, Z-Wave, and More), Product Intelligence Level (Learning Smart Thermostats, Connected/Programmable, and More), and Geography.

Geography Analysis

North America posted the highest 2024 revenue with 38.60% share, aided by Energy Star labeling, state-level demand-response incentives, and high per-capita HVAC penetration. Europe followed, driven by the Fit-for-55 package that compels deep building-energy retrofits by 2030. The Asia Pacific region, however, will record the fastest gains at 17.66% CAGR. China shipped 185 million air-conditioner units in 2024, providing a vast install base that primes upgrades to connected controllers. Japan's carbon-neutrality roadmap requires efficiency upgrades in existing housing stock, and South Korea's smart-home tax credits lower the cost of integrated HVAC controls.

In rapidly urbanizing Southeast Asia, middle-class households view smart thermostats as both status symbols and energy-saving tools during seasonal heatwaves. Government subsidy pools in Thailand and Malaysia now include connected HVAC as eligible equipment, expanding addressable demand. Elsewhere, Latin America posts moderate growth, with Brazil leveraging net-metering reforms and Mexico adopting smart-energy codes for new commercial builds. Middle East buyers focus on controlling the high cooling loads in glass-clad towers, yet cost remains a hurdle in lower-income segments. Regional disparities mean manufacturers must tailor channel strategies, offering budget SKUs in emerging economies while upselling cloud services in mature markets.

- Nest Labs Inc. (Google)

- Resideo Technologies Inc.

- ecobee Inc.

- Emerson Electric Co. (Sensi)

- Lennox International Inc.

- Alarm.com Inc.

- LUX Products Corp.

- APX Group Inc. (Vivint)

- Johnson Controls plc

- Netatmo SA

- Tantalus Systems Corp.

- tado GmbH

- Centrica Hive Ltd.

- Siemens AG

- Amazon.com Inc.

- Schneider Electric SE

- Bosch Thermotechnology

- Carrier Global Corp.

- Trane Technologies plc

- Daikin Industries Ltd.

- Copeland LP

- Robertshaw Controls Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing demand for energy-saving devices

- 4.2.2 Government incentives and dynamic tariff roll-outs

- 4.2.3 Rapid adoption of smart-home ecosystems and IoT hubs

- 4.2.4 Virtual-power-plant (VPP) monetisation via demand response

- 4.2.5 Matter protocol lowers interoperability barriers

- 4.2.6 AI-driven HVAC predictive-maintenance subscriptions

- 4.3 Market Restraints

- 4.3.1 High upfront product and installation cost

- 4.3.2 Data-privacy and cybersecurity concerns

- 4.3.3 Legacy HVAC wiring fragmentation

- 4.3.4 Early-adopter saturation in mature markets

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Connectivity Technology

- 5.1.1 Wireless

- 5.1.1.1 Wi-Fi

- 5.1.1.2 Zigbee

- 5.1.1.3 Z-Wave

- 5.1.1.4 Thread

- 5.1.1.5 Bluetooth

- 5.1.2 Wired

- 5.1.1 Wireless

- 5.2 By Installation Type

- 5.2.1 New Construction

- 5.2.2 Retrofit

- 5.3 By Product Type

- 5.3.1 Learning Smart Thermostats

- 5.3.2 Connected/Programmable

- 5.3.3 Stand-alone/App-only

- 5.4 By End-User

- 5.4.1 Residential

- 5.4.1.1 Single-family Homes

- 5.4.1.2 Multi-family Units

- 5.4.2 Commercial

- 5.4.2.1 Offices

- 5.4.2.2 Retail and Hospitality

- 5.4.2.3 Healthcare Facilities

- 5.4.2.4 Education Campuses

- 5.4.3 Industrial and Others

- 5.4.3.1 Light Industrial

- 5.4.3.2 Data Centres

- 5.4.1 Residential

- 5.5 By Connectivity Protocol

- 5.5.1 Wi-Fi

- 5.5.2 Zigbee

- 5.5.3 Z-Wave

- 5.5.4 Thread (Matter-ready)

- 5.5.5 Bluetooth / BLE

- 5.5.6 Proprietary 915 MHz / Sub-GHz RF

- 5.5.7 Ethernet / Power-over-Ethernet

- 5.6 By Product Intelligence Level

- 5.6.1 Learning Smart Thermostats

- 5.6.2 Stand-alone/App-only (phone-centric)

- 5.6.3 Connected/Programmable

- 5.6.4 Multi-sensor Environment-Aware

- 5.6.5 Voice-assistant-integrated

- 5.6.6 Predictive-maintenance / Self-diagnostic Controllers

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 South Korea

- 5.7.4.4 India

- 5.7.4.5 Australia

- 5.7.4.6 South-East Asia

- 5.7.4.7 Rest of Asia Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 GCC

- 5.7.5.1.2 Turkey

- 5.7.5.1.3 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Nest Labs Inc. (Google)

- 6.4.2 Resideo Technologies Inc.

- 6.4.3 ecobee Inc.

- 6.4.4 Emerson Electric Co. (Sensi)

- 6.4.5 Lennox International Inc.

- 6.4.6 Alarm.com Inc.

- 6.4.7 LUX Products Corp.

- 6.4.8 APX Group Inc. (Vivint)

- 6.4.9 Johnson Controls plc

- 6.4.10 Netatmo SA

- 6.4.11 Tantalus Systems Corp.

- 6.4.12 tado GmbH

- 6.4.13 Centrica Hive Ltd.

- 6.4.14 Siemens AG

- 6.4.15 Amazon.com Inc.

- 6.4.16 Schneider Electric SE

- 6.4.17 Bosch Thermotechnology

- 6.4.18 Carrier Global Corp.

- 6.4.19 Trane Technologies plc

- 6.4.20 Daikin Industries Ltd.

- 6.4.21 Copeland LP

- 6.4.22 Robertshaw Controls Co.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment