PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851459

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851459

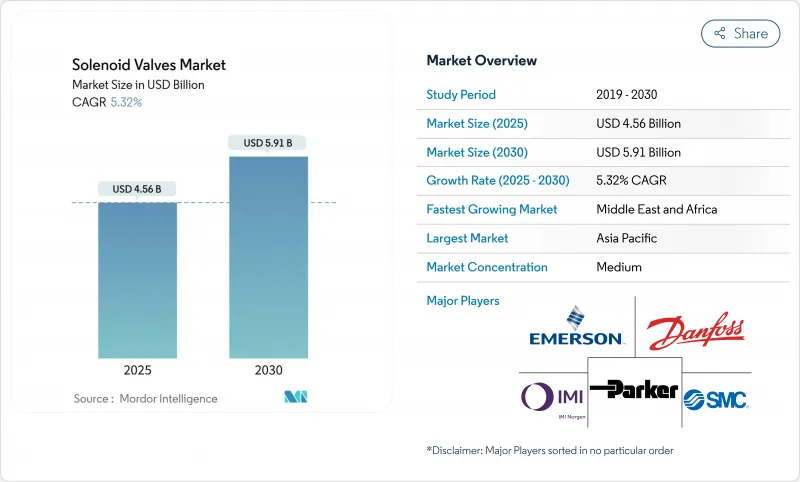

Solenoid Valves - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The solenoid valves market size is valued at USD 4.56 billion in 2025 and is forecast to reach USD 5.91 billion by 2030, reflecting a 5.32% CAGR over the period.

Demand stems from automation projects in water reuse, shale-gas wellheads, hydrogen electrolyzers, and compact electric-vehicle (EV) thermal loops. Asia-Pacific retains volume leadership, while the Middle East and Africa exhibits the fastest expansion because of economic diversification programs. Technology differentiation is shifting toward zero-emissions actuation, IO-Link-enabled diagnostics, and lightweight engineering plastics that satisfy automotive range targets. Despite growing price competition from low-cost Asian producers and alloy cost swings, OEMs continue to prioritize smart, service-friendly solenoid architectures that limit downtime and enable predictive maintenance.

Global Solenoid Valves Market Trends and Insights

Expansion of Industrial Waste-water Re-use Schemes in EU & GCC

Circular-economy directives in the European Union and water-scarcity mandates in the Gulf Cooperation Council are accelerating investments in advanced treatment plants that need automated chemical dosing, back-flush control, and stage switching. Solenoid valves enable precise, low-leak actuation that manual devices cannot match, especially when treatment recipes shift with feed-water variability. Oil producers adopting zero-liquid-discharge plants in the Middle East prefer stainless-steel or duplex bodies coupled with digital position feedback to meet environmental audits.

Surge in Compact EV Thermal-Management Loops Requiring Micro-Solenoids

Battery cooling, power-electronics chillers, and cabin HVAC in next-generation EVs integrate multi-loop circuits that depend on fast, energy-efficient micro-solenoids. Suppliers such as Sanhua Automotive have commercialized refrigerant versions able to cycle millions of times while operating inside constrained battery packs. Lightweight PEEK bodies and low-power coils extend driving range, making the segment a core growth engine for the solenoid valves market.

High Switching-Cycle Fatigue in >120 °C Applications

Steam lines and high-temperature reactors expose solenoid coils to accelerated insulation breakdown. Premium high-temp copper windings and perfluoro-elastomer seals are available but raise bill-of-material cost, curbing adoption in price-sensitive projects. Utilities facing extended maintenance intervals perceive risk in swapping to higher-density windings, moderating growth for the solenoid valves market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Retrofit of Legacy Beverage Lines in ASEAN for Hygienic Design

- Gas Well-Head Automation in Shale Basins of US & Argentina

- Price Volatility of Specialty Alloys (e.g., Duplex Stainless)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct-acting valves led the solenoid valves market with 42% share in 2024, translating to an estimated USD 1.9 billion of 2025 revenue. Their simple architecture, minimal pressure drop, and fast cycling suit utilities water lines and OEM machinery. Yet pilot-operated mechanisms, advancing at 6.9% CAGR, increasingly service wellheads, power boilers, and large chemical reactors that require ports above 25 mm and pressures exceeding 100 bar. Emerson's shale-gas solution highlights the shift, pairing a minute electromagnetic pilot with a piston diaphragm able to pass thousands of standard cubic meters per hour. Industries upgrading to predictive maintenance platforms value the lower inrush current and quieter closing profile typical of pilot-operated units.

The move alters supply-chain needs: coils must tolerate fluctuating upstream pressures, diaphragms demand abrasion-resistant elastomers, and housings often integrate threaded sensors that feed PLCs. Asian fabricators now replicate classic pilot-operated geometries at scale, intensifying price pressure but also expanding availability across emerging economies, thereby broadening the solenoid valves market.

Two-way shut-off valves remain the workhorse, holding 55% revenue in 2024, roughly USD 2.3 billion of solenoid valves market size. They dominate irrigation, compressed-air, and basic process isolation. However, as food, beverage, and biotech adopters demand rapid SKU changeovers, three-way diverter designs grow 6.4% annually. These valves alternate between production, CIP, and sterilization streams without manual spool changes, aligning with hygienic directives. Certain pharmaceutical skids now bundle twenty or more three-way units on a single digital manifold, trimming footprint by 30% and slashing install time.

Manufacturers respond with cavity-free internals and FDA-approved seals that eliminate dead legs where contaminants accumulate. Control software maps each port to PLC tags, enabling recipe-driven flow paths. Multi-port innovations bleed into semiconductor wet benches, where chemistries must route through multiple rinse and etch tanks in milliseconds, reinforcing three-way adoption across the solenoid valves market.

The Solenoid Valves Market Report is Segmented by Operating Principle (Direct-Acting, Pilot-Operated), Port Configuration (Two-Way, Three-Way, and Four-Way), Material (Brass, Steel, Aluminum, and Plastics), Size (Micro, Sub, Mini, Small, and Large), End-User (Food, Automotive, Chemical, Oil and Gas, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific, home to 34% of 2024 revenue, leverages China's vast electronics output, Japan's precision robotics, and India's expanding pharma exports. Governments supporting domestic semiconductor fabs and battery plants fuel manifold adoption, while hydrogen pilot corridors in Japan and Korea demand high-integrity valves able to tolerate 700 bar gaseous service. Additionally, rising water-reuse mandates in coastal Chinese provinces add fresh municipal demand.

The Middle East and Africa, posting a projected 7.50% CAGR, benefits from Vision 2030 diversification projects in Saudi Arabia and petrochemical mega-sites in the UAE. Hydrogen-ammonia export plans from Oman and Saudi NEOM require specialized pilot-operated valves compatible with cryogenic and high-pressure duty. African growth centers on South African mining dewatering and Egyptian food-processing expansion, driving moderate yet diverse uptake.

North America contributes steady aftermarket turnover in shale gas, LNG, and pharma. The rapid rollout of zero-emissions wellhead valves across Colorado and Texas showcases regulatory-driven capex that refreshes installed bases. In Canada, carbon-capture demonstration plants call for corrosion-proof solenoids handling CO2 mixed streams. Europe, a mature yet innovation-led region, pivots to green hydrogen and digitalized manufacturing. That pivot secures value for smart IO-Link-ready valves despite slower headline growth, anchoring premium price bands within the solenoid valves market.

- Emerson Electric Co. (ASCO)

- Danfoss A/S

- Parker-Hannifin Corp.

- SMC Corp.

- IMI plc

- Burkert GmbH and Co. KG

- Curtiss-Wright Corp.

- AirTAC International Group

- Kendrion N.V.

- The Lee Co.

- CEME S.p.A

- PeterPaul Electronics Co.

- CKD Corp.

- Anshan Solenoid Valve Co.

- KANKEO SANGYO Co.

- Rotex Automation

- Festo SE and Co. KG

- ODE S.r.l.

- GEMU Group

- Genebre S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Industrial Waste-water Re-use Schemes in EU and GCC

- 4.2.2 Surge in Compact EV Thermal-Management Loops Requiring Micro-Solenoids

- 4.2.3 Rapid Retrofit of Legacy Beverage Lines in ASEAN for Hygienic Design

- 4.2.4 Gas Well-Head Automation in Shale Basins of US and Argentina

- 4.2.5 Hydrogen Electrolyzer Build-Out in Europe and Japan

- 4.2.6 Growing Preference for Smart, IO-Link-Enabled Valves in Pharma 4.0

- 4.3 Market Restraints

- 4.3.1 High Switching-Cycle Fatigue in greater than 120 degree C Applications

- 4.3.2 Price Volatility of Specialty Alloys (e.g., Duplex SS)

- 4.3.3 Skilled Labor Shortage for Field Retro-Commissioning in LATAM

- 4.3.4 Rising Competition from Piezo-Electric Micro-Valves in Medical OEMs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Pricing Analysis (if applicable)

- 4.8 Industry Standards and Regulations

- 4.9 Technology Snapshot

- 4.9.1 Evolution of Solenoid Valves and Emerging EV / AV Uses

- 4.9.2 Major Design and Technical Considerations

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Operating Principle

- 5.1.1 Direct-Acting

- 5.1.2 Pilot-Operated

- 5.2 By Port/Flow Configuration

- 5.2.1 Two-Way

- 5.2.2 Three-Way

- 5.2.3 Four-Way and Above

- 5.3 By Valve Body Material

- 5.3.1 Brass

- 5.3.2 Stainless Steel

- 5.3.3 Aluminum

- 5.3.4 Engineering Plastics and Composites

- 5.4 By Size

- 5.4.1 Micro-Miniature (less than 5 mm)

- 5.4.2 Sub-Miniature (5-10 mm)

- 5.4.3 Miniature (10-25 mm)

- 5.4.4 Small Diaphragm (25-50 mm)

- 5.4.5 Large Diaphragm (greater than 50 mm)

- 5.5 By End-user Industry

- 5.5.1 Food and Beverage

- 5.5.1.1 Filtration Systems

- 5.5.1.2 Filling / Dosing Lines

- 5.5.2 Automotive

- 5.5.2.1 Air-Suspension

- 5.5.2.2 Fuel Injection and Emission

- 5.5.2.3 Safety and Security Systems

- 5.5.2.4 Transmission and Driveline

- 5.5.2.5 Others (HVAC, Doors)

- 5.5.3 Chemical and Petrochemical

- 5.5.3.1 Direction Control for Storage

- 5.5.3.2 Isolation Valves

- 5.5.4 Power Generation

- 5.5.4.1 Steam Control and Feeders

- 5.5.4.2 Lifts and Pumping

- 5.5.4.3 Deluge Systems

- 5.5.5 Oil and Gas

- 5.5.5.1 Drilling

- 5.5.5.2 Extraction

- 5.5.5.3 Downstream Supply

- 5.5.6 Healthcare and Pharmaceutical

- 5.5.7 Other Verticals (Agri-Tech, Aerospace, Textile, etc.)

- 5.5.1 Food and Beverage

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Israel

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 United Arab Emirates

- 5.6.4.4 Turkey

- 5.6.4.5 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JV, IP)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Emerson Electric Co. (ASCO)

- 6.4.2 Danfoss A/S

- 6.4.3 Parker-Hannifin Corp.

- 6.4.4 SMC Corp.

- 6.4.5 IMI plc

- 6.4.6 Burkert GmbH and Co. KG

- 6.4.7 Curtiss-Wright Corp.

- 6.4.8 AirTAC International Group

- 6.4.9 Kendrion N.V.

- 6.4.10 The Lee Co.

- 6.4.11 CEME S.p.A

- 6.4.12 PeterPaul Electronics Co.

- 6.4.13 CKD Corp.

- 6.4.14 Anshan Solenoid Valve Co.

- 6.4.15 KANKEO SANGYO Co.

- 6.4.16 Rotex Automation

- 6.4.17 Festo SE and Co. KG

- 6.4.18 ODE S.r.l.

- 6.4.19 GEMU Group

- 6.4.20 Genebre S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment