PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907305

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907305

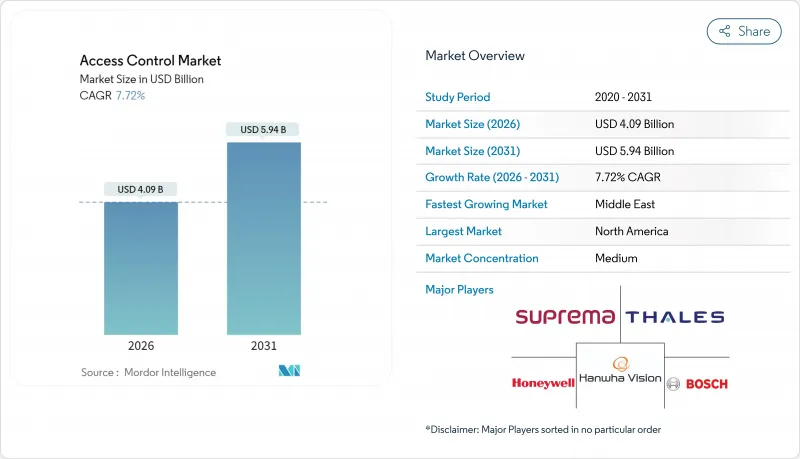

Access Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The access control market size in 2026 is estimated at USD 4.09 billion, growing from 2025 value of USD 3.80 billion with 2031 projections showing USD 5.94 billion, growing at 7.72% CAGR over 2026-2031.

Demand is intensifying as cloud management, mobile credentials and biometrics replace legacy keys and cards across corporate, public-sector and critical-infrastructure facilities. Stricter data-protection regulations, the premium placed on contactless user experiences and convergence with video surveillance are reinforcing the upgrade cycle. Price escalations linked to semiconductor shortages are nudging buyers toward software-defined architectures that future-proof capital expenditure while mitigating supply-chain risk.

Global Access Control Market Trends and Insights

Regulatory Mandates for Electronic Access in GDPR-Sensitive EU Data Centers

The NIS2 directive, effective October 2024, requires multi-factor authentication and tamper-resistant audit trails across every physical entry point. Data-center operators are accelerating migration from legacy cards to biometric or mobile credentials to meet encryption and continuous-monitoring clauses. Vendor supply-chain scrutiny raises procurement thresholds, steering demand toward platforms offering automated compliance reporting. Synergies between NIS2 and GDPR are creating a premium for unified solutions that protect personal data while enforcing physical security, lifting overall replacement budgets across the access control market.

Contactless Mobile Credential Uptake in North American Corporate Real-Estate

Commercial landlords are issuing Apple Wallet and Google Pay credentials that unlock turnstiles, elevators and suites without physical interaction. Remote provisioning cuts badge issuance costs and supports flexible seating policies. Encrypted over-the-air updates let facility teams deactivate lost phones instantly, tightening security while enhancing tenant experience. The solution's compatibility with existing smartphone infrastructure eliminates card-printer overheads, strengthening its business case. Fast deployment cycles translate into visible gains in operational efficiency, reinforcing momentum for the access control market.

Cyber-Security Compliance Costs for EU Cloud Deployments (NIS2)

Cloud-hosted access platforms must add continuous threat-monitoring, secure code-signing and documented development pipelines to satisfy NIS2, lifting vendor operating costs by 15-20%. Small providers struggle to absorb audit fees and penetration-test expenses, triggering consolidation as buyers gravitate toward global brands with certified infrastructure. Some EU enterprises defer upgrades, stretching the replacement cycle, which marginally tempers the access control market growth outlook.

Other drivers and restraints analyzed in the detailed report include:

- Smart-City and Critical-Infrastructure Programs Boosting Biometrics in the Middle East

- Expansion of APAC Co-working Spaces Driving Cloud-Based ACaaS

- Secure MCU Chip Shortages Affecting Reader Shipments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware led 2025 revenue with 61.45% share, reflecting the essential need for electronic locks, controllers and biometric readers in physical deployments. University retrofits alone drove substantial lock refresh cycles as campuses shifted to mobile-ready infrastructure. Electronic locks posted the fastest unit growth, powered by ultra-wideband modules that enable hands-free entry. Biometric multi-sensor readers gained traction in laboratories and pharmacies demanding high-assurance verification.

Software is growing at 8.78% CAGR to 2031, adding predictive analytics and AI-driven anomaly detection to management consoles. Cloud control planes unify disparate sites, allowing real-time policy pushes and automated compliance audits. Video-access convergence within dashboards strengthens investigative capabilities, while open APIs invite ecosystem development. Integration services and recurring support contracts widen partner revenue, positioning managed services as a resilient annuity layer within the access control industry.

Hosted ACaaS controlled 51.60% of 2025 deployments, driven by SMEs favoring predictable subscriptions over server ownership. Feature parity with on-prem solutions, plus automatic updates, reduces the skills burden for lean IT departments. Granular tenant portals help co-working brands manage thousands of members dynamically, deepening customer loyalty within the access control market.

Hybrid ACaaS is the fastest-growing model at 8.35% CAGR, balancing cloud orchestration with local edge storage for regulated entities. Hospitals route sensitive logs to on-site appliances during network outages, then synchronize to the cloud for analytics once connectivity returns. Managed ACaaS retains a niche for complex, multi-vendor estates needing bespoke integrations, but platforms are steadily converging toward self-service paradigms that scale across sectors in the wider access control market.

Access Control Market is Segmented by Component (Hardware, Software, Services), Acaas Deployment (Hosted, Managed, Hybrid), Authentication Method (Single-Factor, Multi-Factor, Mobile Credential), Connectivity Technology (RFID/NFC, Smart Cards, Bluetooth LE, UWB), End-User Vertical (Commercial, Industrial, Government, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained 38.30% 2025 revenue share underpinned by large-scale modernizations in corporate campuses, universities and hospitals. US higher-education retrofits, such as the University of Kentucky's 9,000-door conversion, illustrate campus-wide embrace of mobile-ready platforms that blend access control with attendance analytics. Canada's smart-building incentives and Mexico's cross-border logistics facilities add incremental demand. Venture investment in UWB and biometric startups keeps the region at the forefront of technology innovation within the access control market.

The Middle East is the fastest-growing territory at 9.22% CAGR through 2031, lifted by sovereign smart-city agendas and security-first regulatory frameworks. UAE and Saudi Arabia demonstrate large-scale rollouts of facial, iris and fingerprint systems that replace physical IDs, while Qatar and Oman embed access control into nationwide IoT command centers. Local integrators build on global vendor SDKs, creating region-specific solutions that accelerate market localization.

Europe exhibits steady growth despite stringent privacy legislation. NIS2 and the EU AI Act require explicit consent and transparency for biometric use. Organizations respond by adopting hybrid ACaaS so that sensitive biometric templates remain on European soil. Germany, France and the UK prioritize open-protocol systems to avoid vendor lock-in, while Nordic operators pioneer sustainable, low-power readers. Eastern European transport hubs upgrade card-based barriers with mobile and video-verified entry, all contributing to incremental access control market revenue.

- ASSA ABLOY AB

- Johnson Controls International plc (Tyco)

- Honeywell International Inc.

- Dormakaba Holding AG

- Allegion plc

- Bosch Security Systems Inc.

- Thales Group (Gemalto)

- Suprema Inc.

- Hanwha Vision Co. Ltd.

- Schneider Electric SE

- NEC Corporation

- Idemia Group

- Nedap N.V.

- Axis Communications AB

- Panasonic Connect Co. Ltd.

- Brivo Systems LLC

- Identiv Inc.

- Salto Systems S.L.

- Siemens Smart Infrastructure

- Genetec Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Mandates for Electronic Access in GDPR-Sensitive EU Data Centers

- 4.2.2 Contactless Mobile Credential Uptake in North American Corporate Real-Estate

- 4.2.3 Smart-City and Critical-Infrastructure Programs Boosting Biometrics in the Middle East

- 4.2.4 Expansion of APAC Co-working Spaces Driving Cloud-Based ACaaS

- 4.2.5 IP Video Access Control Convergence Upgrades at European Transport Hubs

- 4.2.6 Retrofit Demand from Ageing Key-Card Systems in US Higher-Education

- 4.3 Market Restraints

- 4.3.1 Cyber-Security Compliance Costs for EU Cloud Deployments (NIS2)

- 4.3.2 Secure MCU Chip Shortages Affecting Reader Shipments

- 4.3.3 Privacy Pushback on Facial Recognition in US and EU States

- 4.3.4 SME Budget Constraints in South America

- 4.4 Supply-Chain Analysis

- 4.5 Technological Snapshot (Evolution, RFID vs NFC, Key Trends)

- 4.6 Regulatory and Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitutes

- 4.8 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Card / Proximity / Smart-card Readers

- 5.1.1.2 Biometric Readers (Fingerprint, Face, Iris, Multimodal)

- 5.1.1.3 Electronic Locks (Magnetic, Electric Strike, Deadbolt, Wireless Smart Lock)

- 5.1.1.4 Controllers and Panels

- 5.1.2 Software

- 5.1.2.1 Access Control Management Suites

- 5.1.2.2 Video Management Integration Plug-ins

- 5.1.3 Services

- 5.1.3.1 Installation and Integration

- 5.1.3.2 Support and Maintenance

- 5.1.1 Hardware

- 5.2 By Access Control-as-a-Service (Deployment)

- 5.2.1 Hosted ACaaS

- 5.2.2 Managed ACaaS

- 5.2.3 Hybrid ACaaS

- 5.3 By Authentication Method

- 5.3.1 Single-Factor Authentication

- 5.3.2 Multi-Factor Authentication

- 5.3.3 Mobile Credential / Bluetooth LE

- 5.4 By Connectivity Technology

- 5.4.1 RFID / NFC

- 5.4.2 Smart Cards (125 kHz, 13.56 MHz)

- 5.4.3 Bluetooth Low Energy

- 5.4.4 Ultra-Wideband (UWB)

- 5.5 By End-User Vertical

- 5.5.1 Commercial Buildings

- 5.5.2 Industrial and Manufacturing

- 5.5.3 Government and Public Sector

- 5.5.4 Transport and Logistics

- 5.5.5 Healthcare Facilities

- 5.5.6 Military and Defense Installations

- 5.5.7 Residential and Smart Homes

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Australia

- 5.6.4.7 New Zealand

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 GCC

- 5.6.5.1.2 Turkey

- 5.6.5.1.3 Israel

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Egypt

- 5.6.5.2.4 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, Partnerships, Product Launches)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 ASSA ABLOY AB

- 6.4.2 Johnson Controls International plc (Tyco)

- 6.4.3 Honeywell International Inc.

- 6.4.4 Dormakaba Holding AG

- 6.4.5 Allegion plc

- 6.4.6 Bosch Security Systems Inc.

- 6.4.7 Thales Group (Gemalto)

- 6.4.8 Suprema Inc.

- 6.4.9 Hanwha Vision Co. Ltd.

- 6.4.10 Schneider Electric SE

- 6.4.11 NEC Corporation

- 6.4.12 Idemia Group

- 6.4.13 Nedap N.V.

- 6.4.14 Axis Communications AB

- 6.4.15 Panasonic Connect Co. Ltd.

- 6.4.16 Brivo Systems LLC

- 6.4.17 Identiv Inc.

- 6.4.18 Salto Systems S.L.

- 6.4.19 Siemens Smart Infrastructure

- 6.4.20 Genetec Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment