PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851446

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851446

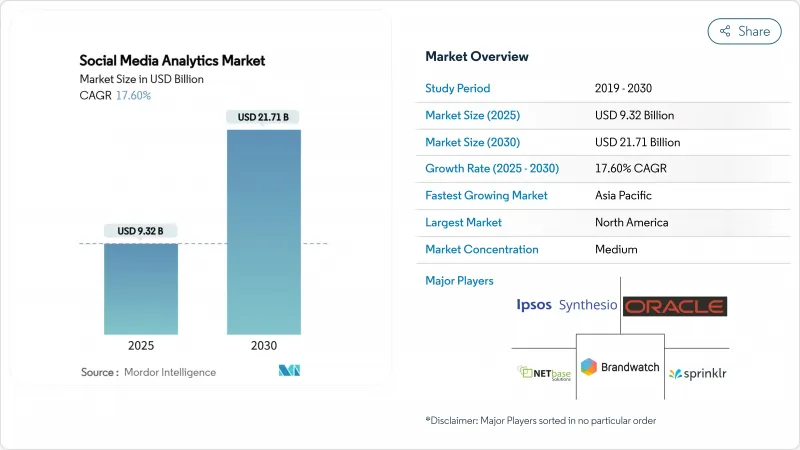

Social Media Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The social media analytics market size stands at USD 9.32 billion in 2025 and is forecast to reach USD 21.71 billion by 2030, advancing at a 17.6% CAGR.

Surging enterprise demand for real-time sentiment detection, predictive behavioral modeling, and campaign ROI measurement underpins this expansion. Growth also reflects a decisive pivot from stand-alone brand monitoring toward unified, AI-driven insight engines that ingest text, image, audio, and video at scale. Accelerated cloud migration, the proliferation of social commerce, and fresh data-privacy mandates are reshaping solution roadmaps. Vendors able to combine multimodal processing, transparent model governance, and domain-specific data connectors are capturing share as buyers consolidate point tools into integrated customer-experience stacks. Competitive intensity remains high because switching costs are modest and proof-of-value cycles are short; as a result, product roadmaps emphasize continuous model retraining and embedded GenAI co-pilots to sustain differentiation.

Global Social Media Analytics Market Trends and Insights

Exponential Growth of Number of Social Media Users

More than 5.24 billion individuals engage on social channels in 2025, expanding data volumes and pushing the social media analytics market toward scalable cloud architectures that parse billions of daily interactions. Rising video-first engagement on TikTok, with 2.50% average interaction rates versus 0.50% on Instagram, forces vendors to embed image and video classifiers, displacing text-only sentiment tools. Healthcare providers leverage this user surge to track public health signals, with 90% of US adults sourcing health information on social platforms. Data diversity strengthens vendor lock-in because proprietary domain ontologies and language models improve accuracy over time. However, the need to de-duplicate bots and fake interactions escalates compute costs and necessitates continual algorithmic refinement.

GenAI-Powered Insight Engines Driving Upsell in North America

North American enterprises invest heavily in GenAI to transform passive monitoring into predictive guidance. Sixty-nine percent of regional marketers call GenAI revolutionary for content personalization. Advanced transformer models now detect misinformation with 99.68% accuracy, lifting overall data fidelity. Banking pilots that applied Long Short-Term Memory networks across 136,150 social posts achieved 91% customer-sentiment classification accuracy, enabling micro-segmented campaign offers. Yet only 12% of firms report clear GenAI ROI, creating advisory and managed-service opportunities for providers that can bridge the skills gap. Vendors rolling out low-code model-training interfaces and explainability dashboards are best positioned to capture expansion revenue.

Stringent Privacy Regulations Limiting Data Granularity

GDPR enforcement cut third-party tracking capability by 14.79% for EU publishers, compelling platforms to devise privacy-preserving analytics such as federated learning. The California Consumer Privacy Act extends similar constraints across the United States. Meta's "Pay or Okay" policy illustrates how consent frameworks reduce data availability and complicate cross-platform user stitching. Vendors able to deliver aggregated, cohort-level insights while preserving individual privacy comply with regulation and reduce client risk exposure.

Other drivers and restraints analyzed in the detailed report include:

- Acceleration of In-App Social Commerce ROI Tracking

- Brand-Safety Metric Mandates by Global Advertisers

- Analytics Skill-Set Gap for Multimodal Data Interpretation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions contributed 65% of 2024 revenue, underlining their role as the entry point to the social media analytics market. Subscription licenses provide predictable margins, yet enterprises now confront implementation backlogs that favor service engagements. Services are forecast to rise at a 23.3% CAGR as firms seek model calibration, taxonomy design, and regulatory mapping. This uptick illustrates how the social media analytics market size for implementation and optimization eclipses basic platform fees, especially when GenAI workflows demand bespoke prompt engineering. Sprinklr's USD 796.4 million FY25 revenue, up from USD 618.2 million in FY23, showcases the dual-stream model of software plus advisory.

The momentum in professional services also stems from vertical compliance nuances. Healthcare clients require HIPAA alignment, while banking customers demand model explainability for credit-risk decisions. Providers that pool domain experts with data scientists reduce time-to-value and deepen wallet share. Consequently, advisory partners co-develop outcome-based pricing tied to conversion uplift or churn reduction, aligning incentives and boosting recurring revenue.

Cloud captured 72% of the social media analytics market share in 2024 and is projected to sustain a 21.8% CAGR through 2030 on the strength of auto-scaling and managed security. Elastic GPU clusters process video streams and transformer models more cost-effectively than most on-premise alternatives. Hybrid options persist in sectors bound by data-residency rules, yet hyperscaler investment in regional zones lowers sovereignty barriers. The social media analytics market size for cloud workloads will therefore expand as real-time dashboards become board-level operational tools.

Cloud-native providers leverage continuous deployment to push weekly feature releases that refine bot-detection, language coverage, and compliance templates. Integration with broader data-warehouse ecosystems such as Snowflake and Databricks enables unified marketing, sales, and service visibility. Conversely, legacy on-premise installations struggle with model-versioning and patch latency, increasing operational risk.

The Social Media Analytics Market Report is Segmented by Component (Solutions, Services), Deployment Mode (Cloud, On-Premise), Module (Social Media Monitoring and Tracking, Social Media Measurement/Listening and Analytics), End-User Industry (Media and Entertainment, IT and Telecom, BFSI, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the social media analytics market with 38% revenue in 2024, buoyed by sophisticated digital-ad ecosystems and early GenAI rollouts. More than 75% of US ad expenditure is online, driving pervasive use of social listening tools within omnichannel campaign orchestration. Enterprises face rising compliance overhead due to state-level privacy statutes, prompting demand for policy-aware analytics frameworks. Despite maturity, growth continues as brands extend usage from marketing into risk, investor relations, and workplace culture assessment.

Asia-Pacific posts the highest regional CAGR at 21.3% through 2030 as mobile-first populations adopt social commerce at scale. The region's USD 77 billion social-media ad spend in 2024, up 15% year over year, anchors investment in cross-language sentiment and influencer fraud detection. China's ecosystem innovation-such as Taobao's live-stream selling-spills over to Southeast Asia, creating green-field analytics demand. India's multilingual diversity further necessitates adaptable ontologies, spurring local-language model development partnerships.

Europe records steady growth because GDPR and the Digital Services Act force enterprises to seek compliant analytics alternatives rather than abandon insight generation. Vendors that embed consent management, on-device processing, and differential-privacy reporting expand pipeline among cautious buyers. Meanwhile, Latin America, Middle East, and Africa begin adopting off-the-shelf cloud analytics as internet penetration rises. Urban clusters in Brazil and the Gulf states mirror advanced market behaviors, accelerating social media analytics market adoption without incurring heavy localization expenditure.

- Sprinklr

- Oracle Corporation

- Synthesio (Crimson Hexagon)

- Brandwatch

- NetBase Solutions Inc.

- Meltwater (Sysomos Inc.)

- Talkwalker

- Sprout Social

- Digimind Social

- Brand24

- Hootsuite Inc.

- Khoros, LLC

- Clarabridge (now Qualtrics)

- Cision Ltd.

- Socialbakers (now Emplifi)

- Mentionlytics

- YouScan

- Pulsar Platform

- Dataminr

- Unmetric

- Awario

- Nuvi

- Adobe Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exponential Growth of Number of Social Media Users

- 4.2.2 GenAI-powered Insight Engines Driving Upsell in North America

- 4.2.3 Acceleration of In-App Social Commerce ROI Tracking

- 4.2.4 Brand-safety Metric Mandates by Global Advertisers (US and EU) Drives the Market

- 4.3 Market Restraints

- 4.3.1 Stringent Privacy Regulations Limiting Data Granularity

- 4.3.2 Analytics Skill-set Gap for Multimodal Data Interpretation Hinders the Market

- 4.3.3 Bot and Fake-traffic Distortion of Sentiment Metrics Hinders the Market

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.3 By Module

- 5.3.1 Social Media Monitoring and Tracking

- 5.3.2 Social Media Measurement/Listening and Analytics

- 5.4 By End-user Industry

- 5.4.1 Media and Entertainment

- 5.4.2 IT and Telecom

- 5.4.3 BFSI

- 5.4.4 Retail and e-Commerce

- 5.4.5 Travel and Hospitality

- 5.4.6 Healthcare and Life-sciences

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Israel

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Sprinklr

- 6.4.2 Oracle Corporation

- 6.4.3 Synthesio (Crimson Hexagon)

- 6.4.4 Brandwatch

- 6.4.5 NetBase Solutions Inc.

- 6.4.6 Meltwater (Sysomos Inc.)

- 6.4.7 Talkwalker

- 6.4.8 Sprout Social

- 6.4.9 Digimind Social

- 6.4.10 Brand24

- 6.4.11 Hootsuite Inc.

- 6.4.12 Khoros, LLC

- 6.4.13 Clarabridge (now Qualtrics)

- 6.4.14 Cision Ltd.

- 6.4.15 Socialbakers (now Emplifi)

- 6.4.16 Mentionlytics

- 6.4.17 YouScan

- 6.4.18 Pulsar Platform

- 6.4.19 Dataminr

- 6.4.20 Unmetric

- 6.4.21 Awario

- 6.4.22 Nuvi

- 6.4.23 Adobe Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment