PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907347

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907347

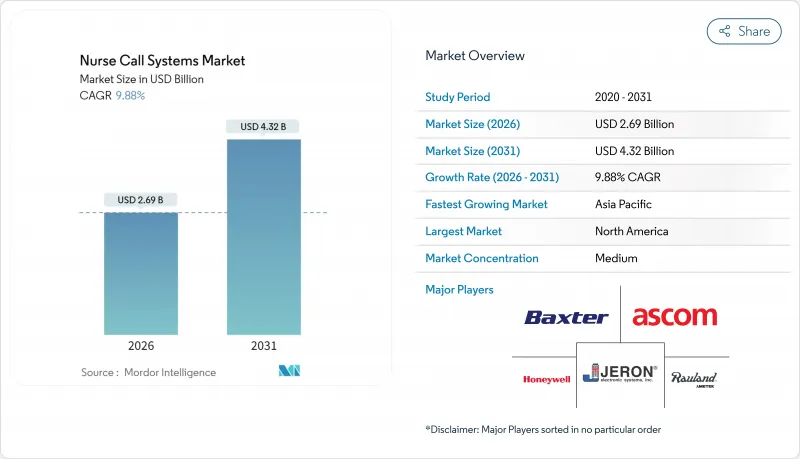

Nurse Call Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The nurse call systems market is expected to grow from USD 2.45 billion in 2025 to USD 2.69 billion in 2026 and is forecast to reach USD 4.32 billion by 2031 at 9.88% CAGR over 2026-2031.

Robust expansion in the nurse call systems market is rooted in hospitals' push for digital-first communication, pay-for-performance mandates, and the steady integration of real-time location analytics. Aging societies, stringent documentation requirements, and the shift toward predictive care elevate these systems from bedside buttons to workflow automation hubs. Technology polarization is clear: wireless platforms accumulate more than half of 2024 revenue, yet IP-based and mobile architectures grow even faster as facilities prioritize interoperability with electronic health records . Regionally, North America remains the largest revenue contributor, while Asia-Pacific delivers the swiftest growth thanks to public-private spending on smart hospitals. Competitive intensity rises as established device firms acquire software innovators to bundle nurse call, virtual monitoring, and ambient intelligence in one stack.

Global Nurse Call Systems Market Trends and Insights

Aging Population Driving Demand for Continuous Monitoring

Global life-expectancy gains double the 65-plus cohort between 2025 and 2050, sharply elevating fall and frailty risks. Care providers adopt predictive nurse call features that analyze movement and vitals to prevent incidents rather than merely respond. Long-term care facilities, growing at an 11.09% CAGR, deploy sensor-rich systems that alert nurses before a resident attempts unsafe ambulation. The pivot supports value-based reimbursement that rewards avoided hospitalizations. Vendors embed AI algorithms that learn individual mobility baselines and trigger early interventions, reducing emergency transfers by up to one-third in pilot programs.

Rapid Adoption of Digital Health Infrastructure by Hospitals

Hospital CIOs view nurse call networks as key data sources for operational dashboards that track response times, staff load, and patient satisfaction. IP-based architecture feeds real-time alerts into electronic health records, turning every button press into a time-stamped quality metric. Mobile clients running on staff smartphones trim hardware overhead and speed software rollouts, a driver behind the 10.98% CAGR in cloud-enabled platforms. Early adopters report 40% declines in alarm fatigue by funneling contextual alerts through clinical communication apps. The same data underpin Medicare performance scores, directly linking call-response efficiency with revenue.

High Upfront & Retrofit Costs for Legacy Facilities

Replacing 2000-era analog cabling with category-6 networks can surpass USD 100,000 in a 150-bed hospital, stalling projects. Structural renovations disrupt clinical workflow, forcing phased installations that extend timelines. Developing-world providers rely on donor budgets that fluctuate yearly, prolonging legacy use. Even after go-live, ongoing license fees and battery replacements add recurring costs absent in old wired buzzers. Financial constraints encourage selective feature adoption, leaving predictive analytics modules dormant until capital frees up.

Other drivers and restraints analyzed in the detailed report include:

- Rising Public-Private Investments in Smart Healthcare Facilities

- Technological Advances: IP-Based & Mobile-First Nurse Call Platforms

- Limited Staff Training & Change-Management Capabilities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mobile and cloud-enabled products remain the fastest-rising slice of the nurse call systems market at a 10.65% CAGR through 2031. Facilities value app-based alerts, secure texting, and on-device escalation rules that mirror consumer messaging simplicity. Traditional bedside call buttons still anchor 39.35% of 2025 revenue because every bed must offer a reliable hardwired trigger. Yet button hardware rarely evolves, so replacements lean toward IP-ready versions that pair with mobile dashboards. Intercom panels cater to operating theaters where clinicians need hands-free voice, while basic audio-visual units satisfy budget-constrained wards.

Platform vendors now bundle analytics subscriptions that flag response bottlenecks and predict maintenance before a dome-light fails. As these insights connect directly to reimbursement reports, upgrade justification strengthens. The nurse call systems market continues to reward suppliers that converge hardware, software, and services under one license, shrinking integration risk for buyers. Emerging entrants pitch software-only overlays compatible with standard SIP phones, intensifying price competition but spreading innovation to lower-tier hospitals .

Wireless deployments commanded 57.11% nurse call systems market share in 2025 and are tracking a 10.55% CAGR. Access points blanket clinical zones, offering room-level positioning for staff badges and patient wearables. Installation avoids wall chasing, crucial for heritage facilities with asbestos risks. Battery-powered pull cords and pillow speakers simplify retrofits but raise maintenance; vendors answer with six-year lithium packs and cloud alerts when charge drops.

Hardwired links endure in ICUs where electromagnetic interference tolerance and life-safety codes remain stringent. Many health networks now insist on dual-mode architecture: wireless for everyday workflow and redundant cabled loops for code events, aligning with NFPA 99 clarity. This hybrid philosophy fuels demand for unified management consoles that supervise both layers and integrate security patching. As Wi-Fi 7 emerges, latency and roaming issues weaken, encouraging migration of alarm audio streams that once required copper.

The Nurse Call Systems Market Report is Segmented by Product (Nurse Call Buttons, Intercom Nurse Call Systems, and More), Modality (Wired Systems, Wireless Systems), Application (Emergency Medical Alarms, Workflow & Staff Optimization, and More), End User (Hospitals and Specialty Clinics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained leadership with 41.05% of global revenue in 2025 as Medicare ties reimbursement to documented response times, compelling system upgrades. United States code frameworks such as UL 1069 streamline approvals, allowing providers to fast-track IP transitions. Hospitals pairing nurse call data with RTLS cut average response by 40% and hit 95% compliance on call-to-door metrics. Canada channels provincial digital-health grants toward cloud-based platforms to support pandemic-era virtual rounding.

Europe follows a steady path as national health systems modernize infrastructure while guarding data privacy. GDPR compliance pushes encryption-in-transit mandates, favoring vendors that can attest to ISO 27001 audits. Scandinavian hospitals link nurse call triggers to electronic medication charts, demonstrating risk reductions in omission errors. Energy-efficient PoE designs align with EU green directives, reducing power draw by 25% against legacy units and slashing lifecycle costs.

Asia-Pacific proves the most dynamic, charting an 10.85% CAGR through 2031. China's Trinity blueprint embeds nurse call nodes in every ward as a prerequisite for smart-grade certification. India's national health stack demands FHIR-based interoperability, prompting call vendors to open RESTful APIs. Japanese medical centers automate post-call audit trails to feed AI patient-flow engines that shaved 12 minutes off average discharge time in trials. ASEAN nations tap World Bank funds for modular nurse call rollouts in tier-2 cities, creating incremental demand. Collectively, these projects lift the nurse call systems market in Asia-Pacific faster than any other region.

- Ascom

- Baxter

- Honeywell International

- Rauland-Borg Corporation

- Tunstall Healthcare Group

- Austco Healthcare

- Jeron Electronic Systems Inc.

- Systems Technologies

- TekTone Sound & Signal Mfg. Inc.

- IndigoCare

- BEC Integrated Solutions LLC

- Cornell Communications

- Caretronic

- Fujian Huanyutong Technology

- West-Com Nurse Call Systems Inc.

- Accutech Healthcare

- Vigil Health Solutions Inc.

- Alpha Communications

- Intercall Systems

- Momentum Healthcare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging population driving demand for continuous monitoring

- 4.2.2 Rapid adoption of digital health infrastructure by hospitals

- 4.2.3 Rising public-private investments in smart healthcare facilities

- 4.2.4 Technological advances: IP-based & mobile-first nurse call platforms

- 4.2.5 Integration with RTLS boosting workflow analytics

- 4.2.6 Value-based care metrics incentivising response-time automation

- 4.3 Market Restraints

- 4.3.1 High upfront & retrofit costs for legacy facilities

- 4.3.2 Limited staff training & change-management capabilities

- 4.3.3 Growing cybersecurity & data-privacy vulnerabilities

- 4.3.4 Interoperability gaps with hospital IT stacks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Nurse Call Buttons

- 5.1.2 Intercom Nurse Call Systems

- 5.1.3 Basic Audio/Visual Systems

- 5.1.4 IP-Based Nurse Call Systems

- 5.1.5 Mobile & Cloud-Enabled Nurse Call Platforms

- 5.2 By Modality

- 5.2.1 Wired Systems

- 5.2.2 Wireless Systems

- 5.3 By Application

- 5.3.1 Emergency Medical Alarms

- 5.3.2 Workflow & Staff Optimization

- 5.3.3 Fall Detection & Prevention

- 5.3.4 Wanderer Control & Dementia Care

- 5.4 By End User

- 5.4.1 Hospitals and Specialty Clinics

- 5.4.2 Long-Term Care Facilities

- 5.4.3 Nursing Homes

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Ascom Holding AG

- 6.3.2 Baxter International

- 6.3.3 Honeywell International Inc.

- 6.3.4 Rauland-Borg Corporation

- 6.3.5 Tunstall Healthcare Group

- 6.3.6 Austco Healthcare

- 6.3.7 Jeron Electronic Systems Inc.

- 6.3.8 Systems Technologies

- 6.3.9 TekTone Sound & Signal Mfg. Inc.

- 6.3.10 IndigoCare

- 6.3.11 BEC Integrated Solutions LLC

- 6.3.12 Cornell Communications

- 6.3.13 Caretronic

- 6.3.14 Fujian Huanyutong Technology Co. Ltd

- 6.3.15 West-Com Nurse Call Systems Inc.

- 6.3.16 Accutech Healthcare

- 6.3.17 Vigil Health Solutions Inc.

- 6.3.18 Alpha Communications

- 6.3.19 Intercall Systems

- 6.3.20 Momentum Healthware

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment