PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851516

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851516

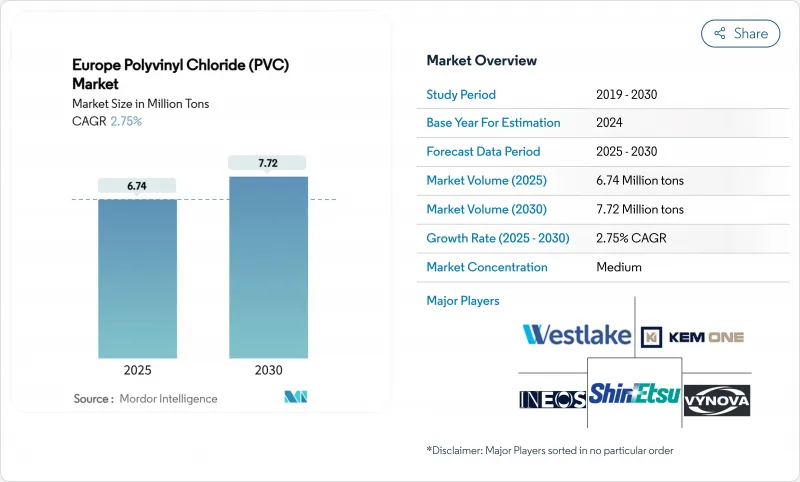

Europe Polyvinyl Chloride (PVC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Europe Polyvinyl Chloride Market size is estimated at 6.74 million tons in 2025, and is expected to reach 7.72 million tons by 2030, at a CAGR of 2.75% during the forecast period (2025-2030).

Robust demand in pipes, profiles, and fittings, coupled with moderate recovery in residential construction, underpins near-term volume gains. Regulatory pressure from REACH continues to accelerate calcium-zinc stabilizer adoption, yet sustained infrastructure spending cushions transition costs. Energy-efficient renovation programs, electrical grid upgrades, and water-management projects anchor structural demand, while circular-economy mandates fast-track investment in recycling and bio-attributed PVC. Competitive intensity remains moderate as integrated producers leverage scale, captive feedstocks, and proprietary technology to offset compliance costs.

Europe Polyvinyl Chloride (PVC) Market Trends and Insights

Growing Demand from Construction Industry

The region's housing shortage and aging building stock keep renovation activity high, driving window-profile and siding volumes in the Europe PVC market. Thermal-performance gains of 12-13% in PVC frames reinforced with thermoplastic inserts improve compliance with EU energy-efficiency codes, further entrenching rigid PVC in retrofit projects. Member-state recovery funds earmark civil-works spending, with water-retention drainage systems illustrating PVC's functional and cost advantages in agricultural infrastructure. Stabilizing interest rates and normalized material prices enhance project viability across Northern markets, though fiscal constraints continue to cap growth in Southern Europe. The overall effect is a well-distributed, medium-term lift in PVC pipe and profile demand.

Increasing Demand from Automotive Industry

Electric-vehicle adoption is reshaping interior-component specifications, widening the aperture for flame-retardant flexible PVC in wire harnesses and floor coverings. German motor-vehicle output advanced 3% YoY in early 2025, boosting resin off-take from regional compounding plants. Bio-attributed PVC grades cut cradle-to-gate CO2 emissions by 58% while preserving tensile and thermal performance, enabling OEMs to meet ESG targets without platform redesign. Growth clusters around Germany, France, and northern Italy facilitate optimized logistics and just-in-sequence supply models. Tier-one suppliers are pairing digital quality-control tools with material innovations to eliminate trim waste and reduce cycle times.

Accelerating Retailer Bans on PVC Food Packaging

Large supermarket chains across Western Europe are phasing out PVC trays and cling films, pressuring converters to shift toward mono-material PET or paper-based formats. The forthcoming Packaging and Packaging Waste Regulation adds PFAS and BPA constraints, complicating compliance pathways for legacy PVC formulations. While pharmaceutical blister packs remain exempt, high-volume fresh-food segments experience immediate substitution, shaving flexible-film demand in the Europe PVC market. Brand-owner purchasing policies cascade upstream, compelling compounders to qualify alternative resins or develop recyclable PVC-blends for niche, barrier-critical applications. Eastern markets show lagged uptake of bans, offering temporary relief yet signaling an eventual region-wide transition.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand from Water Infrastructure Projects

- Healthcare Demand for Medical-Grade PVC

- Escalating REACH Restrictions on Legacy Lead and Tin Stabilizers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rigid grades anchored 60.74% of the Europe PVC market share in 2024 as pipes, profiles, and fittings retain dominance across building and water-supply networks. Low-smoke PVC, although a smaller base, is set to clock the strongest 3.89% CAGR through 2030 on the back of fire-safety regulations in mass-transit, tunnel, and public-assembly projects. Flexible PVC volumes face mixed fortunes: demand for bio-plasticized clear grades in medical tubing offsets contraction in food-packaging films. Chlorinated PVC penetrates industrial hot-water lines, leveraging localized production to mitigate import tariffs and logistics costs.

Capacity additions stay disciplined as mature demand patterns stabilize operating rates around 80%. Extruders focus on die-head upgrades and inline-measurement systems to boost yields rather than greenfield expansions. Product-mix agility becomes a competitive differentiator as converters juggle rigid-clear orders for chemical-processing sight-glasses alongside bulk commitments for municipal pipe contracts. The Europe PVC market thus balances steady, high-volume rigid demand with specialty growth niches in low-smoke and CPVC segments.

Calcium-zinc solutions held 42.88% of stabilizer consumption in 2024, a clear signal of market pivot after the EU lead ban These packages are projected to expand at 3.61% CAGR to 2030, driving most additive-level value growth in the Europe PVC market. Lead-based stabilizers now persist mainly in recycled rigid streams under temporary derogations, while tin systems linger in heat-resistant wire-coating niches. Barium-zinc and liquid-mixed-metal formats supply specialty sheet calendaring but face volume erosion as unified green-chemistry criteria spread downstream.

Chemical suppliers scale modular blending facilities near major extrusion hubs, ensuring just-in-time deliveries and tighter formulation control. Collaborative qualification programs with profile manufacturers accelerate line-change approvals, compressing conversion timelines. The stabilizer shift underscores how regulatory imperatives reshape supply chains in favor of actors with R&D depth and integrated logistics.

The Europe PVC Market Report is Segmented by Product Type (Rigid PVC, Flexible PVC, Low-Smoke PVC, and More), Stabilizer Type (Calcium Based, Lead Based, Tin and Organotin Based, and More), Application (Pipes and Fittings, Films and Sheets, Wires and Cables, and More), End-User Industry (Building and Construction, Automotive, Electrical and Electronics, and More), and Geography (Germany, France, United Kingdom, Italy, and More).

List of Companies Covered in this Report:

- Benvic Group

- Ercros S.A.

- Formosa Plastics Corporation

- Hanwa Solutions Chemical Division Corporation

- Industrie Generali S.p.A.

- INEOS

- KEM ONE

- LG Chem

- Lukoil

- Oltchim SA

- Orbia

- Shin-Etsu Chemical Co. Ltd.

- SIBUR Holding PJSC

- Solvay

- Teknor Apex

- Vynova Group

- Westlake Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand from construction industry

- 4.2.2 Increasing demand from automotive industry

- 4.2.3 Increasing demand from water infrastructure projects

- 4.2.4 Healthcare demand for medical-grade PVC

- 4.2.5 Rinsing Usage in Packaging Application

- 4.3 Market Restraints

- 4.3.1 Accelerating retailer bans on PVC food packaging

- 4.3.2 Escalating REACH restrictions on legacy lead and tin stabilizers

- 4.3.3 Rising bio-based polymer substitution in window-profile segment

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Rigid PVC

- 5.1.1.1 Clear Rigid PVC

- 5.1.1.2 Non-clear Rigid PVC

- 5.1.2 Flexible PVC

- 5.1.2.1 Clear Flexible PVC

- 5.1.2.2 Non-clear Flexible PVC

- 5.1.3 Low-smoke PVC

- 5.1.4 Chlorinated PVC

- 5.1.1 Rigid PVC

- 5.2 By Stabilizer Type

- 5.2.1 Calcium based (Ca-Zn)

- 5.2.2 Lead based Pb)

- 5.2.3 Tin and Organotin based (Sn)

- 5.2.4 Barium-based and Others (Liquid Mixed Metals)

- 5.3 By Application

- 5.3.1 Pipes and Fittings

- 5.3.2 Films and Sheets

- 5.3.3 Wires and Cables

- 5.3.4 Bottles

- 5.3.5 Profiles, Hoses and Tubings

- 5.3.6 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Building and Construction

- 5.4.2 Automotive

- 5.4.3 Electrical and Electronics

- 5.4.4 Packaging

- 5.4.5 Footwear

- 5.4.6 Healthcare

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 France

- 5.5.3 United Kingdom

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Turkey

- 5.5.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Rankinh Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Benvic Group

- 6.4.2 Ercros S.A.

- 6.4.3 Formosa Plastics Corporation

- 6.4.4 Hanwa Solutions Chemical Division Corporation

- 6.4.5 Industrie Generali S.p.A.

- 6.4.6 INEOS

- 6.4.7 KEM ONE

- 6.4.8 LG Chem

- 6.4.9 Lukoil

- 6.4.10 Oltchim SA

- 6.4.11 Orbia

- 6.4.12 Shin-Etsu Chemical Co. Ltd.

- 6.4.13 SIBUR Holding PJSC

- 6.4.14 Solvay

- 6.4.15 Teknor Apex

- 6.4.16 Vynova Group

- 6.4.17 Westlake Corporation

7 Market Opportunities and Future Outlook

- 7.1 PVC Recycling and Circularity

- 7.2 Bio-based Stabilizer and Plasticizer Platforms

- 7.3 White-space and unmet-need assessment