PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910474

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910474

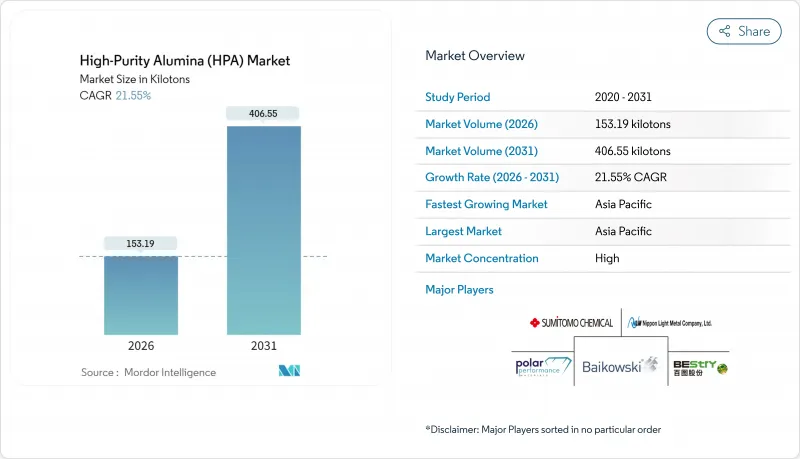

High-Purity Alumina (HPA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The High-Purity Alumina Market was valued at 126.03 kilotons in 2025 and estimated to grow from 153.19 kilotons in 2026 to reach 406.55 kilotons by 2031, at a CAGR of 21.55% during the forecast period (2026-2031).

This steep growth curve reflects surging demand from lithium-ion batteries, sustained momentum in LED lighting, and accelerating adoption in advanced semiconductor packaging. An expanding base of electric-vehicle and energy-storage projects is pulling HPA grades toward ultra-high purities, while producers race to commission lower-cost, lower-carbon capacity based on hydrochloric-acid leaching and solvent-extraction routes. At the same time, breakthroughs in patterned sapphire substrates and larger wafer formats are lifting LED chip yields and keeping traditional 4N demand stable. Semiconductor fabs are pushing for 6N grades that support co-packaged optics and vertical GaN devices, adding another layer of structural demand. Although high production cost remains the primary brake on broader uptake, rapid scale-up is narrowing the cost gap versus lower-purity aluminas, and early adopters in batteries and power electronics are absorbing the premium.

Global High-Purity Alumina (HPA) Market Trends and Insights

Increasing Demand for LED-Based Lighting

Sapphire substrates remain the backbone of high-brightness LEDs because they tolerate high thermal loads and sustain optical clarity. Migration from 2-4 to 6-8 in wafers has raised chip throughput per melt, boosted yield, and lowered die cost. Patterned sapphire substrates now lift light-extraction efficiency by up to 40%, directly improving lumens per watt. Research on Ce-doped garnet ceramics has pushed luminous efficiency to 261.98 lm W-1, stretching the performance ceiling for high-power white emitters. Flexible nanoimprint lithography further cuts process time, raising microstructured LED productivity six-fold. Together, these advances keep LED producers firmly anchored to 4N HPA while opening selective pull-through for 5N grades in ultra-high-luminance devices.

Growing Demand from Lithium-Ion Battery Markets

Rapid scale-up of power-dense cells in passenger EVs and stationary storage propels separator-coating demand for 5N and 6N HPA. Coatings based on alumina nanolayers improve thermal shut-down behavior and suppress dendrite growth, enabling faster charging and longer cycle life. Altech's silicon-anode program, underpinned by an 8,000 tons/year HPA coating plant in Germany, targets 30% higher energy retention versus graphite baselines. The project's EUR 684 million (~USD 793.55 million) NPV and 34% IRR confirm commercial traction for premium grades. Battery OEMs in China are already trialing 6N HPA on ceramic-coated separators for next-generation fast-charge cells, marking a pivot point for large-volume qualifying runs.

High Cost of High-Purity Alumina

Calcination and multiple recrystallization stages keep energy use high, especially for 5N and 6N grades, which can trade at price premiums. Alpha HPA's solvent-extraction route, which bypasses the aluminum-metal step, claims 70% lower carbon emissions and a significant cut in power intensity. While this narrows the cost delta, widespread commissioning of similar plants is still two to three years away, exposing near-term procurement budgets. Spot price volatility in industrial alumina further complicates long-term offtake negotiations for specialty users.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Usage in Semiconductors

- Adoption of HPA-Based Thermal Interface Materials in EV Power-Electronics Modules

- Availability of Low-Cost Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, the 4N grade commanded 73.12% of total volume, anchored by sapphire wafers for general-purpose LEDs. At the same time, 6N shipments are on a 22.22% CAGR path, lifted by semiconductor and next-generation battery uses that demand sub-ppm impurity levels. Alpha HPA's closed-loop solvent-extraction pilot demonstrated full reagent recycling, lowering variable production cost, and making 5N and 6N more accessible. Manufacturers are adopting hybrid strategies, producing 4N for mass LED use and diverting incremental capacity to 6N to serve high-margin contracts. As battery OEMs begin to mandate more than or equal to 5N coatings for fast-charge cells, demand elasticity improves even in traditionally price-sensitive regions. Heightened research and development around energy-efficient purification is expected to close a portion of the cost gap, accelerating the premium-grade mix within the High-Purity Alumina market.

The legacy aluminum-alkoxide hydrolysis route delivered 87.25% of global output in 2025, owing to mature supply chains and ample bauxite feedstock. However, new entrants are favoring hydrochloric-acid leaching, which is scaling at a 22.35% CAGR, encouraged by lower capex per tonne and easier impurity bleed-off. Two-step sintering studies that combine spark-plasma densification with pressureless finishing showed a 19% flexural-strength gain alongside reduced furnace time. Emerging Southeast Asian refineries use modular HCl regeneration units to cut acid consumption and shrink effluent loads, aligning with stricter regional environmental norms. Incumbents are retrofitting older hydrolysis lines with solvent-extraction polishing stages to raise purity yields, preserving market position. Over the medium term, technology choice may hinge on proposed carbon-intensity disclosure rules in Europe and North America, potentially tipping marginal investment toward leach-based plants that score lower on embedded emissions.

The High Purity Alumina Market Report Segments the Industry by Type (4N, 5N, and 6N), Production Technology (Hydrolysis and Hydrochloric Acid Leaching), Application (LED Lighting, Phosphor, Semiconductor, Lithium-Ion (Li-Ion) Batteries, and More), End-User Industry (Electronics, Automotive, Energy Storage, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific accounted for 75.61% of the High Purity Alumina market volume in 2025, supported by China's integrated alumina value chain and Japan's and South Korea's leadership in LED and semiconductor fabrication. The region's market is projected to add 22.85% annually through 2031, thanks to aggressive EV roll-outs, growing wafer fabs, and new solvent-extraction refineries coming online in Australia.

North America is leveraging federal incentives for semiconductor reshoring and growing public-charging infrastructure that lifts lithium-ion battery demand. Canada and the United States benefit from stable electricity grids, supporting low-carbon production ambitions. South America, the Middle East, and Africa contribute modestly but represent long-run opportunities as bauxite-rich nations seek downstream diversification.

Brazil has outlined incentives for specialty alumina, while Saudi Arabia investigates alumina refining linked to its broader minerals strategy. These regions provide optionality for High-Purity Alumina market participants seeking geographic risk diversification.

- Advanced Energy Minerals

- Altech Advanced Materials

- Alpha HPA

- Baikowski SA

- Bestry

- Hebei Pengda New Materials Technology Co., Ltd.

- HONGHE CHEMICAL

- Nippon Light Metal Company, Ltd.

- Polar Performance Materials

- RusAL

- Sasol

- Saint-Gobain

- Shandong Keheng Crystal Material Technology Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Xuancheng Jingrui New Materials Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Led-based Lighting

- 4.2.2 Growing Demand from Lithium-ion Battery Markets

- 4.2.3 Increasing Usage of High Purity Alumina in Semiconductors

- 4.2.4 Adoption of HPA-Based Thermal Interface Materials in EV Power-Electronics Modules

- 4.2.5 Increasing Demand from the Electronics Industry

- 4.3 Market Restraints

- 4.3.1 High Cost of High-purity Alumina

- 4.3.2 Availabity of Low Cost Alternatives

- 4.3.3 Limited Availability of Raw Material Across the Globe

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Purity Level (Type)

- 5.1.1 4N

- 5.1.2 5N

- 5.1.3 6N

- 5.2 By Production Technology

- 5.2.1 Hydrolysis

- 5.2.2 Hydrochloric Acid Leaching

- 5.3 By Application

- 5.3.1 LED Lighting

- 5.3.2 Phosphor

- 5.3.3 Semiconductor

- 5.3.4 Lithium-ion Batteries

- 5.3.5 Technical Ceramics

- 5.3.6 Others (Scratch-Resistant Glass, Optical Lenses, etc.)

- 5.4 By End-User Industry

- 5.4.1 Electronics

- 5.4.2 Automotive

- 5.4.3 Energy Storage

- 5.4.4 Medical Devices

- 5.4.5 Industrial Manufacturing

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Malaysia

- 5.5.1.6 Thailand

- 5.5.1.7 Indonesia

- 5.5.1.8 Vietnam

- 5.5.1.9 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordic Countries

- 5.5.3.7 Turkey

- 5.5.3.8 Russia

- 5.5.3.9 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 Qatar

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 South Africa

- 5.5.5.7 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%) Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Advanced Energy Minerals

- 6.4.2 Altech Advanced Materials

- 6.4.3 Alpha HPA

- 6.4.4 Baikowski SA

- 6.4.5 Bestry

- 6.4.6 Hebei Pengda New Materials Technology Co., Ltd.

- 6.4.7 HONGHE CHEMICAL

- 6.4.8 Nippon Light Metal Company, Ltd.

- 6.4.9 Polar Performance Materials

- 6.4.10 RusAL

- 6.4.11 Sasol

- 6.4.12 Saint-Gobain

- 6.4.13 Shandong Keheng Crystal Material Technology Co., Ltd.

- 6.4.14 Sumitomo Chemical Co., Ltd.

- 6.4.15 Xuancheng Jingrui New Materials Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Application in Scratch-resistant Glasses for Smartphones and Watches

- 7.3 Growing Applications in Manufacturing Optical Lenses