PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851439

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851439

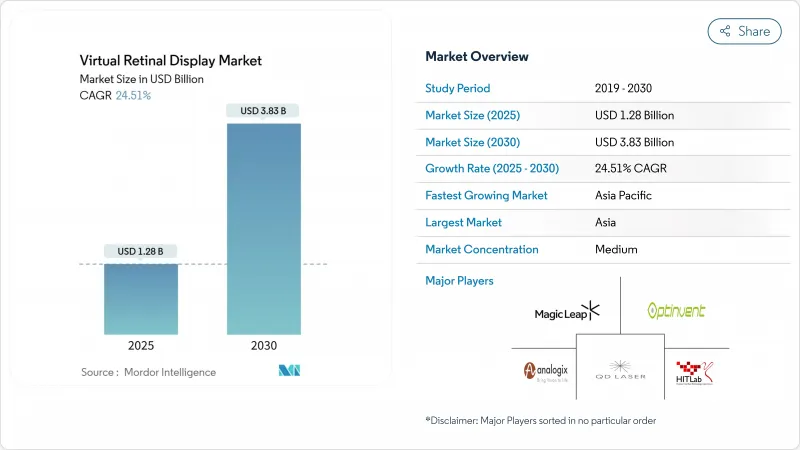

Virtual Retinal Display - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The virtual retinal display market size is is estimated reached USD 1.28 billion in 2025 and is expected to attain USD 3.83 billion by 2030, registering a 24.51% CAGR.

Light-weight retinal projection is moving from experimental labs to mainstream production because silicon-photonics costs are declining, military orders are accelerating, and healthcare providers in developed economies are digitizing vision-care workflows. Transitioning from screen-based to screen-less augmented-reality architecture removes viewing-angle and ambient-light limits while enabling glasses-grade form factors. Procurement programs such as the U.S. Army's soldier color MicroLED initiative and Japan's aged-care vision rehabilitation funding are pulling demand forward. Meanwhile, component makers are shrinking controllers, lasers, and waveguides, which lowers power budgets and opens consumer electronics channels.

Global Virtual Retinal Display Market Trends and Insights

Surging Demand for Ultra-Compact Near-Eye Displays in Military Smart Helmets

Defense programs prioritize displays invisible to night-vision detectors yet bright in daylight. The U.S. Army's Light Secure Special Warfare Display project funds prototypes that illuminate the retina directly, eliminating outward light leakage. Kopin's soldier color MicroLED contracts worth more than USD 7.5 million underscore how ruggedized retinal projection meets size, weight, and power targets for field use.

Rapid Adoption of Retinal Projection Aids for Low-Vision Patients across Japan and DACH

Randomized trials show retinal laser eyewear improves acuity where lenses fail, prompting Japan's insurers and German clinics to reimburse high-end systems. Streamlined EU-MDR approvals and generous coverage in Switzerland support premium therapeutic devices, encouraging manufacturers to prioritize health-care-focused designs.

High Per-Unit Laser Scanner ASPs Causing BOM Pressures below USD 400 AR Glass Price-Point

RGB laser engines still consume up to 40% of total device cost because compound-semiconductor wafers and precision MEMS scanners lack mass-volume scale. Automotive experience shows similar price rigidity for AEC-Q100 mirrors, meaning consumer brands must subsidize optics or forego sub-USD 400 price targets.

Other drivers and restraints analyzed in the detailed report include:

- Shift from Screen-Based to Screen-Less AR Wearables Driven by Silicon-Photonics Cost Drops in U.S.

- Vision-Safe Class-1 Laser Regulations Enabling Wider Consumer Adoption in EU

- Complex FDA and MDR Pathways for Implantable/Therapeutic VRDs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Display Light Source elements, chiefly RGB laser and MicroLED engines, accounted for 34.5% of virtual retinal display market share in 2024. Their dominance stems from the direct link between optical efficiency and battery life. Eye-Tracking & Calibration Modules are expanding fastest at 26.7% CAGR, fueled by AI-enabled gaze analytics. The virtual retinal display market size for Eye-Tracking is expected to widen as MEMS mirrors remain supply-constrained, nudging integrators toward software-centric precision monitoring. Texas Instruments' DLPC8445 controller shrinks by 90% while driving 4K UHD, proving backend silicon keeps pace with front-end lasers.

Optical Combiners and Waveguides are advancing through collaborations such as DigiLens and Avegant, which merge transparent waveguides with retinal projectors. Meanwhile, Q-Pixel's 10,000 PPI tunable polychromatic LEDs hint at single-pixel architectures that could lower alignment tolerances and yield gains. As vertical integration deepens, component vendors that control both emitters and control electronics command sustainable margins.

AR Smart Glasses delivered 41% of virtual retinal display market revenue in 2024, cementing their role as the anchor hardware category. Implantable/Low-Vision Aids, though smaller today, will post a 27.2% CAGR to 2030 as aging populations and insurer reimbursement accelerate uptake. The virtual retinal display market size for therapeutic aids is poised to climb because clinical evidence keeps expanding. Investments such as Quanta Computer's additional USD 5 million in Vuzix improve waveguide throughput, signaling contract manufacturing's growing influence.

Standalone Retinal Projection Headsets persist in defense and industrial simulation niches where long-mission runtimes justify dedicated power packs. Automotive HUDs await qualified MEMS mirrors, which restrains volume scaling despite Texas Instruments' new DLP4620S-Q1 automotive micromirror introduction through Mouser in March 2025. Market skews show consumer convenience versus professional specialization, and suppliers must balance the two roadmaps.

The Virtual Retinal Display Market Report is Segmented by Component (Display Light Source, MEMS Scanning Unit, and More), Product Type (Standalone Retinal Projection Headsets, Augmented-Reality Smart Glasses, and More), Application (Medical and Life Sciences, Aerospace and Defense, and More), Resolution (HD (Upto 720p), Full HD (1080p), and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 27.8% revenue share in 2024 and is forecast to compound 27.6% annually through 2030, reflecting unmatched semiconductor fabs, optics polishing supply chains, and domestic consumer appetites. China's foundry incentives push down laser-die pricing, and Japan's healthcare system actively deploys therapeutic devices for age-related degeneration. South Korea's display giants couple OLED competencies with MicroLED pilot lines, while Taiwan tightens backend packaging yields.

North America leverages defense budgets and university R&D. The virtual retinal display market benefits from the U.S. Army's successive microLED contracts and CHIPS-Act-backed silicon-photonics fabs that localize critical optics. Canada offers streamlined medical-device reviews, making it an attractive first-in-region for therapeutic launches, and Mexico's maquiladora corridors provide tariff-free final assembly for export within North America.

Europe remains regulatory pacesetter. Class-1 laser regulations, coupled with the Valeda photobiomodulation precedent, furnish predictable frameworks that manufacturers can replicate globally. Germany and Switzerland merge precision optics machining with med-tech funding, fostering an ecosystem tailored to high-value medical displays. Nordic early-adopters test lifestyle-oriented AR eyewear, providing feedback loops for battery life and ergonomics. EU energy directives additionally steer suppliers toward low-power designs, giving European players leverage in sustainability-minded markets.

- Avegant Corporation

- QD Laser, Inc.

- Magic Leap, Inc.

- Texas Instruments Incorporated

- Himax Technologies, Inc.

- eMagin Corporation

- Vuzix Corporation

- OmniVision Technologies, Inc.

- Sony Group Corporation

- Kopin Corporation

- STMicroelectronics N.V.

- MicroVision, Inc.

- SeeYa Technology Co., Ltd.

- Syndiant, Inc.

- DigiLens Inc.

- Lumus Ltd.

- Mojo Vision Inc.

- Analogix Semiconductor, Inc.

- Jenoptik AG

- Corning Incorporated

- Optivent

- Human Interface Technology Laboratory

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Ultra-Compact Near-Eye Displays in Military Smart Helmets

- 4.2.2 Rapid Adoption of Retinal Projection Aids for Low-Vision Patients across Japan and DACH

- 4.2.3 Shift from Screen-Based to Screen-Less AR Wearables Driven by Silicon-Photonics Cost Drops in U.S.

- 4.2.4 Vision-Safe Class-1 Laser Regulations Enabling Wider Consumer Adoption in EU

- 4.2.5 Integration of AI Eye-Tracking Modules Boosting Immersive Training Simulators in North America

- 4.3 Market Restraints

- 4.3.1 High Per-Unit Laser Scanner ASPs Causing BOM Pressures below USD 400 AR Glass Price-Point

- 4.3.2 Complex FDA and MDR Pathways for Implantable/Therapeutic VRDs

- 4.3.3 Latency and Speckle Artifacts in RGB-Laser Engines Limiting Gaming Experience

- 4.3.4 Shortage of Automotive-Grade MEMS Mirrors (AEC-Q100) for Head-Up Displays

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Display Light Source (RGB Laser, Micro-LED, OLED)

- 5.1.2 MEMS Scanning Unit

- 5.1.3 Driver and Control Electronics

- 5.1.4 Eye-Tracking and Calibration Module

- 5.1.5 Optical Combiner and Waveguide

- 5.1.6 Others

- 5.2 By Product Type

- 5.2.1 Standalone Retinal Projection Headsets

- 5.2.2 Augmented-Reality Smart Glasses

- 5.2.3 Automotive Head-Up Displays

- 5.2.4 Implantable/Low-Vision Aids

- 5.2.5 Others

- 5.3 By Application

- 5.3.1 Medical and Life Sciences

- 5.3.2 Aerospace and Defense

- 5.3.3 Consumer Electronics and Gaming

- 5.3.4 Automotive and Transportation

- 5.3.5 Industrial, Education and Training

- 5.4 By Resolution

- 5.4.1 HD (Upto 720p)

- 5.4.2 Full HD (1080p)

- 5.4.3 2K-4K

- 5.4.4 Above 4K

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 South America

- 5.5.3.1 Brazil

- 5.5.3.2 Rest of South America

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South-East Asia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Gulf Cooperation Council Countries

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Avegant Corporation

- 6.4.2 QD Laser, Inc.

- 6.4.3 Magic Leap, Inc.

- 6.4.4 Texas Instruments Incorporated

- 6.4.5 Himax Technologies, Inc.

- 6.4.6 eMagin Corporation

- 6.4.7 Vuzix Corporation

- 6.4.8 OmniVision Technologies, Inc.

- 6.4.9 Sony Group Corporation

- 6.4.10 Kopin Corporation

- 6.4.11 STMicroelectronics N.V.

- 6.4.12 MicroVision, Inc.

- 6.4.13 SeeYa Technology Co., Ltd.

- 6.4.14 Syndiant, Inc.

- 6.4.15 DigiLens Inc.

- 6.4.16 Lumus Ltd.

- 6.4.17 Mojo Vision Inc.

- 6.4.18 Analogix Semiconductor, Inc.

- 6.4.19 Jenoptik AG

- 6.4.20 Corning Incorporated

- 6.4.21 Optivent

- 6.4.22 Human Interface Technology Laboratory

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment