PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851568

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851568

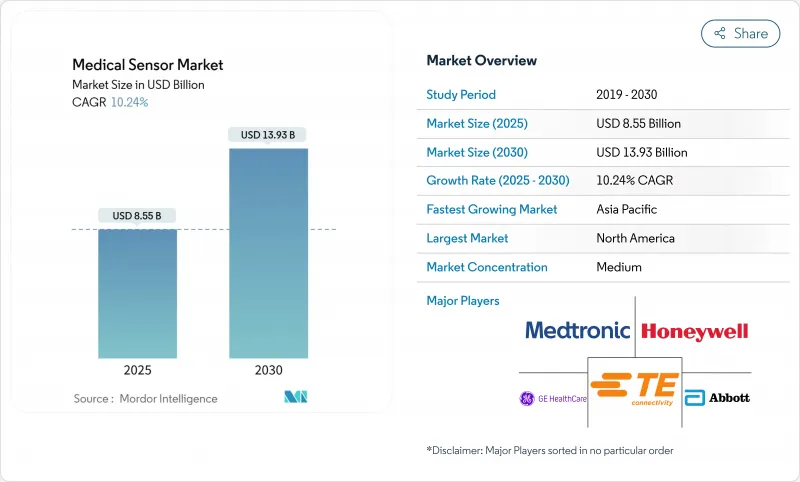

Medical Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The medical sensors market was valued at USD 8.55 billion in 2025 and is projected to reach USD 13.93 billion by 2030, advancing at a 10.24% CAGR.

Rapid semiconductor miniaturization, AI-enabled analytics, and supportive regulatory pathways are accelerating commercialization across clinical and consumer settings. Biosensors retain demand leadership as glucose monitoring shifts from episodic testing to real-time feedback. Optical and image sensors gain momentum through high-resolution, non-invasive diagnostics that complement traditional modalities. Domestic fabrication incentives under the U.S. CHIPS Act, combined with national procurement programs in China, continue to shape supply chains and regional competitive advantages. Strategic partnerships between device firms and technology companies are shortening development cycles and broadening ecosystem integration to unlock new revenue pools across the medical sensors market.

Global Medical Sensor Market Trends and Insights

AI-enabled continuous glucose monitoring adoption

Roche secured CE Mark for its Accu-Chek SmartGuide system in 2024, integrating predictive algorithms that anticipate hypoglycemia events hours in advance. The FDA expanded automated insulin dosing clearance to Type 2 diabetes patients the same year, validating a path for closed-loop therapies. Dexcom's USD 75 million investment in Oura underscores convergence between metabolic sensing and holistic wellness tracking. Collaboration between Abbott and Medtronic is accelerating interoperable platforms that link CGM data to pump algorithms in near real time. IBM and Roche advanced this trajectory in 2025 by adding lifestyle-based predictive models to sensor dashboards.

EU MDR-driven shift to traceable disposable sensors

Medical Device Regulation enforcement obliges full life-cycle traceability through unique device identifiers embedded in even single-use products, pushing manufacturers to integrate digital tracking into disposables shipped to European clinics. German hospitals now pilot 3D-printed microfluidic wound sensors that log batch data at the point of care, creating feedback loops that support both reimbursement and post-market surveillance. Global firms increasingly adopt MDR-compliant design across all facilities to avoid dual inventories, elevating quality baselines in Asia-Pacific contract lines that supply European orders.

Divergent cyber-security labeling

Mismatch between the FDA's real-time threat assessment framework and the EU's pre-market security dossier rulebook requires dual validation pipelines. Development timelines lengthen by up to 20% and smaller entrants frequently limit launches to a single region, constraining competitive diversity and slowing global diffusion of innovations.

Other drivers and restraints analyzed in the detailed report include:

- China NHSA procurement of home-use SpO2 wearables

- Demand for sterilizable sensors in robotic-assisted surgery

- Medical-grade semiconductor wafer shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Biosensors captured 44% of the medical sensors market in 2024, anchored by glucose, cardiac, and infectious disease assays that display strong reimbursement support. Blood-glucose modules dominate subsegment revenues as continuous sensing replaces fingerstick diagnostics. Electrochemical platforms integrate AI filters that flag anomalous readings and reduce false alarms, boosting clinician trust. Pressure sensors remain critical in ventilators and hemodynamic monitors, while temperature elements now feature in multiparameter wearables that track fever progression. Flow sensors support respiratory therapy devices whose volumes rose following pandemic surges. Optical and image sensors hold the fastest growth path with a 14.8% CAGR as terahertz and hyperspectral modalities enable non-invasive tissue characterization. Accelerometers advance rehabilitation tools for stroke survivors, and niche graphene biosensors demonstrate sub-picomolar detection thresholds that anticipate future commercial uptake.

The competitive mix within biosensors is widening as research centers patent carbon nanotube arrays targeting hormonal biomarkers, adding depth to the medical sensors industry pipeline. Market leaders co-develop sensor-analytics bundles that merge raw signals with predictive dashboards. This services layer raises switching costs and broadens profit pools beyond the hardware sale. Given these trends, biosensors will preserve their dominant role while ceding relative percentage share to image-centric modalities that address oncology and dermatology needs within the medical sensors market.

MEMS platforms provided 52.5% of the medical sensors market size in 2024 due to matured fabrication ecosystems and established reliability metrics. They underpin pressure, inertial, and flow devices across ICU monitors and ambulatory pumps. CMOS fabrication supports high-resolution image sensors and multifunctional system-on-chip solutions that house photodiodes, amplifiers, and radio interfaces. Fiber-optic sensors penetrate MRI suites and burn units where electromagnetic immunity is mandatory, supported by advances in flexible glass fibers that survive tensile strain.

Nano and graphene devices, though only a fraction of shipments, will post a 15.2% CAGR through 2030. Graphene metasurface biosensors demonstrated single-molecule viral detection in laboratory trial. Universities also produced sound-wave graphene sensors that achieve chemical fingerprinting, underscoring ultra-high sensitivity possibilities. Parallel progress in 3D-printed organic electronics opens design freedom for custom geometries that conventional lithography cannot deliver. As production yields improve, nano-scale architectures will increasingly displace MEMS in niche, high-sensitivity use cases across the medical sensors market.

The Medical Sensors Report is Segmented by Sensor Type (Pressure, Temperature, Biosensors, Blood-Glucose, and More), Technology (MEMS, CMOS, Fiber-Optic, and More), Deployment (Wearable, Implantable, Invasive, and More), Application (Patient Monitoring, Diagnostics, Therapeutic, Surgical, Wellness), End-User (Hospitals, Ambulatory, Home-Care, Clinics), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained 34.6% revenue share in 2024 owing to large installed bases of connected diabetes and cardiac devices. The CHIPS Act earmarks USD 52 billion for semiconductor capacity that prioritizes medical allocations, reducing import reliance. FDA cybersecurity guidance promotes secure-by-design principles, granting compliant vendors first-mover position. Strategic alliances, such as the Dexcom-Oura partnership, spotlight a region where consumer wearables and regulated devices increasingly overlap. Canada leverages a single-payer model to pilot community-scale remote monitoring, while Mexico attracts nearshored sensor component production under US-Mexico-Canada free trade provisions.

Asia-Pacific presents the fastest expansion at a 14.51% CAGR through 2030. China's NHSA mass procurement funnels millions of SpO2 wearables into primary care, creating the largest longitudinal oximetry dataset worldwide. Japan's aging society and high adoption of robotic surgery fuel demand for autoclave-resistant sensors. India scales low-cost glucometers under national non-communicable disease programs. South Korea's foundries enable co-location of design and fabrication, shortening cycle times for next-generation pressure and image sensors. Semiconductor wafer shortages remain a headwind, yet government incentives encourage local capacity build-out, maintaining momentum across the medical sensors market.

Europe benefits from harmonized MDR regulations that elevate traceability standards and spur adoption of smart disposable sensors. Germany pilots 3D-printed wound sensors that offer embedded UDI codes for post-market surveillance. The United Kingdom's National Health Service trials multi-parameter wearables under digital ward models, though clinician workload concerns moderate rollout speed. France and Italy adapt cybersecurity conformity assessments ahead of EU deadlines, supporting cross-border device portability. Data privacy mandates drive encryption and edge-processing innovations, shaping global design templates for secure medical sensors market deployments.

- Analog Devices Inc.

- GE Healthcare Technologies Inc.

- Honeywell International Inc.

- TE Connectivity Ltd.

- Medtronic plc

- Abbott Laboratories

- Dexcom Inc.

- Philips Healthcare

- Siemens Healthineers AG

- STMicroelectronics N.V.

- Texas Instruments Inc.

- NXP Semiconductors N.V.

- Sensirion AG

- First Sensor AG

- Masimo Corporation

- Omron Corporation

- Amphenol Advanced Sensors

- Analog Devices

- Danaher Corporation

- FISO Technologies Inc.

- Others (ensure 20 total)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-enabled Continuous Glucose Monitoring Adoption in North America

- 4.2.2 EU MDR-Driven Shift to Traceable Disposable Sensors

- 4.2.3 China NHSA Procurement of Home-use SpO Wearables

- 4.2.4 Demand for Sterilizable Sensors in Robotic-Assisted Surgery (Japan)

- 4.2.5 U.S. CHIPS-Act MEMS Fabs for Medical Sensors

- 4.2.6 3D-Printed Microfluidic Wound Sensors in German Hospitals

- 4.3 Market Restraints

- 4.3.1 Divergent Cyber-Security Labeling (FDA RTA-V vs EU MDCG 2024-12)

- 4.3.2 Medical-grade Semiconductor Wafer Shortage (APAC)

- 4.3.3 EU WEEE/RoHS 2024 Cost Impact on Single-use Sensors

- 4.3.4 Clinician Workflow Overload with Multi-param Wearables (UK NHS)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Sensor Type

- 5.1.1 Pressure Sensors

- 5.1.2 Temperature Sensors

- 5.1.3 Biosensors

- 5.1.4 Blood-Glucose Sensors

- 5.1.5 Flow / Airflow Sensors

- 5.1.6 Optical / Image Sensors

- 5.1.7 Accelerometers and Motion Sensors

- 5.1.8 Other Types

- 5.2 By Technology

- 5.2.1 MEMS

- 5.2.2 CMOS

- 5.2.3 Fiber-optic

- 5.2.4 Nano / Graphene

- 5.2.5 3D-Printed

- 5.2.6 Sensor Fusion Modules

- 5.3 By Mode of Deployment

- 5.3.1 Wearable

- 5.3.2 Implantable

- 5.3.3 Invasive (Catheter-based)

- 5.3.4 Non-invasive

- 5.3.5 Disposable / Single-use

- 5.4 By Application

- 5.4.1 Patient Monitoring (Vital Signs, RPM)

- 5.4.2 Diagnostic Imaging and In-vitro Diagnostics

- 5.4.3 Therapeutic and Drug-Delivery

- 5.4.4 Surgical and Minimally-Invasive Procedures

- 5.4.5 Wellness and Fitness

- 5.5 By End-user

- 5.5.1 Hospitals and Large Health Systems

- 5.5.2 Ambulatory Surgical Centers

- 5.5.3 Home-care Settings

- 5.5.4 Specialty Clinics and Diagnostic Labs

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Israel

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 United Arab Emirates

- 5.6.4.4 Turkey

- 5.6.4.5 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Analog Devices Inc.

- 6.3.2 GE Healthcare Technologies Inc.

- 6.3.3 Honeywell International Inc.

- 6.3.4 TE Connectivity Ltd.

- 6.3.5 Medtronic plc

- 6.3.6 Abbott Laboratories

- 6.3.7 Dexcom Inc.

- 6.3.8 Philips Healthcare

- 6.3.9 Siemens Healthineers AG

- 6.3.10 STMicroelectronics N.V.

- 6.3.11 Texas Instruments Inc.

- 6.3.12 NXP Semiconductors N.V.

- 6.3.13 Sensirion AG

- 6.3.14 First Sensor AG

- 6.3.15 Masimo Corporation

- 6.3.16 Omron Corporation

- 6.3.17 Amphenol Advanced Sensors

- 6.3.18 Analog Devices

- 6.3.19 Danaher Corporation

- 6.3.20 FISO Technologies Inc.

- 6.3.21 Others (ensure 20 total)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment