PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851379

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851379

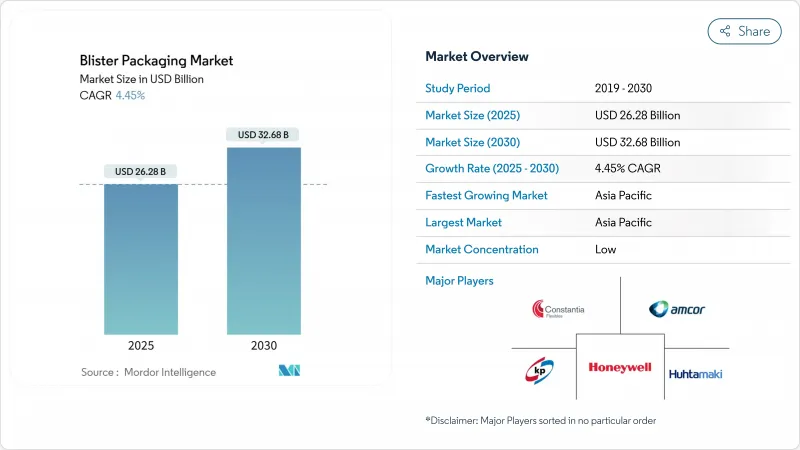

Blister Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The blister packaging market size stands at USD 26.28 billion in 2025 and is set to climb to USD 32.68 billion by 2030, translating into a steady 4.45% CAGR over the forecast horizon.

Robust demand from prescription drugs, over-the-counter medications, and increasingly complex biologics underpins this growth, while unit-dose formats continue to displace bulk bottles across hospital, long-term-care, and retail channels. Regulatory pressure-most notably the European Union's Regulation 2025/40 mandating full recyclability by 2030 and the U.S. FDA's strengthened tamper-evident rules-has sparked a wave of compliance-driven innovation that commands premium pricing and protects margins even as raw-material costs fluctuate. Asia-Pacific leads global demand thanks to China and India's manufacturing scale, while North America and Europe shape high-value niches through serialization, smart packs, and sustainability upgrades. Meanwhile, industry consolidation-typified by Amcor's USD 8.43 billion purchase of Berry Global-signals a pivot toward integrated flexible, rigid, and intelligent solutions that can serve multinational pharmaceutical clients.

Global Blister Packaging Market Trends and Insights

Growing Geriatric Population and Chronic-Disease Prevalence

The global cohort aged 60 and above will surge 56% by 2030, intensifying demand for user-friendly blister packs that improve medication adherence while offering tamper evidence. Senior-centric designs-larger print, color coding, and low opening force-are being commercialized by converters such as Drug Plastics Group, whose Pop & Click closure reduces required hand pressure by roughly a quarter. Chronic conditions like diabetes and cardiovascular disease further amplify multi-dose pack adoption, enabling clear visual cues for complex regimes and reinforcing premium price realization for blister specialists.

Demand for Unit-Dose and Patient-Adherence Packs

Hospitals, pharmacies, and home-health providers increasingly link reimbursement to adherence metrics, elevating the role of blister-based unit-dose packs. Automated equipment from Parata now integrates directly with electronic health-record platforms, cutting dispensing errors while simplifying repack operations. The FDA's proposal to require single-unit containers for orally disintegrating OTC forms underscores regulatory endorsement of unit-dose safety benefits. Pharmaceutical brands also leverage unit-dose blisters for differentiation, combining brand visibility with tamper-evidence that bottles cannot replicate.

Volatile PVC and Aluminium Prices

China's jump in PVC import tariffs from 1% to 5.5% in 2025 lifted resin costs for downstream converters, spotlighting vulnerability to policy shifts. Indian converters remain exposed since 60% of their PVC feedstock is sourced abroad, making hedging and backward integration central to risk management. Aluminium foil prices also swing with energy markets, straining smaller blister firms that lack the scale to lock in multi-year contracts.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Tamper-Evident Formats

- Smart Blister Packs with NFC/QR for Track-and-Trace

- Tightening PVC Disposal/Recycling Legislation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermoforming commanded 64.33% of global revenues in 2024 and will grow 5.67% a year as drug makers favor its low tooling cost, fast line speeds, and compatibility with diverse film substrates. Brown Machine's Quad-Series thermoformers now deliver up to 250,000 lids per hour while trimming energy use by roughly one-quarter, giving contract packers productivity gains that sustain the blister packaging market's momentum. Smaller laboratories gain access through modular machines introduced by GEA, broadening supplier bases beyond large multinationals.

Cold-form foil, though a minority share, is indispensable for moisture- or light-sensitive molecules. Drug makers often specify aluminium-aluminium structures when stability studies demand near-zero water vapor transmission. As biologics and high-potency actives proliferate, cold form's installed base expands, intensifying R&D into thinner foils and hybrid lamination that cut weight without compromising barrier. Together, these advances widen the technology palette, reinforcing the blister packaging market as a versatile platform for both mass-production generics and niche specialty drugs.

Plastic films, led by PVC, PET, and PP, accounted for 68.26% of blister revenues in 2024 thanks to mature supply chains and easy thermoformability. Yet heightened scrutiny of fossil-based materials is spurring rapid incremental gains for paper-based solutions, which log a 7.34% CAGR through 2030. TekniPlex now offers transparent recyclable mid-barrier PET blisters containing 30% recycled content, illustrating how converters preserve pharmacopoeial compliance while advancing circularity.

Paperboard entrants such as Rohrer's EcoVolve-30 use fiber plus functional coatings to withstand line forming temperatures and protect moisture-tolerant tablets. Although moisture sensitivity limits broad substitution, brand owners deploy paper variants in vitamins, nutraceuticals, and short shelf-life SKUs, bolstering eco-credentials. Over time, material science breakthroughs are expected to let hybrid fiber-polymer laminates secure higher-barrier categories, reinforcing the blister packaging market size trajectory and aligning with regulatory recycled-content mandates.

The Blister Packaging Market Report is Segmented by Process (Thermoforming, Cold Forming), Material (Plastic Films, Aluminium, Paper and Paperboard), Product Type (Carded/Face-Seal Blisters, Clamshell Blisters, Trapped and Full-Card Blisters, and More), End-User Industry (Pharmaceuticals, Nutraceuticals and Dietary Supplements, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led with 41.34% of 2024 revenue and will outpace all regions at 7.56% CAGR as China and India scale active-pharmaceutical-ingredient output and align with Western quality standards. WuXi STA's new Taixing API site and proposed Singapore expansion exemplify regional manufacturing build-out, directly lifting local demand for compliant blister lines. China's tariff hike on imported PVC to 5.5% further encourages domestic film extrusion, reinforcing supply-chain localization that underpins the blister packaging market in East Asia.

North America remains a technological bellwether. Stringent FDA serialization plus tamper-evidence rules sustain premium margins for intelligent formats, while machinery capex expands in anticipation of biologic fill-finish demand. PMMI projects packaging-machinery sales will hit record highs by 2027, with pharmaceutical applications outperforming food and beverage. Amcor's Berry Global acquisition consolidates flexible and rigid capabilities inside a single platform, ensuring scale and vertical reach that smaller North American converters will find hard to match.

Europe confronts the most aggressive sustainability legislation. Regulation 2025/40 enforces recyclability and 30% recycled content in PET packs by 2030, directing investment into circular-ready designs. TekniPlex's showcase of transparent recyclable mid-barrier blisters demonstrates compliance pathways that still satisfy stringent EMA barrier specifications. Clinical-trial packs also adapt to EU 536/2014, prompting Catalent to equip its Shiga, Japan, site with high-speed blister lines that serve pan-regional studies and underscore the global nature of compliance-driven demand. Consequently, the blister packaging market share in Europe remains resilient even as material choices evolve.

- Amcor plc

- WestRock Company

- Constantia Flexibles GmbH

- Klockner Pentaplast Group

- Sonoco Products Company

- DuPont de Nemours, Inc.

- Honeywell International Inc.

- Tekni-Plex, Inc.

- Dow Inc.

- Uflex Ltd.

- Huhtamaki Oyj

- Winpak Ltd.

- Bilcare Ltd.

- Bemis Company LLC (Amcor)

- Lotte Aluminium Co., Ltd.

- Toyo Aluminium K.K.

- Pharma Packaging Solutions

- R-Pharm Germany GmbH

- FormPaks Ltd.

- Zhejiang Hualian Pharmaceutical Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing geriatric population and chronic-disease prevalence

- 4.2.2 Demand for unit-dose and patient-adherence packs

- 4.2.3 Regulatory push for tamper-evident formats

- 4.2.4 Smart blister packs with NFC / QR for track-and-trace

- 4.2.5 Personalized-medicine small-batch blister lines

- 4.2.6 PVC-to-PE retrofit demand driven by sustainability

- 4.3 Market Restraints

- 4.3.1 Volatile PVC and aluminium prices

- 4.3.2 Tightening PVC disposal / recycling legislation

- 4.3.3 PVDC-resin supply bottlenecks

- 4.3.4 OTC stick-pack and sachet substitution

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Process

- 5.1.1 Thermoforming

- 5.1.2 Cold Forming

- 5.2 By Material

- 5.2.1 Plastic Films (PVC, PET, PP, PE, rPET, COP, others)

- 5.2.2 Aluminium (ALU-ALU, PTP foil)

- 5.2.3 Paper and Paperboard

- 5.3 By Product Type

- 5.3.1 Carded / Face-Seal Blisters

- 5.3.2 Clamshell Blisters

- 5.3.3 Trapped and Full-Card Blisters

- 5.3.4 Child-Resistant / Senior-Friendly Packs

- 5.4 By End-User Industry

- 5.4.1 Pharmaceuticals

- 5.4.2 Nutraceuticals and Dietary Supplements

- 5.4.3 Consumer Electronics and Hardware

- 5.4.4 Personal Care and Cosmetics

- 5.4.5 Other End-user Industry

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 United Arab Emirates

- 5.5.4.1.2 Saudi Arabia

- 5.5.4.1.3 Turkey

- 5.5.4.1.4 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Nigeria

- 5.5.4.2.3 Egypt

- 5.5.4.2.4 Rest of Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 WestRock Company

- 6.4.3 Constantia Flexibles GmbH

- 6.4.4 Klockner Pentaplast Group

- 6.4.5 Sonoco Products Company

- 6.4.6 DuPont de Nemours, Inc.

- 6.4.7 Honeywell International Inc.

- 6.4.8 Tekni-Plex, Inc.

- 6.4.9 Dow Inc.

- 6.4.10 Uflex Ltd.

- 6.4.11 Huhtamaki Oyj

- 6.4.12 Winpak Ltd.

- 6.4.13 Bilcare Ltd.

- 6.4.14 Bemis Company LLC (Amcor)

- 6.4.15 Lotte Aluminium Co., Ltd.

- 6.4.16 Toyo Aluminium K.K.

- 6.4.17 Pharma Packaging Solutions

- 6.4.18 R-Pharm Germany GmbH

- 6.4.19 FormPaks Ltd.

- 6.4.20 Zhejiang Hualian Pharmaceutical Co.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment