PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851583

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851583

Resistive RAM - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

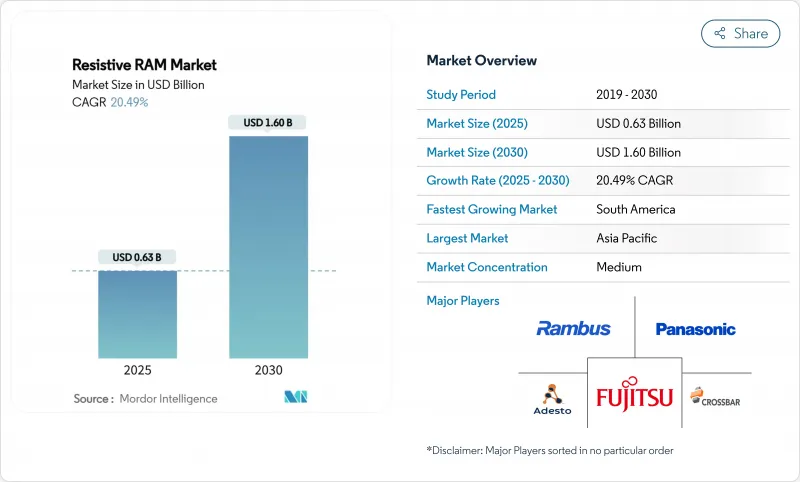

The resistive random access memory market size stood at USD 0.63 billion in 2025 and is forecast to reach USD 1.60 billion by 2030, expanding at a 20.49% CAGR over 2025-2030.

Multiple factors drove this steep climb. Production-grade endurance above 1012 cycles unlocked mission-critical and high-write-frequency workloads, while sub-1V switching created headroom for battery-powered edge devices. Asia-Pacific's deep foundry base accelerated embedded ReRAM tape-outs below 28 nm, and automotive ADAS programs raised demand for high-temperature non-volatile options that conventional flash could not meet. Venture capital funding for neuromorphic compute start-ups also added momentum. Together, these trends signaled that ReRAM was moving from laboratory proof-of-concept to mainstream volume adoption.

Global Resistive RAM Market Trends and Insights

Breakthrough endurance beyond 1012 cycles

Endurance exceeding 1012 cycles positioned ReRAM as a realistic flash replacement for write-intensive enterprise workloads. Academic teams reported aluminum-scandium nitride ferroelectric stacks persisting through 101° cycles while retaining polarization.Weebit Nano later validated 100,000 program cycles at 150 °C during automotive tests. This durability lets storage vendors contemplate using ReRAM for hot-tier caching that had previously defaulted to DRAM.

Sub-1 V switching for ultra-low-power edge devices

Research from the University of Virginia showed a 0.6 V conductive-bridge ReRAM macro consuming 8 pJ per write, eliminating charge-pump overhead. Intel echoed the feasibility of sub-1V operation when it demonstrated FinFET-based embedded ReRAM on 22FFL nodes. Battery life gains mattered across wearables, sensor nodes, and smart meters.

Filament variability causing write-noise and bit-error

Variability in conductive paths hampered yield during high-reliability production. Studies on Ta2O5 devices linked voltage-dependent noise to degraded weight resolution in neural arrays. Crossbar-scale thermal interactions added uncertainty. Wake-up cycling in Al2O3 stacks offered mitigation but lengthened process flows.

Other drivers and restraints analyzed in the detailed report include:

- Foundry support for embedded ReRAM at 28 nm and below

- Automotive ADAS demand for high-temperature NVM

- Limited IP and know-how outside a few licensors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oxide-based devices retained 46.3% share of the resistive random access memory market in 2024. HfO2 and Al2O3 stacks were already part of mainstream CMOS flows, which lowered adoption risk. Conductive-bridge variants, often copper-based, registered a 26.2% CAGR outlook because their sub-1V write capability aligned with wearables and micro-power nodes. The resistive random access memory market size for conductive-bridge devices is projected to reach USD 0.49 billion by 2030, reflecting designers' preference for energy headroom in edge architectures. Nanometal filament approaches captured niche demand where extreme miniaturization or high radiation tolerance mattered. Hybrid carbon filaments demonstrated forming-free operation at 37 nm with >107 cycles.

Oxide-based suppliers responded by enhancing endurance through vacancy-engineered layers that reduced cycle-to-cycle variability. Foundry libraries now bundle oxide-based ReRAM macros alongside logic IP, simplifying MCU tape-outs. Conversely, conductive-bridge proponents leveraged lower programming currents to market battery-life gains. Both camps invested in neural-network analog weight storage demonstrations to tap AI accelerators.

Embedded solutions held 55.4% of revenue in 2024 because system-on-chip designers valued die-space savings and simplified bills of materials. MCU vendors embedded 1-4 Mbit macros for secure code storage, firmware updates, and instant-on features. The resistive random access memory market share of embedded devices is expected to remain above 50% through 2030, even as stand-alone density rises.

Stand-alone ReRAM recorded a 25.2% CAGR projection as AI and HPC customers sought bespoke memory modules. Designers could tune array geometry and selector stacks without logic constraints, enabling larger word lines for parallel analog multiply-accumulate. A 4 Mbit compute-in-memory macro with 8-bit precision demonstrated inference at micro-joule energy levels. Cloud vendors evaluated these stand-alone chips as DRAM cache complements for training workloads that benefit from in-situ weight updates.

Resistive Random Access Memory (ReRAM) is Segmented by Material Type (Oxide-Based, Conductive-Bridge, and Nanometal Filament), Form Factor (Embedded ReRAM, and Stand-Alone ReRAM), Application (In-Memory Computing, Persistent Storage, and Fast Boot/Code Storage), End-User (Industrial and IoT Devices, Automotive and Mobility, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Geography Analysis

Asia-Pacific commanded 41.3% revenue in 2024. Massive foundry investments by Samsung, SK Hynix, and Kioxia expanded embedded ReRAM design kits below 28 nm. South Korea allocated USD 75 billion for advanced memory capacity through 2028, funneling funds into high-bandwidth and next-generation NVM lines. Japan pursued a USD 67 billion semiconductor renaissance plan with ReRAM earmarked for AI edge devices.

South America emerged as the fastest-growing cluster, posting 22.2% CAGR. Brazil funded a R$650 million (USD 130 million) expansion in Atibaia and Manaus to localize encapsulation and test, targeting both ReRAM and DRAM packaging. Regional governments also facilitated the rare-earth mineral supply for oxide films. The resistive random access memory market in South America, therefore, benefited from vertical integration incentives.

North America retained design leadership, leveraging automotive and aerospace use cases that demand radiation hardening. The resistive random access memory market size for the US and Canada is forecast to climb alongside ADAS memory mix shifts. Europe focused on industrial control vendors integrating compute-in-memory macros for real-time analytics. The Middle East and Africa saw early traction in smart-city sensor grids where low-power persistent memory reduced maintenance cycles.

- Crossbar Inc.

- Weebit Nano Ltd.

- 4DS Memory Limited

- Fujitsu Semiconductor Memory Solution Ltd.

- Xinyuan Semiconductor (Shanghai) Co., Ltd.

- Dialog Semiconductor Ltd. (Renesas)

- Panasonic Holdings Corp.

- Sony Semiconductor Solutions Corp.

- Micron Technology Inc.

- Intel Corporation

- IBM Corporation

- Western Digital Technologies, Inc.

- SK hynix Inc.

- Samsung Electronics Co., Ltd.

- TDK Corporation

- Infineon Technologies AG

- Renesas Electronics Corp.

- SMIC

- TetraMem Inc.

- ReRam Nanotech Ltd.

- Adesto Technologies Corp. (Dialog)

- Avalanche Technology Inc.

- RRAMTech S.r.l.

- CEA-Leti

- GigaDevice Semiconductor Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Break-through endurance improvements beyond 1012 cycles

- 4.2.2 Sub-1 V switching enabling ultra-low-power edge devices

- 4.2.3 Foundry support for embedded ReRAM at 28 nm and below

- 4.2.4 Automotive ADAS demand for high-temperature NVM

- 4.2.5 VC funding surge in neuromorphic compute start-ups

- 4.3 Market Restraints

- 4.3.1 Filament variability causing write-noise and bit-error

- 4.3.2 Limited IP/know-how outside a handful of licensors

- 4.3.3 Challenging integration with 3D NAND BEOL stacks

- 4.4 Impact of Macroeconomic Factors

- 4.5 Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Oxide-based (OxRRAM)

- 5.1.2 Conductive-Bridge (CBRAM)

- 5.1.3 Nanometal Filament

- 5.2 By Form Factor

- 5.2.1 Embedded ReRAM

- 5.2.2 Stand-alone ReRAM

- 5.3 By Application

- 5.3.1 In-Memory Computing

- 5.3.2 Persistent Storage

- 5.3.3 Fast Boot / Code Storage

- 5.4 By End-user

- 5.4.1 Industrial and IoT Devices

- 5.4.2 Automotive and Mobility

- 5.4.3 Datacentres and Enterprise SSD

- 5.4.4 Wearables and Consumer Electronics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 Taiwan

- 5.5.4.5 India

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Crossbar Inc.

- 6.4.2 Weebit Nano Ltd.

- 6.4.3 4DS Memory Limited

- 6.4.4 Fujitsu Semiconductor Memory Solution Ltd.

- 6.4.5 Xinyuan Semiconductor (Shanghai) Co., Ltd.

- 6.4.6 Dialog Semiconductor Ltd. (Renesas)

- 6.4.7 Panasonic Holdings Corp.

- 6.4.8 Sony Semiconductor Solutions Corp.

- 6.4.9 Micron Technology Inc.

- 6.4.10 Intel Corporation

- 6.4.11 IBM Corporation

- 6.4.12 Western Digital Technologies, Inc.

- 6.4.13 SK hynix Inc.

- 6.4.14 Samsung Electronics Co., Ltd.

- 6.4.15 TDK Corporation

- 6.4.16 Infineon Technologies AG

- 6.4.17 Renesas Electronics Corp.

- 6.4.18 SMIC

- 6.4.19 TetraMem Inc.

- 6.4.20 ReRam Nanotech Ltd.

- 6.4.21 Adesto Technologies Corp. (Dialog)

- 6.4.22 Avalanche Technology Inc.

- 6.4.23 RRAMTech S.r.l.

- 6.4.24 CEA-Leti

- 6.4.25 GigaDevice Semiconductor Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment