PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906945

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906945

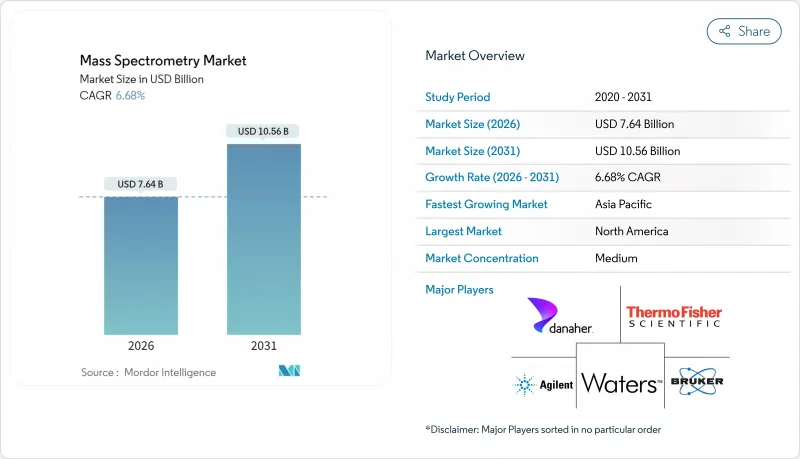

Mass Spectrometry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Mass Spectrometry market is expected to grow from USD 7.16 billion in 2025 to USD 7.64 billion in 2026 and is forecast to reach USD 10.56 billion by 2031 at 6.68% CAGR over 2026-2031.

Momentum stems from rising biologics characterization, tighter food-safety oversight, miniaturized point-of-care systems, artificial-intelligence (AI) data analytics, and multi-omics funding. North America's mature research ecosystem and stringent regulatory framework keep the region at the forefront, yet Asia-Pacific's double-digit trajectory signals a geographical power shift. Competitive differentiation is gravitating toward software-hardware integration, as user demand for real-time, high-throughput insights eclipses pure instrument specifications. Meanwhile, capital constraints in developing-country academic facilities and persistent talent gaps temper adoption, underscoring the need for creative financing and training programs.

Global Mass Spectrometry Market Trends and Insights

Evolving Biologics & Large-Molecule Characterization Needs

Demand for ultra-high-resolution instruments is soaring as drug developers pivot toward monoclonal antibodies and cell-based therapies. Post-translational modification mapping and higher-order structure verification now require hybrid platforms incorporating electron capture dissociation to preserve fragile bonds during fragmentation. Manufacturers that can streamline complex protein workflows are well-positioned to capture future revenue.

Stringent Food-Safety Regulations Accelerating Adoption

The US EPA's 2024 designation of PFOA and PFOS as hazardous substances drove a wave of liquid chromatography-tandem mass spectrometry upgrades across environmental and food laboratories. Comparable policy moves in Europe under ECHA continue to tighten detection limits, propelling instrument placements and method-development services. The food industry's response includes adopting novel approaches like Extractive-liquid sampling electron ionization-mass spectrometry (E-LEI-MS), which enables real-time identification of pesticides on fruit peels without sample preparation, significantly reducing analysis time from hours to minutes.

Capital-Expenditure Constraints in Academic Core Facilities Across Developing Countries

High-end systems range from USD 500,000 to USD 1.5 million, with grant scarcity forces shared-resource centers to postpone upgrades, reducing instrument access for regional researchers. This financial barrier is compounded by ongoing operational costs, including maintenance contracts and consumables, which can represent 15-20% of the initial investment annually. The situation is particularly challenging for core facilities that serve multiple research groups, as they must balance acquisition costs against user fees that remain affordable for local researchers.

Other drivers and restraints analyzed in the detailed report include:

- Miniaturization & High-Throughput Screening Demand in Clinical Diagnostics

- Rising Multi-omics Research Funding

- Shortage of Experienced Mass-Spectrometrists in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid architectures continued to dominate 46.15% of the mass spectrometry market share in 2025, yet MALDI-TOF platforms exhibit the steepest trajectory, posting an 10.88% CAGR outlook to 2031. MALDI-TOF's rapid microbial identification slashed diagnostic turnaround to minutes, lowering hospitalization costs. Beyond microorganisms, MALDI HiPLEX-IHC now delivers multiplexed intact-protein imaging at 5 µm spatial resolution, enabling spatial proteomics in oncology tissue sections.

Second-generation MALDI units also tackle rapid microbiota classification with near-90% accuracy, broadening usage in gut-microbiome studies. Integration with machine-learning algorithms automates spectral-fingerprint libraries, a key differentiator as hospital laboratories scale throughput demands.

The Mass Spectrometry Market Report is Segmented by Technology (Hybrid Mass Spectrometry, Single Mass Spectrometry, MALDI-TOF Mass Spectrometry, and More), Component (Instruments, Ionization Sources, and More), Application (Pharmaceutical & Biotechnology, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 34.65% to the mass spectrometry market in 2025, owing to strong National Institutes of Health funding, a vibrant biotech pipeline, and stringent environmental regulations. The United States Environmental Protection Agency's PFAS mandates require lower detection limits, driving instrument refresh cycles, and specialized consumables. Canada is following up with updated drinking-water quality guidelines, spurring provincial tenders.

Asia-Pacific is forecast to expand at a 9.92% CAGR to 2031 and is central to future volume growth. China's manufacturers secured venture funding to commercialize miniaturized direct-ionization devices, aiming to address domestic demand and export opportunities. Parallel expansion of contract development and manufacturing organizations (CDMOs) in India and South Korea creates recurring demand for compliance-ready platforms.

Europe remains a stable, high-value market, anchored by stringent EFSA and EMA regulations. The ECHA's continuously evolving chemical-safety framework necessitates frequent method-validation updates, sustaining service revenue streams. Middle East & Africa and South America, though smaller in total addressable revenue, exhibit momentum through GCC public-health investments and Brazil's agrochemical-residue monitoring programs, respectively.

- Agilent Technologies

- Thermo Fisher Scientific

- Waters Corporation

- Bruker

- Shimadzu

- Danaher

- PerkinElmer

- LECO

- JEOL Ltd.

- Hitachi

- MKS Instruments (Extrel)

- Bio-Rad Laboratories

- Advion Inc.

- Kore Technology Ltd.

- Analytik Jena GmbH

- Rigaku

- Teledyne FLIR (FLIR Systems)

- TOFWERK AG

- Hiden Analytical Ltd.

- OI Analytical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Evolving Biologics & Large-Molecule Characterization Needs

- 4.2.2 Stringent Food-Safety Regulations Accelerating Adoption

- 4.2.3 Miniaturization & High-Throughput Screening Demand in Clinical Diagnostics

- 4.2.4 Rising Multi-omics Research Funding

- 4.2.5 Increasing R&D Expenditure by Private and Government Research Organizations

- 4.2.6 Emergence of Ambient and Portable Mass Spectrometry Technologies

- 4.3 Market Restraints

- 4.3.1 Capital-Expenditure Constraints in Academic Core Facilities Across Developing Countries

- 4.3.2 Shortage of Experienced Mass-Spectrometrists in Emerging Markets

- 4.3.3 Data-Management & Standardization Challenges in Large-Scale Omics Projects

- 4.3.4 Lengthy Instrument Validation and Regulatory Approval Cycles

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Technology

- 5.1.1 Hybrid Mass Spectrometry

- 5.1.1.1 Triple Quadrupole (LC-MS/MS)

- 5.1.1.2 Quadrupole Time-of-Flight (Q-TOF)

- 5.1.1.3 Fourier-Transform (FT-MS)

- 5.1.2 Single Mass Spectrometry

- 5.1.2.1 Quadrupole

- 5.1.2.2 Time-of-Flight (TOF)

- 5.1.2.3 Ion Trap

- 5.1.3 MALDI-TOF Mass Spectrometry

- 5.1.4 Inductively Coupled Plasma Mass Spectrometry (ICP-MS)

- 5.1.5 Others

- 5.1.1 Hybrid Mass Spectrometry

- 5.2 By Component

- 5.2.1 Instruments

- 5.2.2 Ionization Sources

- 5.2.3 Detectors & Analyzers

- 5.2.4 Software & Informatics

- 5.2.5 Services

- 5.3 By Application

- 5.3.1 Pharmaceutical & Biotechnology

- 5.3.2 Clinical Diagnostics & Proteomics

- 5.3.3 Food & Beverage Testing

- 5.3.4 Environmental Testing

- 5.3.5 Chemical & Petrochemical

- 5.3.6 Forensic & Toxicology

- 5.3.7 Academia & Research Institutes

- 5.3.8 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Agilent Technologies Inc.

- 6.3.2 Thermo Fisher Scientific Inc.

- 6.3.3 Waters Corporation

- 6.3.4 Bruker Corporation

- 6.3.5 Shimadzu Corporation

- 6.3.6 Danaher Corporation (SCIEX)

- 6.3.7 PerkinElmer Inc.

- 6.3.8 LECO Corporation

- 6.3.9 JEOL Ltd.

- 6.3.10 Hitachi High-Tech Corporation

- 6.3.11 MKS Instruments (Extrel)

- 6.3.12 Bio-Rad Laboratories Inc.

- 6.3.13 Advion Inc.

- 6.3.14 Kore Technology Ltd.

- 6.3.15 Analytik Jena GmbH

- 6.3.16 Rigaku Corporation

- 6.3.17 Teledyne FLIR (FLIR Systems)

- 6.3.18 TOFWERK AG

- 6.3.19 Hiden Analytical Ltd.

- 6.3.20 OI Analytical

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment