PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851313

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851313

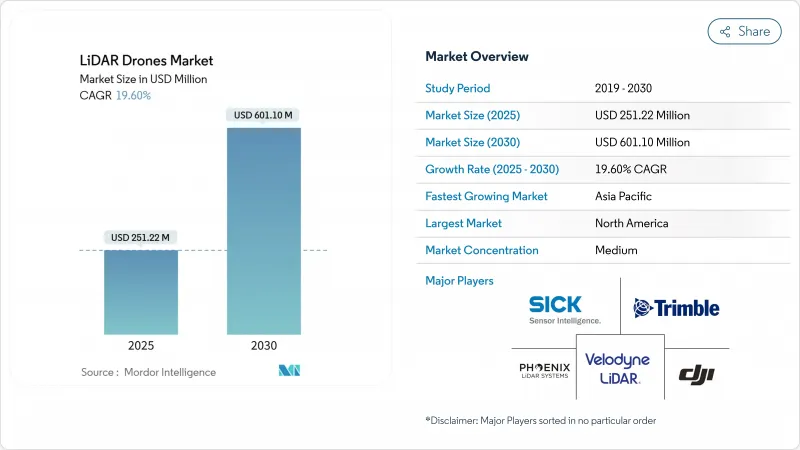

LiDAR Drones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The LiDAR drone market reached USD 251.22 million in 2025 and is forecast to climb to USD 601.10 million by 2030, advancing at a 19.60% CAGR.

Solid-state cost breakthroughs below the USD 400 inflection point, supportive regulatory reforms in major air-space markets, and expanding demand for precision mapping across construction, agriculture, and energy underpin this expansion. Rotary-wing platform upgrades, cloud-native data pipelines, and integrated navigation units are widening the addressable user base, while lower-weight sensors are opening new urban and micro-mapping opportunities. Large infrastructure programs in North America, the European Union, and Asia-Pacific continue to allocate survey budgets toward unmanned systems, and methane-leak detection mandates are accelerating LiDAR payload uptake in the oil and gas sector. Hardware commoditization is steering value toward analytics software and LiDAR-as-a-Service offerings, reshaping competitive strategies and margins.

Global LiDAR Drones Market Trends and Insights

Break-even of Solid-state LiDAR Cost Below USD 400 Enabling Mass-market Drones

Photonics integration and scaled manufacturing have pushed solid-state unit prices below USD 400, removing the historical cost barrier that discouraged smaller contractors, farmers, and municipalities from adopting LiDAR-equipped aircraft. Hesai's 300,000-unit annual volumes exemplify the economies of scale now possible. Mechanical parts elimination improves reliability and cuts maintenance, and patent filings show intense work on beam steering optimization. These shifts are expanding procurement beyond specialized survey firms into mainstream construction and environmental services, bolstering recurring upgrade cycles.

Surge in Sub-250 g Micro-mapping Drones Driven by EU Open-category Rules

Open-category regulations in Europe allow sub-250 g aircraft to be flown without a pilot license, spurring a wave of micro-LiDAR payloads engineered for class C0 drones. Manufacturers now reach point densities near 50 pts/m2 while staying under the weight ceiling. DJI's Air 3S shows how consumer-grade craft now host forward-facing LiDAR for obstacle avoidance and basic mapping. Urban planners and heritage conservators benefit from affordable, quick-deployment tools, and similar frameworks are emerging in Canada and Japan, broadening the addressable base.

EMI Compliance Hurdles for 1550 nm Lasers on Multi-payload Rigs

FAA guidance AC 20-183 requires rigorous EMI, exposure, and ocular hazard calculations when high-power 1550 nm lasers share airframes with radios and radars. Shielding and wavelength-selective filters add 15-25% to system cost, slowing procurement for multi-sensor fleets. Certification backlogs extend lead times, particularly for oil-and-gas operators integrating methane spectroscopy, broadband comms, and GNSS on one rig.

Other drivers and restraints analyzed in the detailed report include:

- Integration of Bathymetric LiDAR on VTOL Drones for Shallow-water Asset Surveys

- Cloud-native SLAM/AI Point-cloud Pipelines Reducing Post-processing Lead-time

- Fragmented Air-traffic Management Delaying BVLOS Permits in ASEAN

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Laser scanners retained 40% of LiDAR drone market share in 2024, reflecting their irreplaceable role in point-cloud generation. Navigation and positioning units are advancing at a 22% CAGR, as centimeter-grade inertial-GNSS fusion has become essential for tightly coupled SLAM workflows. These precise reference packages anchor the LiDAR drone market size for premium survey-grade deliverables. Second-tier components, including thermal regulation modules and edge processors, now incorporate AI accelerators to handle in-flight feature extraction. Manufacturers are rolling out common electrical and data interfaces that shorten development cycles and simplify field swaps, lowering total cost of ownership for fleet operators.

Standardization extends to open-source middleware that allows plug-and-play upgrades of camera, multispectral, or magnetometer units alongside the LiDAR core. Battery management systems gain sophistication as extended-endurance flights stress cell life and thermal limits. Design attention is shifting to shielding against electromagnetic coupling between high-frequency transmitters and light-amplification circuits, a theme amplified by growing 1550 nm deployment.

Rotary-wing aircraft provided 63% of total shipments in 2024, favored for their hover stability, vertical takeoff, and precision positioning around structures. Hybrid VTOL craft, though newer, combine those control benefits with fixed-wing cruise efficiency, allowing operators to surveil corridors exceeding 50 km on a single battery. Fixed-wing designs now include modular nose cones and wing hardpoints capable of hosting dual-sensor payloads, expanding survey productivity per flight hour.

The LiDAR drone market continues to value rotary-wing versatility for cell-tower, facade, and confined-site mapping, yet rising insurance premiums tied to hover time encourage operators to consider fixed-wing sorties where terrain allows launch and recovery strips. Manufacturers answer with quick-swap airframe kits enabling crews to redeploy the same sensor stack across platform types within a single shift, blurring historical boundaries between product classes.

Lidar Drones Market Report is Segmented by Component (Laser Scanners, 905 Nm Mechanical, and More), Product Form-Factor (Rotary-Wing, Fixed-Wing, and More), Operating Altitude (Very-Low, Low, and More), Range (Short, Medium, and More), Service Model (Hardware Sales, Turn-Key LiDAR-As-A-Service, and More), Application (Precision Agriculture, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America preserved 35.7% of global revenues in 2024, benefiting from established BVLOS waiver pathways, robust GNSS correction grids, and federal methane-leak rules that specify 100 kg/h detection thresholds. Energy majors fund fleet rollouts to meet EPA compliance, and state DOTs allocate capital to scan bridges and roads ahead of rehabilitation cycles. Trimble's Q1 2025 USD 841 million earnings reveal sustained instrument demand tied to machine control and survey automation.

Asia-Pacific holds 22% share yet records the steepest growth slope, propelled by China's LiDAR production scale and India's infrastructure build-out. Hesai alone shipped 195,818 sensors in Q1 2025, underlining regional manufacturing muscle. India's public-private corridors embrace drone mapping for land acquisition and progress tracking, while Japan subsidizes local government rice-field surveys. BVLOS harmonization lags across ASEAN, tempering offshore pipeline and power-line reconnaissance expansion.

Europe benefits from uniform air-space provisions under EASA's Open-category, stimulating micro-platform uptake for urban surveying and cultural-heritage archiving. Hexagon reported EUR 564.9 million (USD 664.64 million) recurring revenue for Q3 2024, signaling strong digital reality adoption despite macro headwinds. Single-photon advances promise efficient national mapping, and the Green Deal's biodiversity targets feed demand for forestry and habitat LiDAR baselines.

- DJI

- Leica Geosystems (Hexagon)

- RIEGL Laser Measurement

- Velodyne / Ouster

- Phoenix LiDAR Systems

- YellowScan SAS

- FARO Technologies

- Teledyne Optech

- Trimble Inc.

- Sick AG

- Microdrones GmbH

- senseFly SA

- Terra Drone Corp.

- Innoviz Technologies

- Luminar Technologies

- Parrot Drone SAS

- GeoCue Group Inc.

- Cepton Technologies

- Robosense (LeiShen)

- Topodrone LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Break-even of solid-state LiDAR cost < USD 400 enabling mass-market drones

- 4.2.2 Surge in sub-250 g "micro-mapping" drones driven by EU Open-category rules

- 4.2.3 Integration of bathymetric LiDAR on VTOL drones for shallow-water asset surveys

- 4.2.4 Cloud-native SLAM/AI point-cloud pipelines reducing post-processing lead-time

- 4.2.5 60 % Oil-and-gas methane-leak detection mandates in N. America using LiDAR UAVs

- 4.2.6 African corridor finance (Af CFTA) favouring drone-based topo surveys over manned aircraft

- 4.3 Market Restraints

- 4.3.1 EMI compliance hurdles for 1550 nm lasers on multi-payload rigs

- 4.3.2 Fragmented air-traffic management delaying BVLOS permits in ASEAN

- 4.3.3 Carbon-battery transport regulations raising logistics cost for service providers

- 4.3.4 Limited GNSS correction infrastructure in Caribbean island nations

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Industry Value-Chain Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Laser Scanners

- 5.1.2 905 nm Mechanical

- 5.1.3 905 nm MEMS

- 5.1.4 1550 nm Fiber

- 5.1.5 Navigation and Positioning Systems

- 5.1.6 Inertial Measurement Units

- 5.1.7 Cameras

- 5.1.8 Power and Thermal Modules

- 5.1.9 Other Components

- 5.2 By Product Form-Factor

- 5.2.1 Rotary-Wing

- 5.2.2 Fixed-Wing

- 5.2.3 Hybrid VTOL

- 5.3 By Operating Altitude

- 5.3.1 Very-Low (<120 m)

- 5.3.2 Low (120-300 m)

- 5.3.3 Medium (300-500 m)

- 5.4 By Range

- 5.4.1 Short (<100 m)

- 5.4.2 Medium (100-500 m)

- 5.4.3 Long (>500 m)

- 5.5 By Service Model

- 5.5.1 Hardware Sales

- 5.5.2 Turn-key LiDAR-as-a-Service

- 5.5.3 Analytics SaaS

- 5.6 By Application

- 5.6.1 Construction and Infrastructure

- 5.6.2 Environment and Forestry

- 5.6.3 Precision Agriculture

- 5.6.4 Corridor Mapping (Road, Rail, Pipeline)

- 5.6.5 Mining and Quarrying

- 5.6.6 Defense and Security

- 5.6.7 Disaster Management and Insurance

- 5.7 Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 Germany

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Rest of Asia

- 5.7.4 Middle East

- 5.7.4.1 Israel

- 5.7.4.2 Saudi Arabia

- 5.7.4.3 United Arab Emirates

- 5.7.4.4 Turkey

- 5.7.4.5 Rest of Middle East

- 5.7.5 Africa

- 5.7.5.1 South Africa

- 5.7.5.2 Egypt

- 5.7.5.3 Rest of Africa

- 5.7.6 South America

- 5.7.6.1 Brazil

- 5.7.6.2 Argentina

- 5.7.6.3 Rest of South America

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Funding, Partnerships)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global?level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 DJI

- 6.4.2 Leica Geosystems (Hexagon)

- 6.4.3 RIEGL Laser Measurement

- 6.4.4 Velodyne / Ouster

- 6.4.5 Phoenix LiDAR Systems

- 6.4.6 YellowScan SAS

- 6.4.7 FARO Technologies

- 6.4.8 Teledyne Optech

- 6.4.9 Trimble Inc.

- 6.4.10 Sick AG

- 6.4.11 Microdrones GmbH

- 6.4.12 senseFly SA

- 6.4.13 Terra Drone Corp.

- 6.4.14 Innoviz Technologies

- 6.4.15 Luminar Technologies

- 6.4.16 Parrot Drone SAS

- 6.4.17 GeoCue Group Inc.

- 6.4.18 Cepton Technologies

- 6.4.19 Robosense (LeiShen)

- 6.4.20 Topodrone LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment