PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851275

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851275

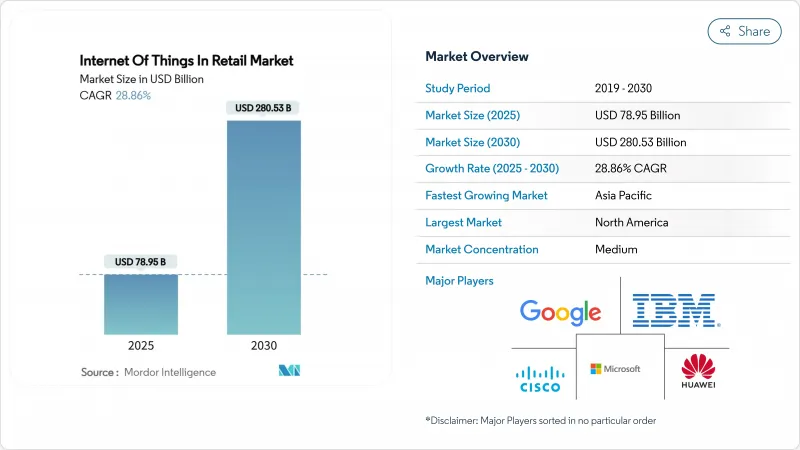

Internet Of Things In Retail - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Internet of Things in retail market stands at USD 78.95 billion in 2025 and is projected to reach USD 280.53 billion by 2030, registering a 28.86% CAGR.

Strong device connectivity, falling sensor costs, and edge-computing maturity are enabling retailers to move from periodic stocktakes to predictive, data-driven decision making. The expanding semiconductor base, wider 5G coverage, and maturing cloud platforms bring down hardware barriers while raising expectations for real-time customer engagement and supply-chain visibility. Retailers also see new revenue streams in retail media networks that monetize first-party data generated by store sensors. Meanwhile, the EU Cyber Resilience Act and similar rules raise compliance costs but ultimately build consumer trust in connected store environments.

Global Internet Of Things In Retail Market Trends and Insights

Adoption of smart shelves and RFID for real-time inventor

RFID inlays have shrunk enough to tag liquids and metals, extending coverage from 30% to 85% of store SKUs and pushing automated stock accuracy gains to 35% while cutting manual checks by 60%. Dynamic-antenna robots now achieve 95.8% pick-up on low shelving and 98.0% on high shelving, allowing storewide audits overnight without staff intervention. Camera systems such as Casino Group's fresh-produce rollout complement RFID by reading visual cues that tags cannot handle. As 2025 systems hit volume production, industry consensus positions RFID as a standard cost of doing business rather than a premium add-on.

Omnichannel retail demand for connected operations

More than 75% of retailers now pursue unified online-offline experiences that require seamless data flow between apps, beacons, and PoS devices. Camera-sensor bundles at Samsoe Samsoe stores lifted men's conversion by 5.5% after adjusting HVAC and lighting in response to live customer analytics. Telstra's edge-AI video analytics deliver 95% accuracy in foot-traffic counts while masking identities on-site, ensuring privacy compliance. FairPrice Group's cloud-connected carts trigger staff alerts when queues grow beyond set limits, turning data into immediate action. Reliable edge processing keeps these systems running even if the WAN link drops, guaranteeing checkout continuity

Security and data-privacy concerns

Ransomware and credential theft increasingly exploit poorly secured sensors, driving average breach costs higher and forcing mid-tier retailers to reevaluate benefit-to-risk ratios. The EU Cyber Resilience Act obliges manufacturers to patch vulnerabilities over the full device life cycle; fines reach EUR 15 million for non-compliance, pushing smaller vendors out of bids. Retailers, therefore, lean toward platforms with Software Bill of Materials transparency and Zero-Trust design. Added encryption and continuous authentication raise compute overhead but reduce liability exposure. As vendor ecosystems consolidate under tougher rules, initial procurement may slow, yet long-term trust is expected to widen adoption.

Other drivers and restraints analyzed in the detailed report include:

- Declining sensor costs and edge-computing maturity

- Retail-media data monetization of in-store IoT

- Interoperability and legacy-system integration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware captured 46.0% of 2024 revenue, anchoring every sensing layer from RFID tags to edge servers within the Internet of Things in the retail market. Services, however, are projected to climb 28.88% per year, reflecting retailer demand for managed connectivity, predictive analytics subscriptions, and device lifecycle outsourcing. Software platforms mediate these layers, turning raw telemetry into replenishment alerts and staff schedules. In revenue terms, managed services are now bundled with hardware in 3- to 5-year contracts, shifting cash flows from capex to opex. Retailers that lack deep IT teams prefer single-point support agreements covering connectivity, firmware patches, and analytics dashboards. Professional services demand spikes during rollouts and again at optimization phases, showing that IoT value realization is a journey rather than a switch-on event. Honeywell-Verizon's 2025 bundle exemplifies this trend, collapsing procurement complexity into one invoice while ensuring 5G uptime warranties.As analytics mature, retailers increasingly benchmark store performance across chains, reinforcing recurring-service stickiness and pushing hardware vendors to adopt consumption-based pricing.

In volume terms, sensors and gateways dominate unit counts, but maintenance tools and monitoring licenses generate higher gross margins. Larger chains negotiate multi-year service-level agreements that guarantee sub-second latency for point-of-sale failover at every site. Over the forecast, devices will continue entering stores; yet revenue curves tilt to software and services, confirming the Internet of Things in retail market's shift to an outcome-based economy where uptime, insight, and security outperform raw device counts.

Smart checkout and POS is expected to be the fastest-rising application at a 31.0% CAGR, reflecting consumer demand for frictionless exits and retailers' drive to redeploy labor. Inventory-centric systems still led with 28.0% of 2024 revenue, but investment dollars now favor customer-facing gains that convert dwell time into higher basket values. The Internet of Things in retail market size for smart checkout solutions is forecast to jump as camera arrays, weight sensors, and computer vision models coalesce into near-instant payment events. Amazon's Just Walk Out blueprint lowered abandonment rates and set shopper expectations globally. In parallel, predictive maintenance applications cut refrigeration downtime in grocery, saving energy and reducing spoilage, with Hussmann reporting a 30% leak-rate drop within the first year of deployment.

Asset tracking remains critical for click-and-collect fulfillment, linking in-store pick paths to customer notification times. Energy and facility-management use cases scale on new carbon-reporting mandates, making real-time kWh dashboards standard in chain store NOCs. Together, these applications underscore how IoT blends operational discipline with customer experience to raise revenue and shrink cost lines.

The Internet of Things (IoT) in Retail Market Report is Segmented by Component (Hardware, Software, and Services), Application (Smart Shelf and Inventory Management, Smart Checkout and POS, and More), Technology (RFID, Bluetooth Low Energy (BLE) Beacons, Wi-Fi, and More), Deployment Mode (On-Premises, Cloud, and More), Retail Format (Supermarkets / Hypermarkets, Convenience Stores, Specialty Stores, and More), and Geography.

Geography Analysis

North America controlled 33.0% of 2024 revenue, backed by early RFID adoption and dense 5G coverage that accelerates edge rollouts. State-by-state cyber rules largely align with federal frameworks, giving chains clear guardrails for experiment budgets. Amazon continues scaling cashier-less formats, and Walmart's chain-wide digital-label program signals mainstream acceptance of dynamic pricing. Retailers also tap hyperscale partners such as Microsoft for managed IoT stacks; Azure consumption by U.S. retailers rose 23% in 2024, indicating deeper system reliance. While new cybersecurity mandates increase baseline costs, predictable regulation supports steady capital plans across 2025-2027.

Asia Pacific is the fastest-growing Internet of Things in retail market at a 33.12% CAGR. The region hosts 1.8 billion mobile subscribers-a vast foundation for payment and loyalty integrations. Local semiconductor output lowers sensor BOM costs, allowing mass deployment across convenience chains in Japan and pop-up kiosks in India. Government digital agendas-from Singapore's Smart Nation to India's ONDC-fund infrastructure that retailers repurpose for last-mile analytics. E-waste rules remain lighter than in Europe, though extended producer-responsibility laws are tightening and nudging vendors toward modular devices. Collectively, cost advantages plus policy tailwinds sustain rapid adoption.

Europe blends strong technology appetite with strict consumer-protection frameworks. GDPR sets the benchmark for data handling, and the upcoming Cyber Resilience Act mandates security-by-design disclosures, potentially elongating procurement cycles. At the same time, ambitious 90% decarbonization targets for 2040 propel energy-monitoring deployments across big-box fleets. The "right to repair" directive passed in 2024 extends device life, boosting service revenue as retailers add in-house repair counters. Overall, Europe's policy landscape tempers initial rollouts but ensures long-term system robustness and customer trust.

- Amazon Web Services Inc.

- ATandT Inc.

- Ayla Networks Inc.

- Bosch Software Innovations GmbH

- Cisco Systems Inc.

- Fujitsu Ltd

- General Electric

- Google LLC

- Hewlett Packard Enterprise

- Hitachi Ltd

- Huawei Technologies Co. Ltd

- IBM Corporation

- Intel Corporation

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Siemens AG

- Zebra Technologies

- PTC Inc.

- Samsung SDS

- Verizon Communications Inc.

- Software AG

- Sensormatic Solutions (Johnson Controls)

- Impinj Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of smart shelves and RFID for real-time inventory

- 4.2.2 Omnichannel retail demand for connected operations

- 4.2.3 Declining sensor costs and edge computing maturity

- 4.2.4 Retail-media data monetization of in-store IoT

- 4.2.5 Carbon-tracking mandates driving energy mgmt IoT

- 4.2.6 5G private networks enabling in-store computer vision

- 4.3 Market Restraints

- 4.3.1 Security and data-privacy concerns

- 4.3.2 Interoperability and legacy-system integration

- 4.3.3 E-waste regulations raise hardware compliance cost

- 4.3.4 Edge-AI bias risks limiting roll-outs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.1.3.1 Managed Services

- 5.1.3.2 Professional Services

- 5.2 By Application

- 5.2.1 Smart Shelf and Inventory Management

- 5.2.2 Asset Tracking and Fleet Management

- 5.2.3 Predictive Equipment Maintenance

- 5.2.4 Smart Checkout and POS

- 5.2.5 Customer Engagement and Marketing

- 5.2.6 Energy and Facility Management

- 5.3 By Technology

- 5.3.1 RFID

- 5.3.2 Bluetooth Low Energy (BLE) Beacons

- 5.3.3 Wi-Fi

- 5.3.4 Zigbee / Z-Wave

- 5.3.5 NFC

- 5.3.6 5G and Cellular IoT (NB-IoT, LTE-M)

- 5.3.7 Computer Vision and AI Cameras

- 5.4 By Deployment Mode

- 5.4.1 On-premises

- 5.4.2 Cloud

- 5.4.3 Edge

- 5.5 By Retail Format

- 5.5.1 Supermarkets / Hypermarkets

- 5.5.2 Convenience Stores

- 5.5.3 Specialty Stores

- 5.5.4 Department Stores

- 5.5.5 eCommerce Warehouses and Dark Stores

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Kenya

- 5.6.5.2.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services Inc.

- 6.4.2 ATandT Inc.

- 6.4.3 Ayla Networks Inc.

- 6.4.4 Bosch Software Innovations GmbH

- 6.4.5 Cisco Systems Inc.

- 6.4.6 Fujitsu Ltd

- 6.4.7 General Electric

- 6.4.8 Google LLC

- 6.4.9 Hewlett Packard Enterprise

- 6.4.10 Hitachi Ltd

- 6.4.11 Huawei Technologies Co. Ltd

- 6.4.12 IBM Corporation

- 6.4.13 Intel Corporation

- 6.4.14 Microsoft Corporation

- 6.4.15 Oracle Corporation

- 6.4.16 SAP SE

- 6.4.17 Siemens AG

- 6.4.18 Zebra Technologies

- 6.4.19 PTC Inc.

- 6.4.20 Samsung SDS

- 6.4.21 Verizon Communications Inc.

- 6.4.22 Software AG

- 6.4.23 Sensormatic Solutions (Johnson Controls)

- 6.4.24 Impinj Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment