PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851368

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851368

Supercapacitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

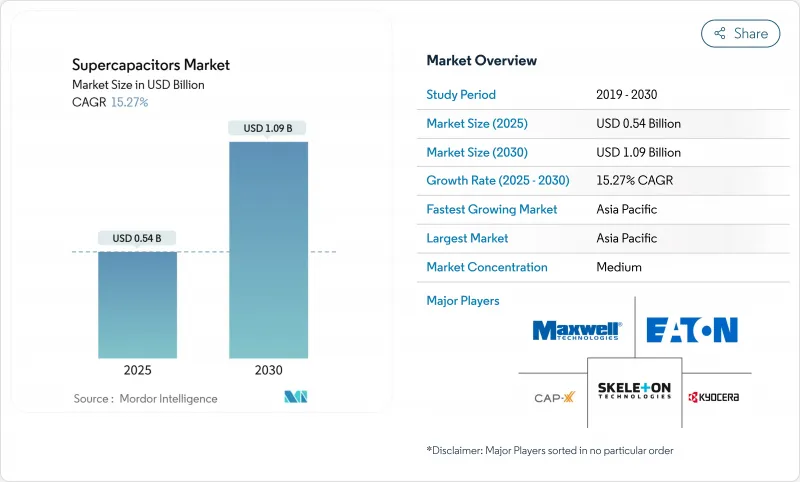

The global supercapacitors market stood at USD 0.54 billion in 2025 and is forecast to reach USD 1.09 billion by 2030, advancing at a 15.27% CAGR.

Growth is supported by electrification rules such as the European Union's 48-volt mild-hybrid mandate, datacenter demand for uninterruptible power during artificial-intelligence (AI) surges, and grid-modernization projects that blend batteries with supercapacitors for rapid frequency response. China continues to anchor production and research, while Korean manufacturers pivot toward energy-storage systems as their lithium-ion share slips. Product innovation centres on hybrid designs that lift energy density toward battery-like levels and graphene electrodes that enable ultra-thin wearables. Supply-chain risks around activated-carbon prices and ionic-liquid electrolytes temper near-term margins but also encourage regional diversification.

Global Supercapacitors Market Trends and Insights

Rapid adoption of regenerative-braking supercapacitor modules in e-bus fleets

Urban transit agencies are scaling regenerative-braking systems that pair batteries with supercapacitors, recovering up to 85% more kinetic energy than battery-only setups. Mercedes-Benz's Intouro hybrid bus cut fuel use by 5% using a 48-volt supercapacitor pack that endures millions of charge cycles without degradation. Chinese cities were first movers and now link hybrid depots to the grid for both vehicle charging and grid-stability services. System suppliers integrate algorithms that shift power between supercapacitors and batteries to match route topography, which lowers total cost of ownership. As electric-bus procurements rise, this capability strengthens the competitive position of the supercapacitors market in mass-transit electrification.

Grid-scale battery-supercapacitor hybrid storage

Utilities value supercapacitors for instant frequency regulation. Demonstrations showed a 17.43% reduction in frequency-drop rates versus standalone lithium-ion arrays, delivering economic benefits 3.2-times greater than battery-only solutions. The U.S. Department of Energy projects levelized storage costs of USD 0.337 per kWh by 2030 as automated cell production scales. Operators also cite environmental advantages because supercapacitors avoid cobalt and nickel. These factors position the supercapacitors market as an essential grid-forming resource that complements long-duration batteries under high-renewable penetration scenarios.

Certification gaps (IEC 62391) limiting residential adoption

IEC 62391 testing procedures prolong qualification timelines and raise costs, especially for smaller firms. Comparative studies show the standard takes longer than Maxwell and QC/T 741-2014 protocols, stretching product launches by up to 12 months. The heavy focus on high-current testing is mismatched with typical household power profiles. This administrative hurdle slows the supercapacitors market from penetrating residential energy-storage segments where simplified compliance would unlock new demand.

Other drivers and restraints analyzed in the detailed report include:

- Graphene-based electrode breakthroughs enabling ultra-thin wearables

- EU 48 V mild-hybrid mandate accelerating demand for 12-48 V modules

- Energy-density plateau (~10 Wh/kg) restricting long-range EV penetration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electric Double-Layer Capacitors maintained a 55.2% share of the supercapacitors market in 2024, reflecting established production lines and proven durability in industrial power buffering. Hybrid Supercapacitors are on track for an 18.1% CAGR to 2030 as they merge battery-like energy storage with classic capacitor power delivery. The hybrid approach answers OEM calls for devices that can ride through seconds-long voltage dips and also sustain longer discharge profiles.

Rapid R&D advances, including lithium-ion capacitor variants, narrow the energy-density gap and extend operating temperatures. Pilot projects in automotive inverters and grid-forming systems showcase cycle lifetimes beyond one million cycles. These traits position hybrids as the next performance benchmark within the supercapacitors industry.

Module assemblies captured 57.8% of the supercapacitors market in 2024 thanks to integrated balancing circuitry and drop-in compatibility for buses, cranes, and wind turbines. Pack configurations, however, are projected to grow 17.4% annually as grid operators and EV makers opt for higher-voltage stacks that exceed 800 V. The supercapacitors market size for pack-level products could double by 2030 as utilities deploy them for sub-second frequency response.

Cell products retain relevance in wearables and industrial controllers where board-level integration and cost sensitivity remain critical. Vendors now offer modular architectures that let customers scale energy in 50-volt increments, shortening project design cycles. Advanced thermal-management features further widen adoption across harsh-duty environments.

The Supercapacitors Market Report is Segmented by Configuration (Type) (Electric Double-Layer Capacitors (EDLC), Pseudo Capacitors, and Hybrid Supercapacitors), Form Factor (Cell, Module, and Pack), Mounting Type (Discrete Components) (Surface-Mount, Radial Leaded, Snap-In, and More), End-User Industry (Consumer Electronics, Energy and Utilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

China controlled 28.2% of global revenue in 2024 due to scale in activated-carbon processing and a deep research base that publishes 65.4% of high-impact papers. Domestic demand from electric-vehicle makers and state-backed grid projects underpins volume growth. State policies that prioritise local energy-storage content further entrench supply-chain ecosystems for the supercapacitors market.

Korea and the broader Asia region are set for a 16.3% CAGR through 2030, propelled by LG Energy Solution, Samsung SDI, and SK On investments that exceed USD 20 billion in new capacity. Korean firms channel expertise in electrode coatings toward pack-level storage systems aimed at North American utilities. Japan contributes precision manufacturing for high-reliability automotive modules, while Southeast Asian nations attract assembly plants seeking diversified supply bases.

The United States leverages Inflation Reduction Act incentives to localise production and deploy supercapacitor-based UPS units in hyperscale datacenters. Europe remains regulation-driven, with the Euro 7 framework spurring automotive demand and grid-modernization funds supporting hybrid storage pilot plants. Emerging regions in Latin America and the Middle East trial supercapacitor packs for microgrid stability, signalling long-term addressable growth for the supercapacitors market.

List of Companies Covered in this Report:

- Maxwell Technologies Inc. (Tesla)

- Skeleton Technologies SA

- CAP-XX Ltd.

- Eaton Corporation plc

- Panasonic Holdings Corp.

- LS Mtron Ltd.

- Kyocera Corp.

- Nippon Chemi-Con Corp.

- Supreme Power Solutions Co.

- Shanghai Aowei Technology Development Co.

- Samwha capacitor Group

- Nanoramic Laboratories (FastCAP)

- Nawa Technologies SAS

- Cornell Dubilier Electronics Inc.

- Toyo capacitor Co.

- Shenzhen Topmay Electronic Co.

- Liaoning Brother Electronics Technology Co.

- Chengdu ZT-Energy Tech Co.

- Loxus Inc.

- Nantong Jianghai capacitor Co. Ltd

- Beijing HCC Energy

- Jinzhou Kaimei Power Co. Ltd (KAM)

- Shanghai Green Tech Co. Ltd (GTCAP)

- Shenzhen Topmay Electronic Co. Ltd

- SEMG (Seattle Electronics Manufacturing Group (HK) Co. Ltd)

- Shanghai Pluspark Electronics Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of regenerative-braking supercapacitor modules in e-bus fleets

- 4.2.2 Grid-scale battery-supercapacitor hybrid storage

- 4.2.3 Graphene-based electrode breakthroughs enabling ultra-thin wearables

- 4.2.4 EU 48 V mild-hybrid mandate accelerating demand for 12-48 V modules

- 4.2.5 Supercapacitor-based UPS deployment by Datacenter hyperscalers to meet ESG targets

- 4.3 Market Restraints

- 4.3.1 Activated-carbon precursor price volatility inflating BOM costs

- 4.3.2 Certification gaps (IEC 62391) limiting the residential adoption

- 4.3.3 Energy-density plateau (~10 Wh/kg) restricting long-range EV penetration

- 4.3.4 Ionic-liquid electrolyte supply-chain bottlenecks elongating lead-times

- 4.4 Regulatory and Technological Outlook (Electrode Material, CAsia-Pacificitance Ratings, Electrolyte, Voltage Range)

- 4.5 Impact of Macroeconomic Factors and Trade Tarrifs

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Configuration (Type)

- 5.1.1 Electric Double-Layer Capacitors (EDLC)

- 5.1.2 Pseudocapacitors

- 5.1.3 Hybrid Supercapacitors

- 5.2 By Form Factor

- 5.2.1 Cell

- 5.2.2 Module

- 5.2.3 Pack

- 5.3 By Mounting Type (Discrete Components)

- 5.3.1 Surface-Mount

- 5.3.2 Radial Leaded

- 5.3.3 Snap-in

- 5.3.4 Screw Terminal

- 5.4 By End-User Industry

- 5.4.1 Consumer Electronics

- 5.4.1.1 Wearables

- 5.4.1.2 Smartphones and Tablets

- 5.4.1.3 SSD and Memory Backup

- 5.4.2 Energy and Utilities

- 5.4.2.1 Grid Frequency Regulation

- 5.4.2.2 Renewable Integration (Wind, Solar)

- 5.4.2.3 Microgrid and UPS

- 5.4.3 Industrial Equipment

- 5.4.3.1 Robotics and Automation

- 5.4.3.2 Power Tools

- 5.4.3.3 Heavy Machinery and Cranes

- 5.4.4 Automotive and Transportation

- 5.4.4.1 Passenger Cars

- 5.4.4.1.1 48 V Mild Hybrid

- 5.4.4.1.2 Start-Stop Micro Hybrid

- 5.4.4.2 Commercial Vehicles

- 5.4.4.2.1 Buses

- 5.4.4.2.2 Trucks

- 5.4.4.3 Rail and Tram

- 5.4.4.4 Aviation and Aerospace

- 5.4.5 Data Centers and Telecom

- 5.4.6 Defense and Space

- 5.4.7 Others (Medical Devices, Agri-drones)

- 5.4.1 Consumer Electronics

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Europe

- 5.5.3 China

- 5.5.4 Japan

- 5.5.5 Korea and Rest of Asia-Pacific

- 5.5.6 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Maxwell Technologies Inc. (Tesla)

- 6.4.2 Skeleton Technologies SA

- 6.4.3 CAP-XX Ltd.

- 6.4.4 Eaton Corporation plc

- 6.4.5 Panasonic Holdings Corp.

- 6.4.6 LS Mtron Ltd.

- 6.4.7 Kyocera Corp.

- 6.4.8 Nippon Chemi-Con Corp.

- 6.4.9 Supreme Power Solutions Co.

- 6.4.10 Shanghai Aowei Technology Development Co.

- 6.4.11 Samwha capacitor Group

- 6.4.12 Nanoramic Laboratories (FastCAP)

- 6.4.13 Nawa Technologies SAS

- 6.4.14 Cornell Dubilier Electronics Inc.

- 6.4.15 Toyo capacitor Co.

- 6.4.16 Shenzhen Topmay Electronic Co.

- 6.4.17 Liaoning Brother Electronics Technology Co.

- 6.4.18 Chengdu ZT-Energy Tech Co.

- 6.4.19 Loxus Inc.

- 6.4.20 Nantong Jianghai capacitor Co. Ltd

- 6.4.21 Beijing HCC Energy

- 6.4.22 Jinzhou Kaimei Power Co. Ltd (KAM)

- 6.4.23 Shanghai Green Tech Co. Ltd (GTCAP)

- 6.4.24 Shenzhen Topmay Electronic Co. Ltd

- 6.4.25 SEMG (Seattle Electronics Manufacturing Group (HK) Co. Ltd)

- 6.4.26 Shanghai Pluspark Electronics Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment