PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907240

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907240

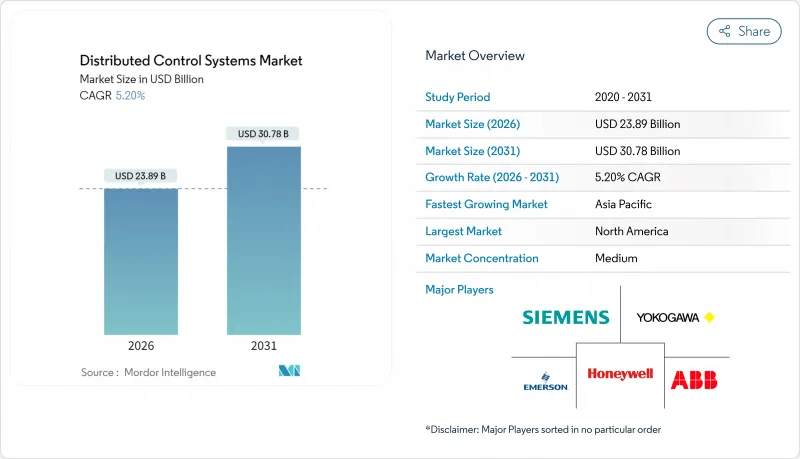

Distributed Control Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The distributed control systems market was valued at USD 22.71 billion in 2025 and estimated to grow from USD 23.89 billion in 2026 to reach USD 30.78 billion by 2031, at a CAGR of 5.20% during the forecast period (2026-2031).

The green-hydrogen build-out, carbon-capture projects, nuclear power additions, and the pharmaceutical shift to continuous production anchor growth. Vendors are expanding software-defined architectures, digital-twin integration, and edge connectivity to unlock operational gains, while small plants adopt scaled-down platforms that lower entry costs. Rising cybersecurity requirements, shortages of certified engineers, and residual semiconductor constraints temper the pace but do not derail the expansion. Competitive momentum centers on predictive maintenance, modular deployment, and subscription licensing that spread capital outlays.

Global Distributed Control Systems Market Trends and Insights

Energy Transition Drives DCS Demand in Green Hydrogen and CCUS Facilities

Green-hydrogen capacity announcements reached 16.4 million tons in 2024 and each new plant installs sophisticated control platforms valued at USD 2-10 million. DCS architectures must handle intermittent renewable power, ensure hydrogen safety, and flex for rapid electrolyzer efficiency gains forecast at 20-30% within five years. Vendors are packaging modular control nodes that scale with plant phases, letting operators upgrade without wholesale rip-and-replace. Europe and the Middle East lead early adoption, but North American developers are quickly issuing RFQs tied to Inflation Reduction Act incentives. The long investment horizon underpins a stable pipeline of distributed control systems market projects well beyond 2030.

Nuclear and SMR Projects Requiring Cyber-secure Safety-Classified DCS

Regulators now demand air-gapped, safety-class DCS with certified redundancy for every new reactor. The U.S. Nuclear Regulatory Commission tightened cyber rules in 2025, raising qualification costs but also locking in premium pricing for compliant platforms. SMR vendors specify digital safety channels that shorten physical wiring runs, cut construction schedules, and support remote diagnostics. Europe and China are standardizing on similar frameworks, while Gulf countries add nuclear units to decarbonize desalination. Certification cycles that run 18 months or more keep new entrants out and reinforce the position of incumbent suppliers in the distributed control systems market.

High Up-front CAPEX versus Modern PLC/SCADA Alternatives

Open process automation pilots show 52% cost savings over classic DCS builds, tempting small and mid-tier operators that weigh every capital dollar Vendors counter with subscription licenses, flexible I/O, and pre-engineered libraries that trim hardware counts. Yet sticker shock still postpones projects in ASEAN, Latin America, and parts of Africa, shaving 0.8 percentage points off distributed control systems market growth.

Other drivers and restraints analyzed in the detailed report include:

- Offshore Floating LNG Complexity Elevates High-Reliability DCS Adoption

- Pharma Continuous Manufacturing Spurs Modular Batch DCS Installations

- Scarcity of DCS-Certified Engineers and Lifecycle Service Staff

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware retained a 54.35% distributed control systems market share in 2025, reflecting end-user preference for field-proven controllers, universal I/O, and redundant networks. The distributed control systems market size for hardware hit USD 12.34 billion, buoyed by replacement cycles in energy and chemicals. Vendors now ship configurable I/O slices that accept analog, digital, or HART signals on any channel, cutting cabinet counts by up to 30%. Universal cards also support late-stage design changes, a compelling feature for EPC contractors facing tight schedules. Controller platforms add fast cycle times for high-density PID loops in green hydrogen plants, safeguarding accuracy when power supply fluctuates with renewables.

Software revenue, though smaller, is rising 7.55% per year as operators embrace analytics, virtualization, and OT-IT convergence. Model-predictive algorithms embedded in historian layers fine-tune setpoints and shave energy consumption 2-5%. Virtualized servers host multiple control domains on a single hypervisor, easing failover and patch management. Service portfolios evolve as well: Emerson's factory resident engineers guarantee KPIs, while ABB's lifecycle software plans bundle cyber hardening and alarm-rationalization updates. This pivot reshapes value capture across the distributed control systems market, shifting focus from capital goods to recurring service streams.

Hybrid architectures blended centralized supervisory nodes with distributed edge controllers to secure 45.40% of the distributed control systems market size in 2025. Plants adopt this topology to migrate legacy I/O in phases, preserve wiring, and layer new analytics without wholesale rip-and-replace. In a typical retrofit, on-premise virtual machines host logic while deterministic Ethernet rings connect field modules, yielding latency under 50 microseconds. Hybrid layouts also simplify cybersecurity zoning, keeping safety loops isolated yet data-accessible via secure proxies.

Fully redundant high-availability designs grow fastest at 8.95% CAGR as pharma, LNG, and nuclear end-users mandate zero unplanned downtime. Redundancy spans controllers, power, switches, and even GPS-synchronized time stamps to maintain sequence-of-events accuracy. Siemens demonstrated a virtual PLC in a production Audi line that migrated workloads between servers without interrupting motion control. Centralized controllers still serve turbine islands and batch digesters where deterministic cycles trump flexibility, but their share of the distributed control systems market declines as modular digital plants dominate new capex.

Distributed Control System (DCS) Market Report Segments the Industry Into by Component (Hardware, Software, Services), by End-User Vertical (Power Generation, Oil & Gas, and More), Architecture (Centralized Controller Systems and More), Deployment Model(On-Premise and More), Plant Size(Small ( Less Than 5000 I/O) and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 37.60% share of the distributed control systems market in 2025, anchored by China's refining and chemicals capacity and India's rapid infrastructure build-out. Regional suppliers like Supcon win municipal water and mid-tier chemical jobs, yet global majors still dominate multi-billion-dollar LNG and nuclear projects. Beijing's smart-manufacturing program funds retrofits that couple DCS data with enterprise AI, expanding software pull-through. India's PLI incentives spur pharmaceutical and battery plants that specify modular, scalable DCS from day one. Southeast Asian economies add flexible packaging lines and biodiesel units, sustaining mid-single-digit growth.

The Middle East posts the fastest 6.95% CAGR, powered by Saudi Arabia's Vision 2030, which automates 40% of the kingdom's grid and builds green-hydrogen clusters. GCC states commit to USD 3.1 trillion in capital projects, each embedding OT-IT convergence from design. Local integrators partner with multinationals to meet localization quotas, broadening the vendor ecosystem within the distributed control systems market.

North America modernizes aging power and chemicals infrastructure, embedding cybersecurity as a funding prerequisite under DOE and DHS programs. The Inflation Reduction Act funnels incentives to carbon capture and clean fuels, both heavy DCS users. Europe emphasizes sustainability; process plants deploy advanced analytics to trim energy and comply with Fit-for-55 targets. South America invests in copper and lithium mining that uses edge-connected control for remote sites, while Africa rolls out desalination and grid upgrades blending local renewables, creating pockets of double-digit demand.

- ABB Ltd.

- Emerson Electric Co.

- Honeywell International Inc.

- Siemens AG

- Yokogawa Electric Corporation

- Schneider Electric SE

- Mitsubishi Electric Corporation

- Rockwell Automation, Inc.

- Valmet Oyj

- Azbil Corporation

- Omron Corporation

- Novatech LLC

- Toshiba Corporation

- Hitachi, Ltd.

- GE Digital (General Electric Co.)

- Fuji Electric Co., Ltd.

- Supcon Technology Co., Ltd.

- Hollysys Automation Technologies Ltd.

- Endress+Hauser Group Services AG

- BandR Industrial Automation GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy Transition Drives DCS Demand in Green Hydrogen and CCUS Facilities

- 4.2.2 Nuclear and SMR Projects Requiring Cyber-secure Safety-Classified DCS

- 4.2.3 Offshore Floating LNG Complexity Elevates High-Reliability DCS Adoption

- 4.2.4 Pharma Continuous Manufacturing Spurs Modular Batch DCS Installations

- 4.2.5 Digital-Twin-Integrated DCS for Predictive Maintenance in Brownfields

- 4.2.6 Remote Operations Centres in Mining Accelerate Edge-Connected DCS

- 4.3 Market Restraints

- 4.3.1 High Up-front CAPEX versus Modern PLC/SCADA Alternatives

- 4.3.2 Scarcity of DCS-Certified Engineers and Lifecycle Service Staff

- 4.3.3 Semiconductor Supply Crunch for High-Performance Controller Hardware

- 4.3.4 Lengthy Cyber-security Certification and Compliance Cycles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Industry Capacity and Investment Trends

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Architecture

- 5.2.1 Centralized Controller Systems

- 5.2.2 Hybrid / Distributed Hybrid Systems

- 5.2.3 Fully Redundant High-Availability Systems

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud / Edge-Hosted

- 5.4 By Industry Vertical

- 5.4.1 Power Generation

- 5.4.1.1 Thermal Power Plants

- 5.4.1.2 Renewable and Battery Storage Plants

- 5.4.1.3 Nuclear Power Plants

- 5.4.2 Oil and Gas

- 5.4.2.1 Upstream

- 5.4.2.2 Midstream

- 5.4.2.3 Downstream and Refineries

- 5.4.3 Chemicals and Petrochemicals

- 5.4.4 Mining and Metals

- 5.4.5 Pulp and Paper

- 5.4.6 Pharmaceuticals and Life Sciences

- 5.4.7 Food and Beverage

- 5.4.8 Water and Wastewater

- 5.4.9 Other Industries

- 5.4.1 Power Generation

- 5.5 By Plant Size (Controller I/O)

- 5.5.1 Small ( greater than 5 000 I/O)

- 5.5.2 Medium (5 000 - 15 000 I/O)

- 5.5.3 Large (less than 15 000 I/O)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.2 Caribbean

- 5.6.3 South America

- 5.6.3.1 Brazil

- 5.6.3.2 Argentina

- 5.6.3.3 Rest of South America

- 5.6.4 Europe

- 5.6.4.1 Germany

- 5.6.4.2 United Kingdom

- 5.6.4.3 France

- 5.6.4.4 Italy

- 5.6.4.5 Nordics

- 5.6.4.6 Rest of Europe

- 5.6.5 Middle East

- 5.6.5.1 UAE

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Qatar

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.7 Asia-Pacific

- 5.6.7.1 China

- 5.6.7.2 Japan

- 5.6.7.3 India

- 5.6.7.4 South Korea

- 5.6.7.5 ASEAN

- 5.6.7.6 Rest of Asia-Pacific

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 ABB Ltd.

- 6.4.2 Emerson Electric Co.

- 6.4.3 Honeywell International Inc.

- 6.4.4 Siemens AG

- 6.4.5 Yokogawa Electric Corporation

- 6.4.6 Schneider Electric SE

- 6.4.7 Mitsubishi Electric Corporation

- 6.4.8 Rockwell Automation, Inc.

- 6.4.9 Valmet Oyj

- 6.4.10 Azbil Corporation

- 6.4.11 Omron Corporation

- 6.4.12 Novatech LLC

- 6.4.13 Toshiba Corporation

- 6.4.14 Hitachi, Ltd.

- 6.4.15 GE Digital (General Electric Co.)

- 6.4.16 Fuji Electric Co., Ltd.

- 6.4.17 Supcon Technology Co., Ltd.

- 6.4.18 Hollysys Automation Technologies Ltd.

- 6.4.19 Endress+Hauser Group Services AG

- 6.4.20 BandR Industrial Automation GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment