PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907283

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907283

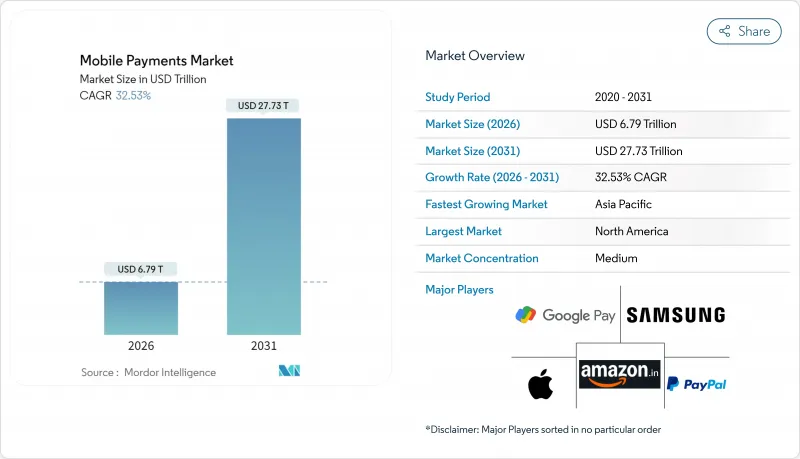

Mobile Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The mobile payments market was valued at USD 5120 billion in 2025 and estimated to grow from USD 6787.5 billion in 2026 to reach USD 27730.9 billion by 2031, at a CAGR of 32.53% during the forecast period (2026-2031).

Rapid adoption of government-backed real-time rails, subsidized merchant discount programs, and consolidation around super-app ecosystems underpin this expansion. Strong proximity payment deployment, driven by NFC transit projects, is narrowing the historical gap with remote commerce channels, while account-to-account wallets continue to compress traditional card economics. Emerging economies are leapfrogging legacy infrastructure, shifting competitive advantage toward mobile-first platforms, and fostering new revenue pools in data monetization and value-added services. Intensifying regulatory focus on instant settlement, privacy, and cross-border interoperability further reshapes business models across the mobile payments market.

Global Mobile Payments Market Trends and Insights

Explosive UPI and PIX-style real-time rails adoption

Government-sponsored instant payment systems have re-engineered settlement economics by removing intermediary fees and providing 24/7 availability, creating material cost advantages over card networks. Brazil's PIX processed 6 billion monthly transactions in 2025, with projections that 58% of e-commerce spend will use PIX within five years. India's UPI demonstrates similar scale, prompting regional replication across Thailand and other ASEAN markets. These sovereign rails localize data, strengthen monetary oversight, and accelerate the mobile payments market toward account-to-account models. Traditional processors face share erosion as emerging markets bypass legacy infrastructure.

Subsidized merchant MDRs boosting QR-code uptake

Zero-fee or heavily discounted merchant schemes in India and Indonesia dramatically reduce acceptance friction for small retailers, accelerating QR-code penetration. India earmarked INR 1,500 crore (USD 180 million) for UPI incentives in FY 2024-25, while Indonesia's QRIS applies no merchant charges on micro-transactions, driving formalization of cash-heavy sectors. As subsidies taper, policy makers plan tiered MDR regimes to ensure long-term sustainability without reversing adoption gains. The initiative enlarges addressable merchant pools and cements domestic preference for mobile-native payments, further lifting the mobile payments market.

Fragmented tokenization standards hindering cross-wallet acceptance

Inconsistent token formats force merchants to juggle multiple SDKs, elevating integration cost and checkout friction. Mastercard's pledge to eliminate manual card entry by 2030 highlights industry recognition of the issue, with 30% of its traffic already tokenized. Although bodies like the NFC Forum propose multi-purpose tap specifications, adoption remains uneven. Without alignment, cross-wallet acceptance lags, tempering growth in the mobile payments market.

Other drivers and restraints analyzed in the detailed report include:

- Super-app ecosystem lock-ins

- NFC-enabled transit projects

- High chargeback ratios in cross-border wallets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Remote transactions accounted for 64.32% of the mobile payments market in 2025, reflecting e-commerce momentum. Proximity flows, however, are forecast to advance at a 35.92% CAGR, supported by broad NFC rollout in retail and transit. The mobile payments market size for proximity channels is poised to close the gap as contactless norms spread in grocery and quick-service verticals. Unified wallet strategies now offer scan-to-buy, tap-to-ride, and in-app checkout under one interface, eroding channel distinctions and fostering omnichannel loyalty. Technology vendors emphasize edge security and token lifecycle management to ensure parity between remote and face-to-face use cases.

Increasing transit adoption illustrates proximity scaling. California registers 69% contactless penetration for debit card rides, while Singapore's cloud-connected carts integrate biometric payment paths. Continuous convergence positions the mobile payments market for blended customer journeys where context, not location, dictates the payment rail.

Person-to-merchant flows held 37.92% share in 2025, yet in-store POS volumes are projected to grow at 36.65% CAGR as retailers upgrade terminals, add softPOS, and lean on loyalty-linked taps. The mobile payments market size for in-store POS will expand as venues migrate from mag-stripe to NFC and QR, benefiting acquirers with omnichannel orchestration. Peer-to-peer transfers and emerging AI-agent purchases fill a complementary role by funneling balances back into commerce ecosystems, sustaining wallet stickiness.

Visa, Mastercard, and PayPal now prototype autonomous shopping journeys where biometric authentication triggers AI-negotiated pricing, compressing checkout steps. As automation blurs transaction categories, providers must harmonize dispute resolution and data privacy rules across retail and peer contexts, preserving confidence in the mobile payments market.

The Mobile Payments Market Report is Segmented by Payment Type (Proximity Payments, Remote Payments), Transaction Type (Peer-To-Peer (P2P), In-Store Point-Of-Sale (POS), and More), Application (Retail and ECommerce, Transportation and Logistics, and More), End-User (Personal, Business), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 38.61% share in 2025 on the strength of established card rails, extensive smartphone ownership, and robust NFC terminal coverage. Yet incremental growth moderates as saturation nears and merchants contest swipe fees that totaled USD 187.2 billion in 2024. Regulatory scrutiny, including the Credit Card Competition Act, opens space for lower-cost mobile-native options. Apple's curtailed in-app commission model following antitrust rulings creates additional channels for alternative wallets, nudging the mobile payments market toward more competitive economics.

Asia-Pacific advances at a 34.24% CAGR, propelled by mass adoption of UPI, Pix-style systems, and super-app ecosystems. China records 82% wallet penetration in e-commerce; India surpasses 50% across online and physical stores. Mobile internet penetration reached 51% of the population by 2023, and cash usage is forecast to dip to 14% by 2027. Governments leverage digital rails to deliver subsidies, further embedding wallets in daily life. Regional interoperability frameworks, such as ASEAN QR code linkage, foster cross-border merchant acceptance, widening the mobile payments market.

Europe experiences steady progress under instant payment mandates and upcoming digital euro pilots. The European Central Bank outlines offline capability requirements and high privacy standards, ensuring that any CBDC complements existing schemes. Latin America showcases rapid scale through Brazil's PIX, reaching 64 billion transactions in 2024 and preparing NFC extensions, while Colombia and Argentina deploy similar blueprints. Middle East and Africa display mixed trajectories: Gulf states spearhead smart-city payment layers, whereas AML/KYC bottlenecks slow Tier-2 African bank onboarding. AI-driven compliance vendors such as Flagright cut onboarding times by 80%, signalling future uplift for the mobile payments market.

- Alphabet (Google Pay)

- Apple Inc.

- Samsung Electronics (Samsung Pay)

- PayPal Holdings

- Amazon Pay

- Visa, Inc.

- American Express Inc.

- Mastercard

- Stripe, inc.

- Block Inc. (Square and Cash App)

- FIS (Worldpay)

- Fiserv (Clover)

- ACI Worldwide

- Adyen Inc.

- Ant Group (Alipay)

- Tencent (WeChat Pay)

- Paytm

- GrabPay

- Kakao Pay

- Mercado Pago

- MTN MoMo

- Comviva Tech.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive UPI and PIX-style Real-time Rails Adoption in APAC and LATAM

- 4.2.2 Subsidised Merchant MDRs Fueling QR-Code Uptake in India and Indonesia

- 4.2.3 Super-App' Ecosystem Lock-ins by Chinese and SE-Asian Tech Majors Drives the Market

- 4.2.4 NFC-enabled Transit Projects (e.g., MTA NYC OMNY) Accelerating Urban Proximity Spend

- 4.2.5 Interchange-free A2A Wallets (iDEAL 2.0, Brazil Pix, FedNow) Compressing Card Fees and Shifting Volumes

- 4.3 Market Restraints

- 4.3.1 Fragmented Tokenization Standards Hindering Cross-Wallet Acceptance

- 4.3.2 High Chargeback Ratios in Cross-border Wallet-funded Transactions

- 4.3.3 In-store NFC Interoperability Gaps in U.S. Dual-Tap Flows Hinders the Market

- 4.3.4 AML/KYC Friction Slowing Wallet On-boarding in Africa's Tier-2 Banks

- 4.4 Value Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Future of Mobile Payments (Cashless Evolution, Rise of Wearables, Biometrics Payments, Impact of Blockchain Technology)

- 4.8 Mobile Payments in E-Commerce (Utility of e-wallets, Digital Commerce Spending (2021 and 2025), Mobile Commerce Penetration, Future Developments, etc.)

- 4.9 Impact on Banking Industry (Investments in Mobile Technology, Bank-MNO partnership, Opportunities in Government to Person (G2P) Payments, etc.)

- 4.10 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Payment Type

- 5.1.1 Proximity Payments

- 5.1.2 Remote Payments

- 5.2 By Transaction Type

- 5.2.1 Peer-to-Peer (P2P)

- 5.2.2 In-store Point-of-Sale (POS)

- 5.2.3 Person-to-Merchant (P2M/Checkout)

- 5.2.4 Other Transaction Types

- 5.3 By Application

- 5.3.1 Retail and eCommerce

- 5.3.2 Transportation and Logistics

- 5.3.3 Hospitality and Food-Service

- 5.3.4 Government and Public Sector

- 5.3.5 Other Applications (Education, Healthcare)

- 5.4 By End-user

- 5.4.1 Personal

- 5.4.2 Business

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alphabet (Google Pay)

- 6.4.2 Apple Inc.

- 6.4.3 Samsung Electronics (Samsung Pay)

- 6.4.4 PayPal Holdings

- 6.4.5 Amazon Pay

- 6.4.6 Visa, Inc.

- 6.4.7 American Express Inc.

- 6.4.8 Mastercard

- 6.4.9 Stripe, inc.

- 6.4.10 Block Inc. (Square and Cash App)

- 6.4.11 FIS (Worldpay)

- 6.4.12 Fiserv (Clover)

- 6.4.13 ACI Worldwide

- 6.4.14 Adyen Inc.

- 6.4.15 Ant Group (Alipay)

- 6.4.16 Tencent (WeChat Pay)

- 6.4.17 Paytm

- 6.4.18 GrabPay

- 6.4.19 Kakao Pay

- 6.4.20 Mercado Pago

- 6.4.21 MTN MoMo

- 6.4.22 Comviva Tech.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment