PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851452

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851452

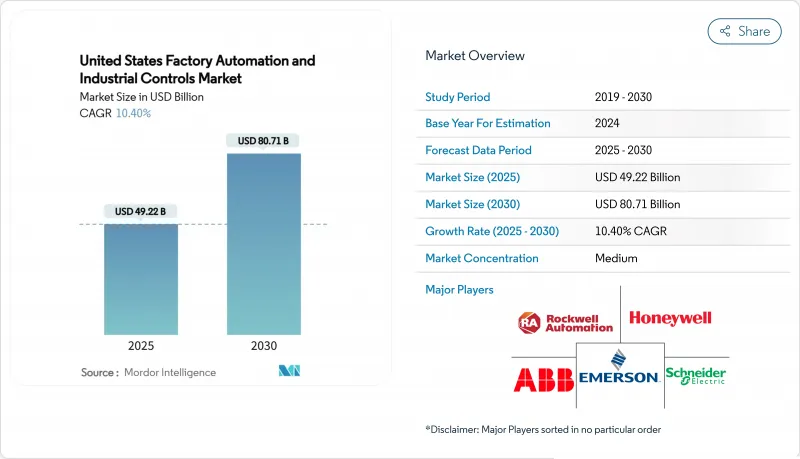

United States Factory Automation And Industrial Controls - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The United States factory automation and industrial controls market reached USD 49.22 billion in 2025 and is forecast to climb to USD 80.71 billion by 2030, advancing at a 10.40% CAGR.

The projected growth reflects a manufacturing pivot toward smart production lines that offset labor shortages, comply with stricter safety rules, and capture reshoring incentives delivered through the CHIPS Act and Inflation Reduction Act. Semiconductor fabs, battery plants, and clean-energy component makers lead new capital expenditure, while brownfield sites race to retrofit programmable logic controllers (PLCs), machine-vision systems, and industrial IoT sensors for real-time optimization. Hardware continues to dominate spending, yet service-led contracts that bundle cybersecurity, predictive maintenance, and performance guarantees are gaining momentum as manufacturers pursue outcome-based agreements. Heightened cyber-risk and tariff uncertainty remain hurdles, but the overall investment thesis is reinforced by state and federal policy alignment that rewards domestic, digitally enabled production.

United States Factory Automation And Industrial Controls Market Trends and Insights

Reshoring incentives & CHIPS Act accelerate semiconductor factory automation

The CHIPS and Science Act has triggered the largest wave of domestic semiconductor investment on record, with multibillion-dollar fabs in Arizona, Texas, and Ohio specifying ultra-clean robotics, nanometer-precision motion systems, and automated material handling that minimize particle contamination. Every USD 1 billion allocated to chip fabrication typically pulls USD 200-300 million of automation spend, magnifying demand for high-speed wafer transfer robots, machine-learning-driven process control, and safety-integrated PLC platforms. State-level abatements further shift large projects toward the South and Mountain West, where purpose-built greenfield sites can adopt fully digital, lights-out manufacturing cells from day one. Suppliers that bundle hardware, MES software, and lifecycle services gain a competitive edge as fab owners seek turnkey solutions that shorten qualification cycles and protect sensitive.

Labor shortage drives collaborative robotics adoption

Manufacturing payrolls face a 750,000-person gap today and risk 2.1 million unfilled roles by 2030, pressing management teams to deploy collaborative robots (cobots) that assume monotonous, high-repetition tasks while up-skilling employees into quality, maintenance, and data-analytics positions. Surveys show 57% of plants report that robots augment rather than eliminate human jobs, reinforcing adoption even in unionized facilities. Automotive assemblers are first movers, but small and midsize job shops follow suit as plug-and-play cobots drop in price and gain no-code programming interfaces. Federal and state training grants amplify the trend by covering tuition for certificate programs in robot operation and safety, accelerating labor-technology convergence.

Legacy OT interoperability challenges in diverse U.S. brownfield facilities

Plants built across several industrial revolutions run a patchwork of proprietary protocols, making seamless data flow difficult. Integrators often confront PLCs installed before Y2K with no native Ethernet interface, forcing custom drivers that inflate project cost and risk. Open-architecture movements such as OPC UA over TSN aim to standardize connectivity, but progress is slower than software vendors predict because downtime windows remain narrow and capital budgets are stretched. Collaborative initiatives involving automation majors and component suppliers have begun to release pre-certified interoperability bundles, yet many small firms still delay projects until clearer return on investment emerges

Other drivers and restraints analyzed in the detailed report include:

- Clean-energy manufacturing boost from Inflation Reduction Act

- OSHA-enforced machine-safety compliance raises demand for safety-integrated control systems

- Cyber-security risks in connected control systems hinder deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware accounted for 72% spending in 2024 as manufacturers purchased robots, drives, sensors, and HMIs to digitalize production lines. The United States factory automation and industrial controls market size for hardware is projected to post mid-single-digit growth while services expand faster, signaling a transition toward subscription-based support, remote condition monitoring, and performance guarantees. Leading suppliers bundle software licenses, cybersecurity management, and workforce training into multi-year agreements that stabilize revenue and align incentives with customer output. Software platforms bridge field data to MES and cloud analytics, enabling closed-loop optimization that lowers scrap and energy intensity. The hardware layer thus remains indispensable, yet value capture is migrating to integrators and OEMs that orchestrate devices, data, and domain expertise into measurable outcomes.

The services segment's 12.8% CAGR reflects manufacturer preference for predictable operating expenditure over upfront capital outlay. As-a-service robotic welding cells, vision-as-a-service inspection, and security-as-a-service packages resonate with tier-one automotive and consumer packaged goods firms seeking to hedge technology obsolescence. Vendors that co-locate remote operations centers provide 24/7 support and real-time insight, shortening mean time to repair and driving continuous improvement cycles without inflating headcount. Such models unlock new margin pools and differentiate suppliers in a crowded hardware market.

United States Factory Automation and Industrial Controls Market Report is Segmented by Component (Hardware, Software, and More), Type (Industrial Control Systems and Field Devices), and End-User Industry (Oil and Gas, Metals and Mining, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Rockwell Automation Inc.

- Siemens AG

- Schneider Electric SE

- Emerson Electric Co.

- ABB Ltd

- Mitsubishi Electric Corporation

- Honeywell International Inc.

- Omron Corporation

- Yokogawa Electric Corporation

- Fanuc Corporation

- Bosch Rexroth AG

- KUKA AG

- Kawasaki Heavy Industries Ltd.

- Beckhoff Automation GmbH and Co. KG

- GE Vernova (GE Automation and Controls)

- Keyence Corporation

- Danfoss Drives A/S

- Parker Hannifin Corporation

- Yaskawa Electric Corporation

- Banner Engineering Corp.

- Advantech Co.

- Cognex Corporation

- Delta Electronics

- Hitachi Industrial Equipment Systems Co.

- BandR Industrial Automation GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Reshoring Incentives and CHIPS Act Accelerating Semiconductor Factory Automation in the U.S.

- 4.2.2 Labor Shortage Driving Collaborative Robotics Adoption Across U.S. Manufacturing

- 4.2.3 Clean-Energy Manufacturing Boost from Inflation Reduction Act Stimulating Advanced Automation Investments

- 4.2.4 OSHA-Enforced Machine-Safety Compliance Elevating Demand for Safety-Integrated Control Systems

- 4.2.5 Brownfield IIoT Retrofits for Real-Time OEE Optimization Among U.S. OEM Supplier Network

- 4.2.6 EV Production Expansion Necessitating Flexible High-Speed Assembly Automation Lines

- 4.3 Market Restraints

- 4.3.1 Legacy OT Interoperability Challenges in Diverse U.S. Brownfield Facilities

- 4.3.2 High Initial CapEx Limiting Adoption by Mid-Sized U.S. Manufacturers Despite Tax Credits

- 4.3.3 Cyber-Security Risks in Connected Control Systems Hindering Deployment

- 4.3.4 Trade Policy Volatility Impacting Supply of Critical Automation Components

- 4.4 Value / Supply-Chain Analysis

- 4.5 Industry Policies and Regulations

- 4.6 Regulatory or Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

- 4.9 Key Case Studies and Implementation Scenarios

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Type

- 5.2.1 Industrial Control Systems

- 5.2.1.1 Distributed Control System (DCS)

- 5.2.1.2 Programmable Logic Controller (PLC)

- 5.2.1.3 Supervisory Control and Data Acquisition (SCADA)

- 5.2.1.4 Product Lifecycle Management (PLM)

- 5.2.1.5 Manufacturing Execution System (MES)

- 5.2.1.6 Human Machine Interface (HMI)

- 5.2.1.7 Other Industrial Control Systems

- 5.2.2 Field Devices

- 5.2.2.1 Machine Vision

- 5.2.2.2 Industrial Robotics

- 5.2.2.3 Motors and Drives

- 5.2.2.4 Safety Systems

- 5.2.2.5 Sensors and Transmitters

- 5.2.2.6 Other Field Devices

- 5.2.1 Industrial Control Systems

- 5.3 By End-user Industry

- 5.3.1 Oil and Gas

- 5.3.2 Chemical and Petrochemical

- 5.3.3 Power and Utilities

- 5.3.4 Food and Beverage

- 5.3.5 Automotive and Transportation

- 5.3.6 Pharmaceutical

- 5.3.7 Semiconductor and Electronics

- 5.3.8 Metals and Mining

- 5.3.9 Pulp and Paper

- 5.3.10 Other End-user Industries

- 5.4 By Region (United States)

- 5.4.1 Northeast U.S.

- 5.4.2 Midwest U.S.

- 5.4.3 South U.S.

- 5.4.4 West U.S.

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Rockwell Automation Inc.

- 6.4.2 Siemens AG

- 6.4.3 Schneider Electric SE

- 6.4.4 Emerson Electric Co.

- 6.4.5 ABB Ltd

- 6.4.6 Mitsubishi Electric Corporation

- 6.4.7 Honeywell International Inc.

- 6.4.8 Omron Corporation

- 6.4.9 Yokogawa Electric Corporation

- 6.4.10 Fanuc Corporation

- 6.4.11 Bosch Rexroth AG

- 6.4.12 KUKA AG

- 6.4.13 Kawasaki Heavy Industries Ltd.

- 6.4.14 Beckhoff Automation GmbH and Co. KG

- 6.4.15 GE Vernova (GE Automation and Controls)

- 6.4.16 Keyence Corporation

- 6.4.17 Danfoss Drives A/S

- 6.4.18 Parker Hannifin Corporation

- 6.4.19 Yaskawa Electric Corporation

- 6.4.20 Banner Engineering Corp.

- 6.4.21 Advantech Co.

- 6.4.22 Cognex Corporation

- 6.4.23 Delta Electronics

- 6.4.24 Hitachi Industrial Equipment Systems Co.

- 6.4.25 BandR Industrial Automation GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment