PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851386

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851386

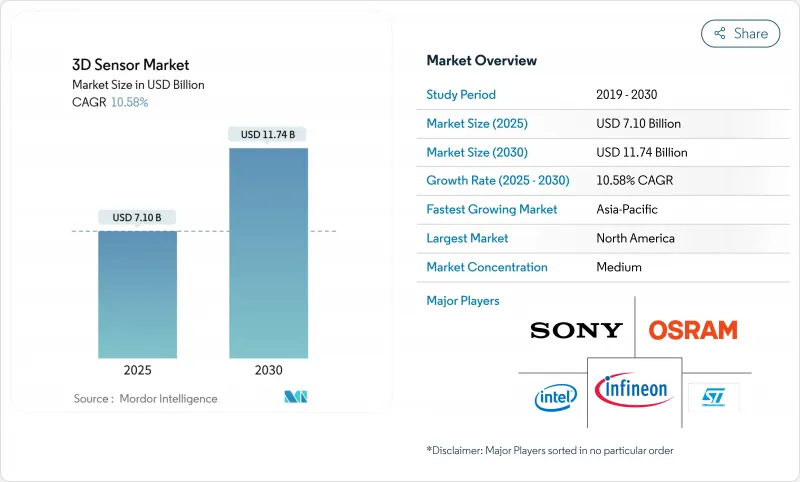

3D Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The 3D sensor market is valued at USD 7.1 billion in 2025 and is forecast to reach USD 11.74 billion by 2030, advancing at a 10.58% CAGR.

Growth is anchored in rising demand for spatial awareness across consumer electronics, automotive safety, industrial automation, and emerging mixed-reality platforms. Miniaturization of optical components, integration of on-sensor edge processing, and falling unit costs are enlarging the addressable base of applications. Regional momentum is strongest in Asia-Pacific, where deep electronics manufacturing capacity shortens design-to-production cycles, while government-backed smart-city spending is accelerating adoption in the Middle East. Competitive differentiation is now moving from discrete hardware specifications toward complete sensing-plus-software stacks that reduce latency and power consumption in embedded environments.

Global 3D Sensor Market Trends and Insights

Smartphone facial recognition adoption fuels regional leadership

Premium handsets in Asia are expected to pass a 65% attachment rate for 3D facial recognition by 2026, consolidating the 3D sensor market's largest single application base. Structured-light and Time-of-Flight modules now generate sub-millimeter depth maps reliable under varied lighting, enabling secure payments, avatar creation, and personalized UI. Asian OEMs have moved sensors beneath the display to save frontage without sacrificing robustness. Volume scaling in handset production is lowering component costs for adjacent sectors such as wearables and smart-home devices, reinforcing a virtuous demand cycle.

Automotive LiDAR transforms vehicle-safety benchmarks

European automakers are installing LiDAR-based ADAS ahead of the 2026 NCAP mandate for pedestrian automatic emergency braking. Solid-state designs deliver centimeter-level accuracy at up to 200 m, meeting stringent automotive reliability tests while shrinking bill-of-materials. The regulatory push in Europe is echoed by voluntary commitments in North America, creating a homogeneous requirements profile that benefits global tier-one sensor suppliers. As cost curves decline, LiDAR uptake is expected to cascade from premium models into mid-segment vehicles, enlarging the 3D sensor market addressable volume.

Thermal challenges hinder VCSEL array miniaturization

As VCSEL emitters are packed closer to achieve higher optical power in ever-smaller footprints, central elements in an array can run 50 °C hotter than ambient. Elevated junction temperatures degrade efficiency and risk catastrophic failure. Device makers are experimenting with segmented drive circuits and advanced packaging that routes heat laterally to copper layers before it reaches sensitive optics. Adoption of these innovations will moderate the current drag on the 3D sensor market by preserving performance inside compact consumer devices.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of depth-sensing cameras in mixed-reality headsets

- Collaborative robots advance precision electronics assembly

- EU AI Act creates compliance burdens for biometric sensing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Image Sensors accounted for 62% of 2024 revenue, confirming their foundational role in the 3D sensor market. Robust demand arises from smartphones, industrial inspection, and robotics that depend on high-resolution depth maps spanning 5 m ranges with sub-millimeter precision. Multi-stack backside-illuminated architectures and on-chip HDR pipelines continue to improve signal-to-noise ratios. Leading suppliers have shifted to 300 mm wafer lines, driving yield improvements that lower cost per megapixel.

Gesture-Recognition Sensors record the fastest expansion, advancing at a 14.8% CAGR to 2030 as touchless interfaces penetrate infotainment consoles, interactive kiosks, and healthcare devices. New modules fuse ToF depth, millimeter-wave radar, and AI inference on a single substrate, enabling recognition of complex hand poses under variable lighting. Upskilled OEM design teams in Asia-Pacific further shorten development cycles, helping this segment accumulate a higher share of the 3D sensor market.

Position Sensors, Inertial Measurement Units, and Thermopile elements round out the portfolio, each addressing specific accuracy or environmental requirements where optical methods face limits. Cross-licensing among suppliers is consolidating IP, ensuring multi-vendor availability for system designers.

The image-sensor subcategory represents the largest 3D sensor market size at USD 4.4 billion in 2024 and is on course for a mid-single-digit CAGR through 2030. Within this category, back-illuminated stacked CMOS architectures commanded roughly 50% of shipments, underscoring the move toward higher dynamic range at lower power. Gesture-recognition modules, despite a smaller base, are set to contribute USD 1.6 billion incremental revenue by 2030 as public and private spaces look to minimize shared-surface contact. This surge illustrates how diversified form factors collectively reinforce growth momentum across the 3D sensor market.

Time-of-Flight sensors generated 46% of total revenue in 2024, reflecting their favorable cost-to-accuracy balance. Indirect ToF dominates consumer devices thanks to mature VCSEL emitters and simple single-photon avalanche diode (SPAD) receivers. Direct ToF variants, with picosecond timing resolution, lead in robotics and industrial automation requiring longer working distances. Integration of capacitive depth-computation engines on the same die as photodiodes slashes latency, feeding edge-AI models without round-trips to host processors.

LiDAR solutions, though smaller in today's shipment volumes, are growing at a 13.61% CAGR through 2030, propelled by automotive autonomy programs and infrastructure digital-twin projects. Solid-state scanning, micro-electro-mechanical beam steering, and frequency-modulated continuous-wave architectures are improving range while lowering moving-part counts. These advances reduce cost per point cloud and, by extension, broaden the 3D sensor market beyond premium vehicles.

Structured-light remains a preferred choice for close-range, high-detail capture such as facial unlocking and industrial metrology. Stereo vision and ultrasound maintain footholds in specific niches-stereo offers a lens-based alternative without active illumination, while ultrasound succeeds where optical paths are obstructed by dust or fluid.

3D Sensor Market Share Report is Segmented by Product (Position Sensors, Image Sensors and More), Technology (Structured Light, Time-Of-Flight and More), End-User Vertical (Consumer Electronics, Automotive and More), Component (IR VCSEL Emitters, and More), and Geography (North America, Europe, Asia and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 38% of global revenue in 2024, reflecting the region's dense semiconductor fabs, skilled optics workforce, and vertically integrated supply chains. China accounts for about 40% of regional sales, bolstered by domestic smartphone OEMs that are aggressively adopting in-house depth modules. Japan excels in precision glass molding and wafer-level optics, feeding high-accuracy sensors for industrial robotics. South Korea leverages advanced packaging know-how to integrate logic and sensing into single substrates, improving thermal performance in compact modules.

The Middle East, though starting from a low base, is on course for a 12.87% CAGR through 2030. National smart-city roadmaps fund installations of depth-sensing street furniture, automated retail kiosks, and AI-enabled healthcare imaging suites. Domestic system integrators in the Gulf Cooperation Council are forging partnerships with European and Asian component vendors to localize solutions that meet climatic and linguistic requirements. Rapid procurement cycles in the retail sector are accelerating pilot-to-production timelines, providing near-term upside for the 3D sensor market.

North America remains the epicenter of LiDAR RandD, supported by a vibrant venture ecosystem and defense-driven research grants. Tier-one automotive suppliers here lead the push toward chip-scale beam steering. Europe sustains demand in automotive and industrial automation despite rigorous data-protection laws, spurring sensor designs that process personal data at the edge. South America shows early adoption in security and agritech, while Africa's deployments are mainly confined to logistics hubs and mining operations that require rugged sensing solutions.

- Intel Corp.

- Sony Group Corp.

- ams OSRAM AG

- STMicroelectronics N.V.

- Infineon Technologies AG

- Lumentum Holdings Inc.

- Apple Inc. (PrimeSense)

- Samsung Electronics Co. Ltd.

- OmniVision Technologies Inc.

- Panasonic Holdings Corp.

- Cognex Corp.

- Sick AG

- LMI Technologies Inc.

- Teledyne e2v

- Qualcomm Inc.

- SoftKinetic (Sony DepthSense)

- Melexis N.V.

- Himax Technologies Inc.

- Velodyne Lidar Inc.

- XYZ Interactive Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Smartphone Facial Recognition Adoption (Asia)

- 4.2.2 Automotive LiDAR-Assisted ADAS Roll-outs (Europe)

- 4.2.3 Proliferation of Depth-Sensing Cameras in AR/VR Headsets (US)

- 4.2.4 Deployment of Collaborative Robots in Electronics Assembly (South Korea, Taiwan)

- 4.2.5 Integration of 3D Sensors in Security and Surveillance Systems

- 4.2.6 Edge-AI Powered 3D Vision for Smart Retail (GCC)

- 4.3 Market Restraints

- 4.3.1 Thermal Management Challenges in Miniaturised VCSEL Arrays

- 4.3.2 Privacy-Led Regulatory Scrutiny on Depth Cameras (EU AI Act)

- 4.3.3 High Power Consumption in Continuous Time-of-Flight Modules

- 4.3.4 Semiconductor Supply-Chain Tightness for Gallium-Nitride Lasers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Patent Landscape

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 Position Sensors

- 5.1.2 Image Sensors (3D Cameras)

- 5.1.3 Temperature Sensors

- 5.1.4 Accelerometer and IMU Sensors

- 5.1.5 Ambient-Light and Proximity Sensors

- 5.1.6 Gesture-Recognition Sensors

- 5.2 By Technology

- 5.2.1 Structured Light

- 5.2.2 Time-of-Flight (dToF and iToF)

- 5.2.3 Stereo Vision

- 5.2.4 LiDAR (Flash and FMCW)

- 5.2.5 Ultrasound

- 5.3 By End-User Vertical

- 5.3.1 Consumer Electronics

- 5.3.2 Automotive and Transportation

- 5.3.3 Healthcare and Medical Devices

- 5.3.4 Industrial Automation and Robotics

- 5.3.5 Security and Surveillance

- 5.3.6 Aerospace and Defence

- 5.4 By Component

- 5.4.1 IR VCSEL Emitters

- 5.4.2 Depth Image Sensors

- 5.4.3 System-on-Chip Processors

- 5.4.4 Optics and Filters

- 5.4.5 Illumination Modules

- 5.4.6 Software and Algorithms

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Nordics (Sweden, Norway, Denmark, Finland)

- 5.5.4 Middle East

- 5.5.4.1 GCC

- 5.5.4.2 Turkey

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Nigeria

- 5.5.6 Asia-Pacific

- 5.5.6.1 China

- 5.5.6.2 Japan

- 5.5.6.3 South Korea

- 5.5.6.4 India

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Intel Corp.

- 6.4.2 Sony Group Corp.

- 6.4.3 ams OSRAM AG

- 6.4.4 STMicroelectronics N.V.

- 6.4.5 Infineon Technologies AG

- 6.4.6 Lumentum Holdings Inc.

- 6.4.7 Apple Inc. (PrimeSense)

- 6.4.8 Samsung Electronics Co. Ltd.

- 6.4.9 OmniVision Technologies Inc.

- 6.4.10 Panasonic Holdings Corp.

- 6.4.11 Cognex Corp.

- 6.4.12 Sick AG

- 6.4.13 LMI Technologies Inc.

- 6.4.14 Teledyne e2v

- 6.4.15 Qualcomm Inc.

- 6.4.16 SoftKinetic (Sony DepthSense)

- 6.4.17 Melexis N.V.

- 6.4.18 Himax Technologies Inc.

- 6.4.19 Velodyne Lidar Inc.

- 6.4.20 XYZ Interactive Technologies

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment