PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851533

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851533

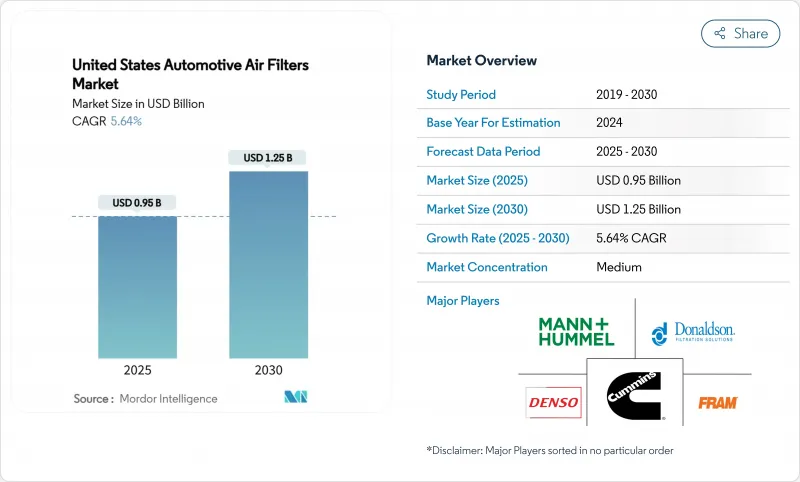

United States Automotive Air Filters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The United States automotive air filters market is valued at USD 0.95 billion in 2025 and is projected to grow at a 5.64% CAGR to reach USD 1.25 billion by 2030.

Steady expansion is underpinned by an aging national vehicle fleet, stricter emissions rules, and post-pandemic concern for in-car air quality. A record average vehicle age of 12.6 years boosts replacement volumes, while Environmental Protection Agency (EPA) particulate limits of 0.5 mg/mi compel automakers to integrate high-efficiency gasoline particulate filters. Cabin filter innovation accelerates as consumers seek allergen and pathogen protection, and nanofiber media gains traction by delivering higher capture efficiency with lower pressure drop. Supply-chain reconfiguration after the May 2025 import-tariff hike is pushing manufacturers toward regionalized sourcing, and forward-looking suppliers are investing in advanced thermal-management filtration to offset future internal-combustion-engine (ICE) volume attrition.

United States Automotive Air Filters Market Trends and Insights

Rise in Vehicle Production and Parc Growth

Vehicle production recovery and an expanding parc create a dual-demand surge. About 110 million units sit in the 6-14-year sweet spot for service, representing 38% of the total fleet and translating into higher filter-replacement frequency. Robust aftermarket expansion is supported by consumers deferring new-car purchases, which channels spending toward maintenance parts. OEM demand also rises as U.S. assembly plants ramp up output following supply-chain normalization. Together, these trends underpin stable volume increases across both factory-installed and replacement filters.

Stringent EPA Emission Standards

The EPA final rule for model-year 2027-2032 light-duty vehicles cuts fleet-average greenhouse-gas emissions in half and sets the first nationwide 0.5 mg/mi particulate limit. Automakers must therefore fit gasoline particulate filters on direct-injection engines, effectively adding an entirely new high-volume filter line. Compliance pressure is highest in California and other Section 177 states that historically adopt more aggressive thresholds, driving early procurement cycles that ripple through the supplier base.

Shift Toward BEVs Curbing ICE Filter Volumes

Battery-electric models eliminate fuel and oil filters and cut intake-air filter demand. The EPA forecasts that 30%-56% of light-duty sales will be electric by 2032, producing a structural headwind for ICE-specific categories. Although emerging BEV thermal-management filters offer partial volume substitution, they cannot fully offset the decline through 2030, tempering overall growth prospects for legacy component makers.

Other drivers and restraints analyzed in the detailed report include:

- Aging Fleet Boosting Aftermarket Demand

- Rising Adoption of Cabin Filters for In-Car Air Quality

- Raw-Material Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paper still commands 42.38% of the United States automotive air filters market share in 2024, owing to low cost and wide availability. The segment's entrenched tooling base and mass-production scale keep unit prices attractive for do-it-yourself shoppers and fleet managers alike. Nevertheless, nanofiber composites are forecast to grow at an 8.54% CAGR through 2030, the fastest among all substrates, as automakers and tier-ones specify media that deliver superior particulate capture without boosting pressure drop. Synthetic melt-blown blends occupy a mid-price niche, marrying durability with acceptable efficiency, while gauze and foam serve performance enthusiasts and specialty off-highway equipment.

Momentum is shifting as manufacturers retrofit domestic lines to mass-produce nano-enabled rolls, reducing import exposure and aligning with tariff-mitigation strategies. Sustainability pressures also influence material choice: PFAS-free coatings and recycled fibers are moving from optional to baseline requirements in new RFQs. Suppliers able to balance environmental credentials with filtration performance gain an edge in the United States automotive air filters market. Over the forecast horizon, value migration toward advanced materials supports price realization even as traditional paper volumes plateau.

Cabin units generated 56.27% of 2024 revenue, underscoring the consumer pivot toward wellness features inside the vehicle. Particulate cabin filters remain the volume leader, yet HEPA and antiviral variants are advancing at a 12.83% CAGR to 2030, driven by heightened sensitivity to allergens, wildfire smoke, and airborne viruses. Intake-air filters, still essential for ICE engines, face gradual volume erosion as BEVs gain share, although medium-duty trucks and off-highway machinery sustain demand. Fuel, oil, and transmission filters hold steady in the aftermarket but plateau in OEM channels as factory-filled units adopt extended-life designs.

Premium cabin media also deliver higher margins that offset sliding sales of traditional engine-air elements. Automakers now market air-quality technology as a competitive differentiator, bundling advanced filters with connected sensors that alert drivers when replacements are due. Regulatory bodies are exploring indoor-air-quality standards, further legitimizing the category. Collectively, these forces ensure cabin products remain the principal growth engine within the United States automotive air filters market.

The United States Automotive Air Filters Market Report is Segmented by Material Type (Paper, Synthetic, and More), Filter Type (Intake Filters [Cellulose Intake and More] and Cabin Filters [Particulate and More]), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Sales Channel (OEM and Aftermarket), and Distribution Channel (Online Retailers and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- KandN Engineering Inc.

- Mahle GmbH

- AL Group Ltd.

- Parker-Hannifin Corp.

- MANN+HUMMEL Group

- Denso Corporation

- Robert Bosch GmbH

- ACDelco (General Motors)

- First Brands Group LLC

- Cummins Filtration Inc.

- Donaldson Company Inc.

- Sogefi Filtration USA

- Fram Group

- Baldwin Filters

- Ahlstrom-Munksjo

- Hengst North America

- WIX Filters

- Fleetguard

- Freudenberg Filtration Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in vehicle production and parc growth

- 4.2.2 Stringent EPA / CARB emission standards

- 4.2.3 Aging fleet boosting aftermarket demand

- 4.2.4 Rising adoption of cabin filters for in-car air quality

- 4.2.5 Electrified powertrains need advanced thermal-air management

- 4.2.6 Nanofiber and antiviral media enter mass production

- 4.3 Market Restraints

- 4.3.1 Shift toward BEVs curbing ICE filter volumes

- 4.3.2 Raw-material (cellulose, synthetics) price volatility

- 4.3.3 Extended OEM service intervals lower replacement frequency

- 4.3.4 Growth of washable / reusable filters

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Material Type

- 5.1.1 Paper

- 5.1.2 Synthetic

- 5.1.3 Gauze

- 5.1.4 Foam

- 5.1.5 Nanofiber / Composite

- 5.1.6 Others

- 5.2 By Filter Type

- 5.2.1 Intake Filters

- 5.2.1.1 Cellulose Intake

- 5.2.1.2 Synthetic Intake

- 5.2.1.3 Nanofiber / Composite Intake

- 5.2.2 Cabin Filters

- 5.2.2.1 Particulate

- 5.2.2.2 Activated Carbon

- 5.2.2.3 HEPA / Antiviral

- 5.2.1 Intake Filters

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.3.4 Off-Highway (Construction and Agriculture)

- 5.3.5 Two-Wheelers

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Distribution Channel

- 5.5.1 Online Retailers

- 5.5.2 Brick and Mortar Retail

- 5.5.3 Service Centers and Dealerships

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 KandN Engineering Inc.

- 6.4.2 Mahle GmbH

- 6.4.3 AL Group Ltd.

- 6.4.4 Parker-Hannifin Corp.

- 6.4.5 MANN+HUMMEL Group

- 6.4.6 Denso Corporation

- 6.4.7 Robert Bosch GmbH

- 6.4.8 ACDelco (General Motors)

- 6.4.9 First Brands Group LLC

- 6.4.10 Cummins Filtration Inc.

- 6.4.11 Donaldson Company Inc.

- 6.4.12 Sogefi Filtration USA

- 6.4.13 Fram Group

- 6.4.14 Baldwin Filters

- 6.4.15 Ahlstrom-Munksjo

- 6.4.16 Hengst North America

- 6.4.17 WIX Filters

- 6.4.18 Fleetguard

- 6.4.19 Freudenberg Filtration Technologies

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment