PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851455

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851455

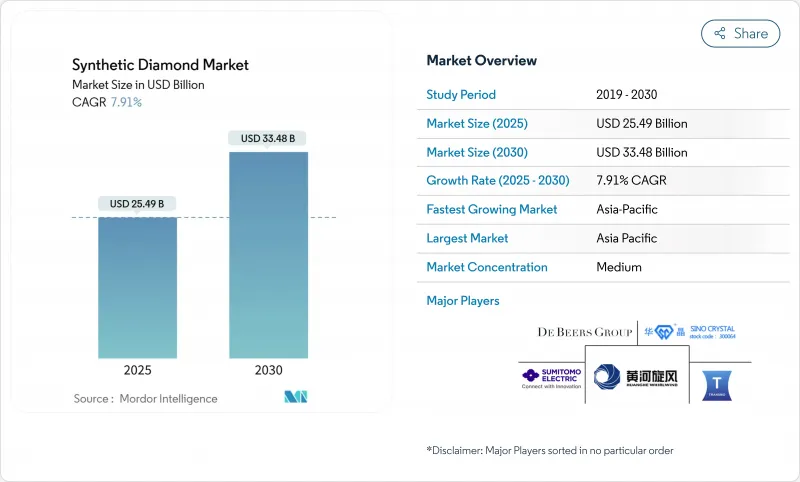

Synthetic Diamond - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Synthetic Diamond Market size is estimated at USD 25.49 billion in 2025, and is expected to reach USD 33.48 billion by 2030, at a CAGR of 7.91% during the forecast period (2025-2030).

Escalating demand from telecommunications, electric vehicles, aerospace, and high-precision manufacturing is accelerating revenue streams, while persistent sustainability mandates are steering customers away from mined stones toward engineered alternatives. Asia Pacific, already supplying most diamond wafers and super-abrasive tools, benefits from generous state incentives and surging electronics exports. Competition is intensifying because technology-focused entrants are scaling Chemical Vapor Deposition (CVD) capacity that can achieve device-grade purity, posing a direct challenge to the incumbent High Pressure High Temperature (HPHT) model. Meanwhile, luxury brands in the Gulf Cooperation Council are leveraging fancy-color lab-grown stones to satisfy environmentally conscious consumers, widening the addressable base beyond traditional bridal jewelry. Regulatory uncertainty and uneven certification standards remain the chief headwinds, especially as retail price corrections undermine perceived resale value among end users, but the performance-driven high-tech arena continues to shield margins.

Global Synthetic Diamond Market Trends and Insights

Rising Adoption of CVD Diamonds for 5G/6G RF Filters in Asia

CVD single-crystal wafers dissipate heat at 22 W/cm*K, enabling smaller and more reliable radio-frequency filters that underpin dense 5G and future 6G networks. Large-area substrate work sponsored by DARPA is migrating into commercial foundries, particularly in China, South Korea, and Taiwan, where vertically integrated OEMs are embedding diamond die-attach layers inside massive multiple-input multiple-output (mMIMO) antennas. Local equipment vendors report lower power consumption and longer base-station lifetimes, giving operators measurable total-cost-of-ownership gains.

Industrial Diamond Demand Surge from EV Battery Gigafactories

Precision grinding wheels with polycrystalline diamond coatings are indispensable for cutting silicon-rich anodes, laser-scribing separator films, and surfacing aluminum casings. Giga-scale battery plants in the United States and Europe now specify diamond tooling in over 70% of high-speed machining stations, elevating unit consumption per vehicle platform. Diamond Foundry's wafer-based inverter, six times smaller than the incumbent design yet more powerful, underscores how thermal and electrical properties improve drivetrain efficiency.

Regulatory and Certification Challenges

The Central Consumer Protection Authority in India requires retailers to specify production origin and growth method on invoices and marketing collateral, adding compliance costs and compelling supply-chain transparency. In the United States, Jewelers Vigilance Committee guidelines similarly tighten audit obligations, prompting firms to invest in spectroscopy and automated screening equipment. Divergent rules by region complicate cross-border trading and create legal exposure for distributors.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Super-Abrasives

- Luxury Brands' Sustainability Pivot to Lab-Grown Fancy-Color Stones in the GCC

- Consumer Confusion Over Lab-Grown Diamond Price Depreciation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rough stones captured 66% of the synthetic diamond market share in 2024, owing to heavy uptake in construction, oil-and-gas drilling, and precision cutting tools, all of which leverage unmatched hardness and thermal conductivity. The U.S. Geological Survey recorded domestic output of 160 million carats valued at USD 53 million, a 5% rise on the prior year.

Polished stones, though smaller in tonnage, are the fastest-expanding category at a projected 9.84% CAGR. Wider consumer acceptance, heightened design flexibility, and advances in plasma post-processing that enhance color saturation are boosting volumes across mid-tier jewelry chains. The Gemological Institute of America notes that CVD submissions now exceed HPHT samples, with fancy colors and 3-carat-plus stones up sharply year over year. Over the forecast horizon, polished gems are expected to secure incremental shelf space in omnichannel retail, even as wholesale prices stabilize.

The Synthetic Diamond Market Report Segments the Industry by Product Type (Polished and Rough), Manufacturing Process (High Pressure, High Temperature (HPHT) and Chemical Vapor Deposition (CVD)), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific anchored 56% of global revenue in 2024 and continues to post the fastest regional growth at an 8.35% CAGR through 2030. Production clusters in Henan, Shandong, and Gujarat host vertically integrated operations that span seed synthesis to finished jewelry. China's dominance in lab reactors provides cost advantages, while India's abolition of a 5% import duty on diamond seeds attracts overseas joint ventures.

North America remains pivotal for high-performance applications, particularly in quantum sensing and wide-band-gap power electronics. Adamas One Corp's South Carolina facility, which currently runs 12 reactors producing 3,000 rough carats monthly, emphasizes IP-protected growth protocols to secure aerospace and medical contracts.

Europe maintains a stable but innovation-oriented stance. German toolmakers and French photonics startups incorporate diamond inserts to meet automotive lightweighting mandates. The United Kingdom's academic ecosystem, notably the National Quantum Computing Centre, advances Nitrogen-Vacancy (NV) defect engineering for secure communications. Outside Europe, the Middle East positions Dubai as a trading and production hub.

- ADAMAS ONE

- Applied Diamond Inc.

- Coherent Corp.

- De Beers Group (Element Six)

- Diamond Foundry

- Henan Huanghe Whirlwind CO.,Ltd.

- Heyaru Group

- ILJIN DIAMOND CO., LTD.

- John Crane (Advanced Diamond Technologies, Inc.)

- NEW DIAMOND TECHNOLOGY LLC

- PURE LAB DIAMONDS

- Sandvik AB

- Sumitomo Electric Industries, Ltd.

- Swarovski AG

- Tecdia, Inc.

- Washington Diamond

- Zhengzhou Sino-Crystal Diamond Co.,Ltd.

- Zhuhai Zhong Na Diamond Co.,Ltd Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of CVD Diamonds for 5G/6G RF Filters Asia

- 4.2.2 Industrial Diamond Demand Surge from EV Battery Gigafactories

- 4.2.3 Growing Demand for Super Abrasives

- 4.2.4 Super-abrasive Usage in Automated CNC Machining for Aerospace Composites

- 4.2.5 Luxury Brands' Sustainability Pivot to Lab-Grown Fancy-Color Stones in the GCC

- 4.3 Market Restraints

- 4.3.1 Regulatory and Certification Challenges

- 4.3.2 Complex Manufacturing Process

- 4.3.3 Consumer Confusion Over LGD Price Depreciation vs. Natural Diamonds

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Product Type

- 5.1.1 Polished

- 5.1.1.1 Jewelry

- 5.1.1.2 Electronics

- 5.1.1.3 Healthcare

- 5.1.1.4 Other Polished Types

- 5.1.2 Rough

- 5.1.2.1 Construction

- 5.1.2.2 Mining

- 5.1.2.3 Oil and Gas

- 5.1.2.4 Other Rough Types

- 5.1.1 Polished

- 5.2 By Manufacturing Process

- 5.2.1 High Pressure High Temperature (HPHT)

- 5.2.2 Chemical Vapor Deposition (CVD)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordics

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ADAMAS ONE

- 6.4.2 Applied Diamond Inc.

- 6.4.3 Coherent Corp.

- 6.4.4 De Beers Group (Element Six)

- 6.4.5 Diamond Foundry

- 6.4.6 Henan Huanghe Whirlwind CO.,Ltd.

- 6.4.7 Heyaru Group

- 6.4.8 ILJIN DIAMOND CO., LTD.

- 6.4.9 John Crane (Advanced Diamond Technologies, Inc.)

- 6.4.10 NEW DIAMOND TECHNOLOGY LLC

- 6.4.11 PURE LAB DIAMONDS

- 6.4.12 Sandvik AB

- 6.4.13 Sumitomo Electric Industries, Ltd.

- 6.4.14 Swarovski AG

- 6.4.15 Tecdia, Inc.

- 6.4.16 Washington Diamond

- 6.4.17 Zhengzhou Sino-Crystal Diamond Co.,Ltd.

- 6.4.18 Zhuhai Zhong Na Diamond Co.,Ltd Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Applications in Orthopedic Medical Devices