PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851456

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851456

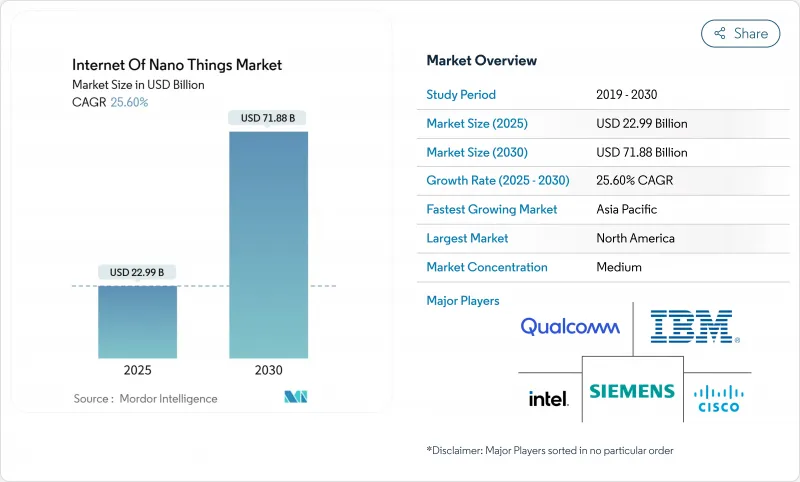

Internet Of Nano Things - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Internet of Nano Things Market size is estimated at USD 22.99 billion in 2025, and is expected to reach USD 71.88 billion by 2030, at a CAGR of 25.60% during the forecast period (2025-2030).

The surge reflects the commercialisation of terahertz-band nano-antenna designs, the roll-out of ultra-low power carbon-nanotube sensors, and the rapid convergence of nanoscale communication protocols with mainstream wireless networks. Governments are funding pandemic surveillance frameworks built on nanosensors, while private investment is accelerating AI-driven orchestration platforms that translate molecular-level data into actionable insight. Hardware continues to account for almost half of all spending, but software platforms are expanding at a markedly faster pace as enterprises prioritise analytics over devices. Regionally, North America leads on account of federal research grants and early terahertz spectrum allocation, yet Asia-Pacific exhibits the strongest growth as semiconductor hubs embed nanosensor networks into Industry 4.0 roadmaps. Competitive pressure is intensifying as semiconductor majors leverage existing fabs while start-ups introduce disruptive molecular communication stacks, but steep fabrication costs and fragmented spectrum policies remain notable headwinds.

Global Internet Of Nano Things Market Trends and Insights

Rapid Advancements in Nanotechnology Enabling Ultra-Low Power Sensors

Carbon-nanotube-based devices now harvest ambient energy, removing conventional battery constraints and slashing maintenance cycles. MIT engineers demonstrated plant-powered nanosensors that self-energize through photosynthesis, validating energy autonomy for remote deployments. Boron nitride nanotube fibres provide heat-tolerant networks that withstand harsh industrial settings without degradation. Coupled with AI-accelerated materials discovery, exemplified by Materials Nexus' rare-earth-free permanent magnet breakthrough, innovation cycles have shrunk from years to months. These advances unlock applications ranging from precision agriculture to hazardous-environment monitoring, underpinning the long-term growth of the Internet of Nano Things market.

Growing Demand for Real-Time Health Monitoring Wearables

FDA clearance of Nanowear's nanosensor cardiac patch underscores regulatory validation for nano-enabled medical devices. Continuous glucose monitors built on carbon-nanotube films now rival laboratory accuracy while retaining discreet, skin-patch form factors. Multi-analyte patches track electrolytes, lactate, and cortisol simultaneously, supporting preventive care models that lower chronic-disease costs. Hospitals integrating these devices report earlier sepsis detection and shorter ICU stays, reinforcing healthcare's contribution to the Internet of Nano Things market expansion. The sector's 30.3% revenue share in 2024 signals entrenched demand that other verticals must challenge.

Severe Data Security and Privacy Risks at Nanoscale

Nanosensors lack the compute headroom for traditional encryption, exposing attack surfaces that could compromise hospital, factory, or municipal networks. Implantable medical nanosensors are especially vulnerable; a hijacked glucose monitor can falsify readings, endangering patients. GDPR treats nanosensor data as high-risk, mandating explicit consent that is difficult to implement on autonomous sub-millimetre devices. Quantum-resistant lightweight ciphers remain at proof-of-concept stages, widening the security gap and exerting a negative 4.3% pull on forecast CAGR for the Internet of Nano Things market.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption of Industry 4.0 and Smart Manufacturing

- Proliferation of 5G/6G and Edge Computing Infrastructure

- High Capital Costs and Complexity of Nano-Fabrication

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware generated 47.6% of 2024 revenue, anchoring the Internet of Nano Things market in essential physical devices, antennas, and gateways. Yet the software segment is racing ahead at a 28.6% CAGR as analytics platforms capitalise on torrents of molecular data. Services remain nascent but record double-digit growth because enterprises require consulting expertise to integrate nano-devices with legacy systems. Dow's collaboration with Carbice on thermal interface materials shows how specialised know-how is turning into high-margin service lines.

The software boom is redefining value capture: hardware margins compress as commoditisation sets in, while orchestration stacks that manage billions of endpoints command premium licences. Cloud vendors embed nano-device APIs, drawing developers into unified platforms that bundle security, AI, and lifecycle management. Over the forecast horizon, the Internet of Nano Things market size linked to software revenues is projected to narrow the gap on hardware, recalibrating competitive strategies across the ecosystem.

Healthcare contributed 30.3% of 2024 revenue and remains the largest adopter, leveraging nanosensors for continuous vitals monitoring, implant surveillance, and smart drug delivery. Smart-city programmes, however, will expand at 27.6% CAGR to 2030 as municipalities deploy nanosensor meshes for air-quality analytics, water-leak detection, and intelligent traffic control. In manufacturing, nanosensors embedded on production lines feed real-time molecular data into predictive-maintenance engines, while logistics firms fit nanosensors inside containers to verify cold-chain compliance.

Environmental agencies adopt nanosensor buoys that detect pollutants at parts-per-billion resolution, a capability classical sensors lack. Agriculture outfits scatter plant-tissue nanosensors that signal nutrient deficits early, cutting fertiliser usage and water waste. These deployments illustrate how vertical diversification is accelerating overall Internet of Nano Things market penetration across the real economy.

Internet of Nano Things Market is Segmented by Component (Hardware, Software, and Services), End-User (Healthcare, Logistics and Transportation, Defense and Aerospace, Manufacturing, and More), Communication Technology (Electromagnetic, Molecular Communication, Nano RFID/NFC, and More), Deployment Model (On-Premise, Cloud, and Hybrid), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 38.6% revenue share in 2024, buoyed by federal grants, early terahertz spectrum allocation, and entrenched semiconductor fabs capable of nano-class production. The NIST IoT Advisory Board provides clarity around standards, accelerating commercial pilots. However, high labour costs and capital outlays squeeze margins, and the talent pipeline struggles to supply nano-manufacturing technicians. The United States focuses on defence, aerospace, and advanced healthcare implants, while Canada channels resources into environmental monitoring for natural-resource stewardship.

Asia-Pacific will post a 28.1% CAGR to 2030, reflecting aggressive Industry 4.0 incentives, deep electronics supply chains, and expansive 5G footprints. China drives manufacturing uptake, embedding nanosensors inside fabs and chemical plants to boost yield and safety, while Japan's med-tech firms pioneer bio-compatible nano implants. South Korea exploits telecom leadership to pilot 6G-ready nano-mesh networks. Regional governments subsidise nano R&D, compressing time-to-market and intensifying competition. The resulting scale advantages will narrow the Internet of Nano Things market size gap between Asia-Pacific and North America by decade end.

Europe remains influential, championing data privacy and sustainability frameworks that shape global norms. Horizon Europe has earmarked EUR 100 million for edge-AI and IoT research, with part allocated to nano-device interoperability. Germany deploys nanosensors in precision manufacturing, and the United Kingdom tests graphene-based health patches. Emerging regions in South America and the Middle East, and Africa invest selectively in environmental and infrastructure monitoring, capitalising on nanosensors' ability to deliver high granularity at lower lifecycle costs.

- IBM Corporation

- Intel Corporation

- Cisco Systems, Inc.

- Qualcomm Technologies, Inc.

- Siemens AG

- Schneider Electric SE

- SAP SE

- Juniper Networks, Inc.

- Nokia Corporation

- Honeywell International Inc.

- Analog Devices, Inc.

- STMicroelectronics N.V.

- Nanoscale Components, Inc.

- NanoSensors, Inc.

- Agilent Technologies, Inc.

- TeraSense Group, Inc.

- Graphenea, Inc.

- Litmus Automation, Inc.

- ON Semiconductor Corporation

- Microchip Technology Inc.

- Camtek Ltd.

- NeuraLace Medical, Inc.

- Nanolike SAS

- Ambiq Micro, Inc.

- Synapse Wireless, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid advancements in nanotechnology enabling ultra-low power sensors

- 4.2.2 Growing demand for real-time health monitoring wearables

- 4.2.3 Increasing adoption of Industry 4.0 and smart manufacturing

- 4.2.4 Proliferation of 5G/6G and edge computing infrastructure

- 4.2.5 Emerging terahertz-band nano-antenna breakthroughs reducing signal attenuation

- 4.2.6 Government-funded pandemic surveillance networks leveraging nanosensors

- 4.3 Market Restraints

- 4.3.1 Severe data security and privacy risks at nanoscale

- 4.3.2 High capital costs and complexity of nano-fabrication

- 4.3.3 Biocompatibility and long-term cytotoxicity concerns in human body deployments

- 4.3.4 Lack of standardized terahertz spectrum regulations causing deployment delays

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By End-user

- 5.2.1 Healthcare

- 5.2.2 Logistics and Transportation

- 5.2.3 Defense and Aerospace

- 5.2.4 Manufacturing

- 5.2.5 Energy and Power

- 5.2.6 Environmental Monitoring

- 5.2.7 Retail

- 5.2.8 Agriculture

- 5.2.9 Smart Cities and Infrastructure

- 5.2.10 Other End-users

- 5.3 By Communication Technology

- 5.3.1 Electromagnetic

- 5.3.2 Molecular Communication

- 5.3.3 Nano RFID/NFC

- 5.3.4 Nano Sensor Networks

- 5.3.5 Nano Satellite Communication

- 5.3.6 Others

- 5.4 By Deployment Model

- 5.4.1 On-Premise

- 5.4.2 Cloud

- 5.4.3 Hybrid

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Singapore

- 5.5.4.6 Malaysia

- 5.5.4.7 Australia

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Intel Corporation

- 6.4.3 Cisco Systems, Inc.

- 6.4.4 Qualcomm Technologies, Inc.

- 6.4.5 Siemens AG

- 6.4.6 Schneider Electric SE

- 6.4.7 SAP SE

- 6.4.8 Juniper Networks, Inc.

- 6.4.9 Nokia Corporation

- 6.4.10 Honeywell International Inc.

- 6.4.11 Analog Devices, Inc.

- 6.4.12 STMicroelectronics N.V.

- 6.4.13 Nanoscale Components, Inc.

- 6.4.14 NanoSensors, Inc.

- 6.4.15 Agilent Technologies, Inc.

- 6.4.16 TeraSense Group, Inc.

- 6.4.17 Graphenea, Inc.

- 6.4.18 Litmus Automation, Inc.

- 6.4.19 ON Semiconductor Corporation

- 6.4.20 Microchip Technology Inc.

- 6.4.21 Camtek Ltd.

- 6.4.22 NeuraLace Medical, Inc.

- 6.4.23 Nanolike SAS

- 6.4.24 Ambiq Micro, Inc.

- 6.4.25 Synapse Wireless, Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 8.1 White-Space and Unmet-Need Assessment